After last week’s drama, things should settle down a bit now, with the calendar looking a lot less frantic. That being said, US Q1 earnings season kicks off this week, and while Alcoa starts things off officially today, JP Morgan and Citigroup will certainly demand greater attention later in the week.

The weak headline print in Friday’s payrolls report taught us a number of things, not least that the long treasuries trade isn’t over just yet. Clearly there was also further confirmation that the USD is trading as an investment asset, as opposed to a pure risk-on, risk-off vehicle. The weak prints in last week’s manufacturing ISM, ADP private payrolls, jobless claims and NFP (non-farm payrolls) have all confirmed the USD’s investment status. The real risk was that an above-consensus number could be the catalyst for the June FOMC meeting to be the forum to portray a more hawkish view on future policy, potentially signalling that the board could curb the pace of asset purchases. It is important to realise however that the unemployment rate (at 7.6%) is just above the Fed’s own year-end forecast of 7.3% to 7.5%, while the six month average is still a healthy 188,000 after the sizeable February revision. Clearly however, this was a weak number, and whether this signals a new trend is yet to be seen, but this is not the first time we seen the Fed hold a public debate about its accommodative policy only for the economy to subsequently fall.

It was also impressive to see such strength in USD/JPY when US treasuries fell five basis point (on the ten-year), but such is the influence Mr Kuroda et al have had on the JPY. The bank’s new focus on expanding the monetary base by 45% this year and 35% is clearly significant, and will keep the JPY notably offered in the medium term. The BoJ has won over the market; the question is which currency to short the JPY against. Today, it seems that the weapon of choice was the CAD, which rallied 1.1%, although we still like AUD/JPY and EUR/JPY from a near-term and longer-term perceptive.

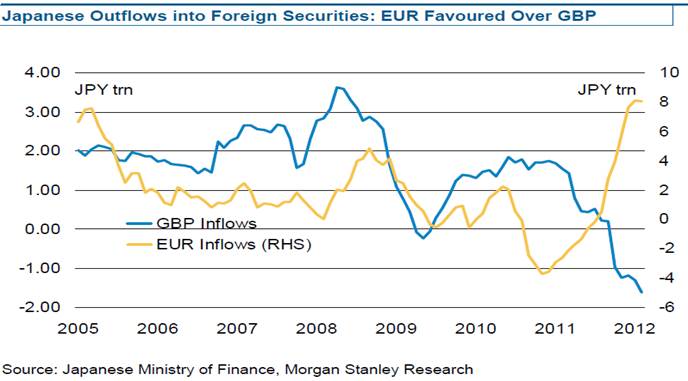

As said, EUR/JPY looks good not just because we like the JPY weaker from here, but because Japanese investors are changing their investment destinations. The BoJ has done a good job pushing traders into equities, and the sizeable inflows into the JPY from domestic players in February are testament towards the mantra of buying Japan before the BoJ does. However, what is also evident is the demand for yield from the different players, and clearly one of the key destinations is the European peripheral bond markets of Spain and Italy. The sizeable moves in yields to the downside on Friday are testament to that, and as long as yields continue to remain bid, so will EUR/JPY.

The Nikkei has predictably rallied today (currently up 2.8%), but once again it has had trouble getting through 13,225, being both the top on Friday and today. The JGB (Japanese government bond) market seemed to have settled down after last week’s volatility helped by the BoJ following through on its commitment to buy ¥1.2 trillion of bonds. Perhaps Christine Lagarde’s comments that the IMF has a positive stance on the BoJ’s implemented measures have helped.

China re-opened on a sour note with the combination of fears of bird flu contagion, increases to down payments on second homes and further rhetoric around North Korea hurting sentiment. China seems to be edging closer to the side of the US, albeit very cautiously. Comments from the Chinese president that no country should be allowed to throw Asia into chaos fell short of directly naming North Korea, but it was pretty obvious who they were directed at. It still feels like the market is giving this one a wide berth for now, but ready to react if it goes a step further, in a situation that is clearly being managed with care from all sides involved and looks as though it is at a key tipping point.

The ASX 200 has managed to etch out a small gain of 0.3%, with materials to provide support. The sizeable falls in the sector have many talking about value trap or value play for the space. As Goldman Sachs pointed out today in a note, that the sector trades on a 30% discount to industrials (on an 11.3x forward PE), with 50% of the metals sector trading on a single digit multiple. Interestingly the sector has underperformed the ASX 200 by 40%, its worst run since 1999; this is usually the time contrarians like to come out to play and there have been some interesting calls from certain investment banks increasing exposure to the space today.

Our European calls look constructive at this stage, but the bias has been to sell although there has really been no conviction behind it and reflects the fact the S&P futures are up 0.4% from the European cash close. The moves by the BoJ of late and commitment of the Fed mean the ample liquidity in the capital markets makes equities very difficult to short at present. With no clear catalyst to provoke a decent pullback, traders are looking at other opportunities. Something that may be worth keeping an eye on though is moves out of Portugal, with its Prime Minister looking to put through new austerity measures after some of the previous measures were deemed unconstitutional by the national court. A failure to come up with these measures could lead to speculation of a new bailout, or perhaps worse. German industrial production numbers are also released and are expected to print +3% in February.