S&P has done a pretty good job in the post GFC environment in tracking the financial vulnerabilities of Australia. Yet it looks like that’s about where its expertise ends because late yesterday it released a report into Australian growth prospects that can only be described as laughably optimistic:

We expect Australia’s mining investment to peak in 2013, which will likely trigger greater dependence on investment in other sectors to drive economic growth.

However, business investment remains subdued and residential investment is only starting to recover.

In addition, the country’s terms of trade are falling and income growth is very weak, while the strong exchange rate is unfavorable for non mining exports and import-competing sectors.

We therefore expect Australia’s transition to non mining-led growth to be a little bumpy, with growth dipping slightly below trend in 2013 to 2.6%, before improving to 3.0% in 2014 and 3.5% in 2015.

In the medium term, stronger mining exports will support GDP growth along with an improving non mining sector.

The key assumption of the note is that falling mining investment will be substantially offset by rising commodity export volumes:

Advertisement

Mining investment rose sharply in 2012 to 8% of GDP (see chart 1), supported by a number of major iron ore, coal, and liquefied natural gas (LNG) projects. This investment allowed the economy to sail through the storms of 2012–including renewed concerns about Europe’s financial crisis, worries about the so-called ‘fiscal cliff’ in the U.S., and a stumble in China’s economic growth–with little collateral damage overall.

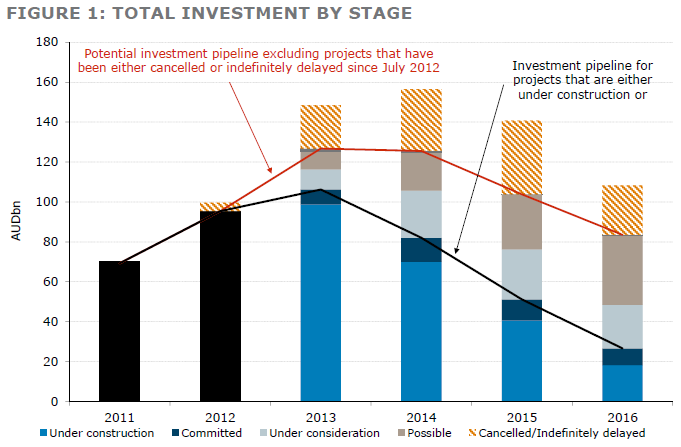

It appears clear, however, that the peak in resource investment is nigh, probably occurring in the coming year. It’s also likely to be sooner and at a lower level than was expected a year ago. The dramatic falls in iron ore and coal prices in September 2012 have resulted in a more circumspect attitude among resource companies regarding the medium-term strength in commodity prices and demand from China. Companies have shelved a number of mooted, marginally-viable mining projects indefinitely, and the sector has turned its focus to reining in costs.

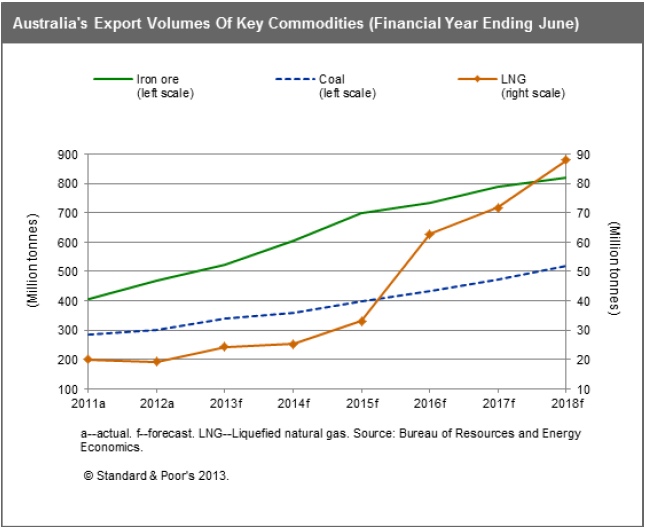

…Mining investment will inevitably be a drag on growth once it passes its peak, but the economic benefit of the massive increase in mining capital stock over recent years is only beginning to be realized. Over the next six years, as further projects are completed, we expect iron ore and coal exports each to rise by more than 70%. Likewise, we predict LNG exports will jump more than four-fold over the same period. Following the booms firstly in commodity prices and then mining investment over the past decade, this “third phase” of the resource boom will support Australia’s economic growth and trade balance in coming years.

I’ve cross-referenced these forecasts and although there’s no reference upon them, they are a nearly perfect fit for those of BREE, the official Australian government forecaster. So, in effect, S&P is recycling the official view of things that we’ll see a manageable decline in investment offset by rising export volumes.

There are two problems in this view. The first is that the mining investment decline will not be slow. The end of the LNG boom means that 2% of GDP per year from 2014 to 2016 will disappear. That is a VERY deep hole and export volumes will not offset it:

Advertisement

Second, strong volume projections will also result in coal and iron ore price collapses, which means a couple of things:

although net exports will contribute to real GDP, nominal GDP will be even more weak than it is now:

Advertisement

national and personal income growth is derived from nominal GDP and will also therefore be very weak and probably in recession, as it is now:

Advertisement

that means that any attempt to resuscitate growth via non mining investment will run into conservative banks. Poor income growth means falling deposit growth leading to greater offshore borrowing by banks to fund loans (which S&P has warned will result in bank downgrades)

government receipts will be very weak. Even if the government persists with current tight fiscal policy settings, deficits will grow substantially anyway across the cycle (which S&P has warned will result in a sovereign downgrade)

Ironically, S&P does not understand the linkages in the Australian economy between the terms of trade, mining investment, income growth and credit that will prompt it to downgrade both the sovereign and banks in the next two years.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.