Yesterday, Captain Glenn Stevens warned that Chinese shadow banking needed to be watched closely:

…concern has been expressed about the risks that may be growing in the ‘shadow banking’ system in China. In recent years, an increasing share of financing in China has been provided by non-bank entities and through banks’ off-balance sheet activities. In no small part, this growth in shadow banking reflects restrictions on both the quantity of bank credit, and controls on loan and deposit rates. Such restrictions lead to demand for credit exceeding the formal banking sector’s ability to supply it, and also provide an incentive for savers to seek alternatives to low-yielding bank deposits. The Chinese authorities have introduced a number of measures to mitigate the risks, and many types of shadow banking activities in China are now subject to some regulatory oversight. Hopefully, this will lead to a stable outcome. But China’s experience is one that others have had at various times: as long as there are incentives to by-pass the formal banking sector, the shadow banking system may keep on growing together with the risks.

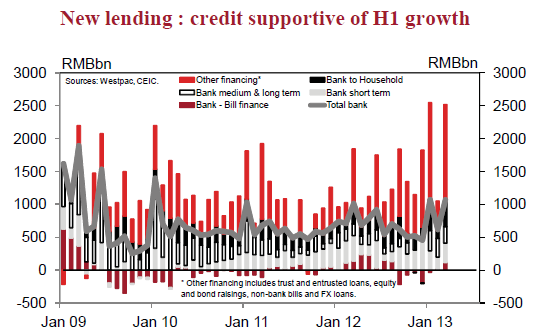

And later in the day we received the March Chinese new loans data which more than confirmed RBA concerns. Bank loans originated a trillion or so yuan, but shadow banks originated another 1.5 trillion. The total result was a big number:

Late in the day, Phat Dragon provided another chart on the formal/shadow split:

So, Chinese shadowing banking is providing some 60% of the nation’s financing flow, up from a third only two years ago. That’s growth.

We have very little to compare this with. But as a basic point of reference, we can juxtapose these proportions with the US credit system, the home of shadow banking in the past several decades.

On a stock of assets basis, US shadow banking hit almost half of the nation’s total before the GFC:

But that’s only if we exclude the GSEs, Fanne Mae and Freddie Mac, which we should not do given they were semi-private and required some of the largest components of the bailout. The ratio then becomes two-thirds to one third, shadow versus balance sheet banking.

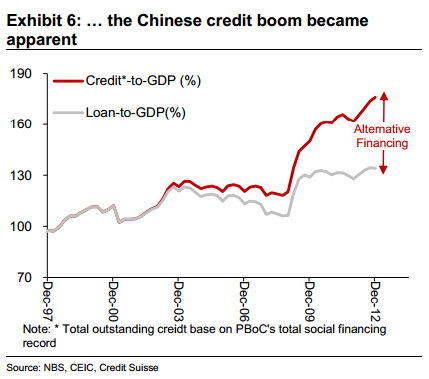

Acccording to Credit Suisse, in terms of the total stock of China’s credit assets, shadow banking still accounts for below 30%:

Does this tell us anything useful? The US and Chinese systems are miles apart. But in the end, banking is banking and the same counts for shadow finance. It shares the common charateristics of being cheaper and more profitable than traditional banking because it gets around capital reservation. It tends as well to rely on borrowing short and lending long, even if at heart it matches maturity durations. Both of these make it stable and profitable so long as nothing happens to confidence in the market for short term funding. Sadly, something always goes wrong sooner or later because there is no capital backstop or government support to prevent it.

That doesn’t mean a collapse in Chinese shadow banking is imminent. But let’s just say that if allowed to grow at its current pace much longer, Chinese shadow banking will loom as an uncomfortably large component of Chinese financing even if still below the US prior to its meltdown, which is a sobering addendum to Glenn Stevens’ point.

Recently, some have argued that although this is the case, in the event of a bust, Chinese authorities have the resources to the recapitalise its banks, as it assuredly does.

But so too did the US, with its nationalisations of the GSEs, AIG etc and $700 billion TARP programme. It may be that the Chinese will be better placed to not have to borrow quite so much in the public sector to fund any recapitalisation but that’s not terribly comforting vis-a-vis the economic fallout from any bust, which will still bury private sector balance sheets for a quite a while and, although not suppressing activity so long as it did in the US given China’s underlying productivity boom, will still mean a permanent shunt lower in growth.

The question is, then, is that what we’re in for this year? Back to Phat Dragon:

What is the correct interpretation? One could cite the results of the March quarter banking climate survey that reported a perception that for practical purposes monetary policy is still easy, despite ‘jawboning’ efforts such as lower M2 and CPI targets – not to mention a range of tightening measures for housing and greater financial regulatory focus. Proponents of this thesis might argue, plausibly [but incompletely], that the recovery in the real and nominal economy since Q3 last year, in addition to the lagged impact of 2012 easing, is having a predictably positive impact on private sector confidence. A fuller explanation would allow those points, but also offer a behavioural overlay. With the future direction of policy very clear, rational agents will bring forward their borrowing activity [and their property transactions and project approvals], aggressively pre-funding rather than relying on the smooth future availability of capital. Phat Dragon argues that Chinese lenders and borrowers frequently collude to beat unobservable but potentially imminent deadlines. This gives the appearance of low policy traction in the first instance, but these dynamics sow the seeds of an abrupt slowdown later, as policy makers tend to lose patience and eventually resort to harsh controls.

In other words, at minimum we’re in for a rerun of last year with tightening eventually puncturing enthusiasm for credit. But with a difference. The cyclical bogey man that needed taming last year was inflation. This year it looks more like the future stability of the Chinese banking system.

Whether or not tightening turns into a more enduring slowdown and balance sheet reckoning will depend upon just how serious Chinese authorities are about rebalancing and ending the investment and property boom. Michael Pettis argues that they are but he also observes, rightly, that the Chinese are caught between the proverbial Scylla and Charybdis and may lurch from loosening to tightening to loosening in increasingly frenetic cycles.

I don’t have the answer but it’s obvious that the stakes are rising fast and the longer it isn’t done, the worse it will be. I still say that the costs of delay for the Chinese are now greater than the price of action today.