While much of the nation is busy today discussing how to carve up the Australian magic pudding economy, the reality that the sausage is already depleted seems a distant prospect. But the fact is that Woodside’s decision to shelve Browse last week has ended the mining boom and we must now find new ways to develop investment if we are to grow.

To do so we must become more competitive, and we will, one way or another. There are two models to achieve it.

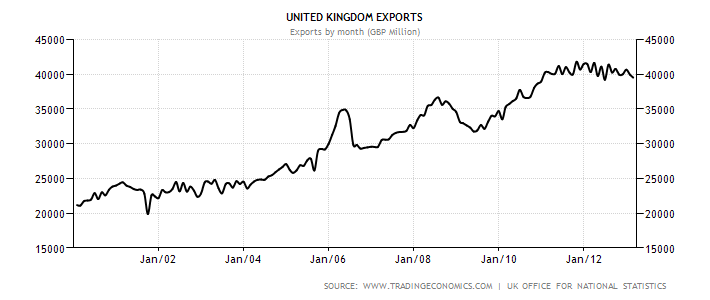

The UK model

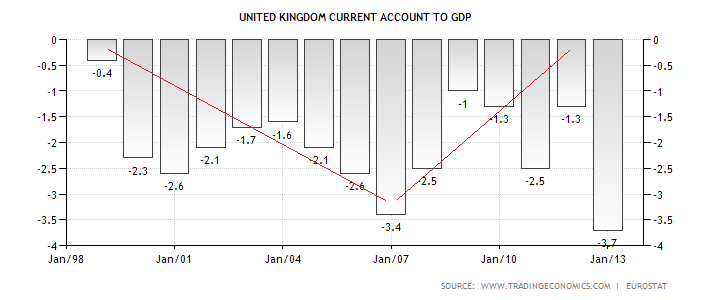

When an economy’s standard of living surpasses its productive capacity it tends to run large current account deficits as it borrows offshore and invests in unproductive stuff like property to support its inflated living standards. This game can run for a long time but eventually it runs out of gas when that nation’s external position deteriorates enough to spook markets about the risk of not being repaid. Such is what happened to the UK in the GFC:

At this point, a country has limited choices. It can continue to borrow via the public sector, as the UK has done, to support growth:

As well as drop interest rates very low to ease the repayment burden on the private sector. This has the added benefit devaluing the currency which makes the nation even more competitive.

With a bit of luck you also get productivity gains but that is uncertain if investment takes time to ramp up. The UK has not done well on this front. The US, which is also pursuing this same model, has done much better.

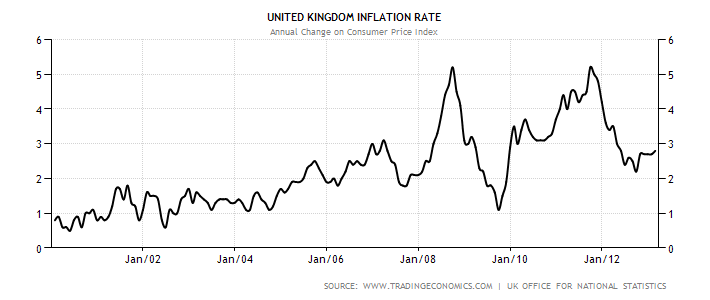

The lower currency may, in turn, spark inflation, which also serves to devalue the debts that are burdening both public and private sectors and the real price of labour. This the UK has also done:

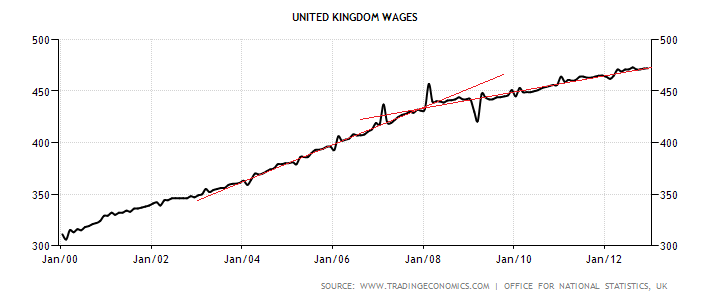

And thus, wage growth since the GFC has been modest and well below inflation:

The UK is devaluing via these various inputs and was succeeding quite nicely in growing via external demand until Europe descended into its crisis:

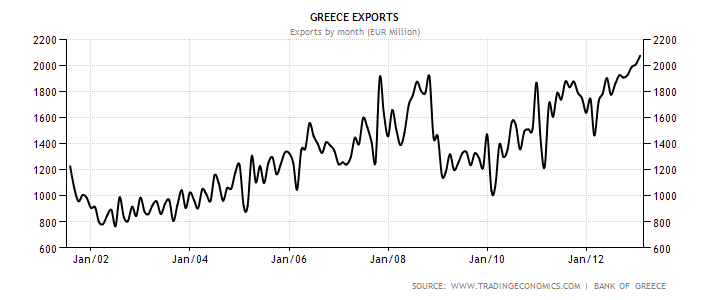

The European model

Which brings us to our second model. Europe’s fringe states are pursuing, or rather are being forced to pursue, an exclusively internal devaluation. The major differences to the UK approach are that government spending is cut, not expanded, and because of the common currency, there is no boost to competitiveness via a falling external price.

In Greece, for example, this has meant that wages are taking the brunt of the price adjustment:

Which has worked well to boost the external demand for its goods:

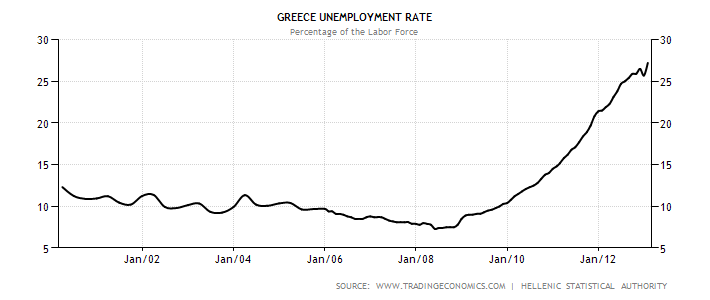

But it also means unemployment is through the roof and social unrest is a constant risk, not to mention general social suffering:

In this scenario growth is also so lousy that the real debt burdens in the economy actually grow despite cutting spending.

Australia’s adjustment

Australia is better placed than the UK or Greece for the reason that it has a built-in ramp up of exports under construction already in the LNG boom. Some might argue that the same is going to happen in volumes for the bulk commodities but they are wrong. The expansion in iron ore and coal is in trouble, with supply set to leap frog demand later this year and then leave it far behind. If anything, the LNG boom will substitute for this deflating boom, not build upon it.

And that presents Australia with a pricing problem. We have enjoyed the high wage and income growth rates of the mining boom largely because China paid more for our goods not because we earned it though working more efficiently. As that income falls, so too will our capacity for wage increases and, if the falls are large enough, as I think they will be, then the nation will need to deflate somehow to repair its competitiveness and boost investment.

So, how are we going to do it?

So far, as the terms of trade have fallen and mining investment begins to fall, unemployment to slowly rise and wage growth to slow our response has been to cut interest rates and ease off fiscal tightening. In short, we’ve so far pursued the UK model.

Though productivity is rising, the above has not resulted in falls in the currency. So enamored have global markets become with of the Australian dollar that it is going to take a crisis to knock it off its perch.

In the mean time, non-mining private investment is rebounding very modestly on investor’s search for yield in asset markets, delaying the reckoning but not halting it. As mining investment and the terms of trade come off further they will overwhelm the asset inflation in economic terms, interest rates will fall again and so will the currency. Judging the timing of this is the hard part, though we have one useful pivot point to examine in the forthcoming change of government.

If the incoming Abbott government chooses to slash spending when it assumes office then growth will fall sharply going into 2014. Interest rates will have to fall quickly too and this will bring a lower dollar sooner. But the dollar has been high for too long so we’ll not see any immediate substantial rebound in non-mining tradeables. That will take time.

Moreover, this austerity path of devaluation comes with the risk that unemployment rises quickly and overwhelms the specufesting pulse in the property market. Asset prices could roll over and a bust ensue. This would feed back into government revenues and spending via automatic stabilisers and comprehensively blow up the drive for surplus.

The one advantage of this approach is that there is unlikely to be an inflation problem as the dollar falls because deflationary forces from the weak labour market offset rises in tradable prices. The Phillips Curve works pretty well in Australia.

The alternative approach for the incoming Abbott government is declare post election that the budget is a mess, blame it on Labor, and retain deficits at least for its first term. Then the adjustment can take a path more like the UK model. Unemployment will rise more gently and further falls in interest rates and the dollar will take longer.

The disadvantage of this is that it implies a higher level of aggregate demand in the economy even as the dollar falls. That means the deflationary offsets to rising tradable prices are likely to be lower and inflation may well become a problem, confronting the RBA with a stark choice.

Does it raise interest rates, choke off inflation, and take us down the bust path? Or let it run like the UK did?

This path has other limits too. The deficits will not be able to rise much from current levels because it will result in the loss of Australia’s credit rating within a year or two. Politically, and in terms of the downgrades that follow through in the banking sector, this also starts the nation down the faster adjustment path as borrowing costs rise and the Abbott government comes under more pressure to repair the budget.

Any way you look at it, if the terms of trade fall in conjunction with mining investment, Australia is going to have to devalue and risk a bust.