Our favourite China observer, Westpac’s Phat Dragon, today feigns humility before blaming Chinese data manipulation for yesterday’s big GDP miss. In true Australian fashion, the AFR embraces this easy excuse without pause (find the full report below).

A more constructive approach is taken everywhere else and is summarised nicely at FT Alphaville which is cross-posted below:

It’s nice that China can still surprise us:

A double-digit rise in bank lending and a surge in total credit in the economy in the first three months of the year, together with forecast-busting import growth in March, have set analysts thinking the economy is expanding faster than expected and policymakers may have to act to restrain it. (Reuters, yesterday)

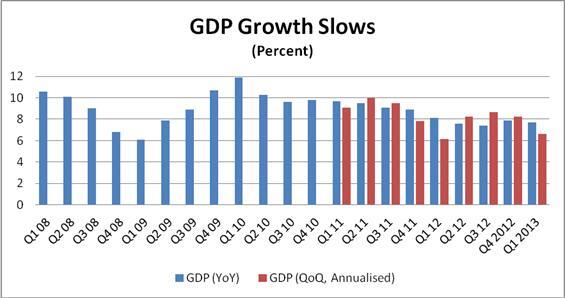

Every strategist around, it seems, was expecting an increase in the YoY quarterly growth rate after the recent credit surge. Of course… it didn’t happen. The Q1 GDP growth figure published today was 7.7 per cent above the same period in 2012, well short (relatively) of the 8 per cent that was expected and lower than the previous quarter’s YoY figure of 7.9 per cent.

Yet much of the reason for those expectations of credit tightening are still there: credit really surged, particularly in March.

Most other China data released today – March numbers for industrial production, fixed-asset investment, electricity output and retail sales — was also an unhappy surprise (numbers can be found here):

Unlike many countries, China does not publish an annualised adjusted quarter-on-quarter GDP figure, but only a year-on-year figure and a seasonally-adjusted quarter-on-quarter figure. We explored this at length last year, and this Q1 growth rate looks worse if given the more standard treatment. The officially-provided, seasonally-adjusted QonQ rate is 1.6 per cent, which annualises to 6.6 per cent.

Alistair Thornton of IHS Global Insight has charted both rates:

However, that’s perhaps nitpicking; we’re still talking growth rates that would be the envy of the world, et cetera…

We think the biggest question out of today’s GDP number is what it means for China’sincreasingly credit-fuelled growth model.

There’s a couple of ways of looking at this.

There’s total credit outstanding to total nominal GDP. In Q4 2012, as calculated by Michael Werner of Bernstein:

However another way of looking at it is to compare the rate of financing flows compared with the rate of GDP growth; that is the growth created by each marginal yuan of credit. On an unadjusted, nominal comparison, GDP for Q1 2013 was about Rmb1.1tn higher than the previous year, while the credit issuance rate increased about Rmb2.27tn year-on-year. So that very rough calculation gives us about a 2x relationship, although it’s not a great description of the situation because it’s comparing gross new issuance with growth.

Bernstein’s Warner calculated the credit multiplier on a rolling basis in January, showing that the credit:growth ratio has plummeted from about 1:1 to 3:1 – that is, about Rmb3 of new credit for every Rmb1 of new growth:

The above chart is based on Bernstein’s own estimate of credit growth, which they call Total Credit Formation, but that metric also likely deteriorated in Q1 as the official measure of credit growth was dramatic this quarter. Below is a chart of Total Social Financing growth; TSF is the government’s measure of credit issuance including some shadow financing:

Again, this is gross new credit, but clearly this latest quarter was something special.

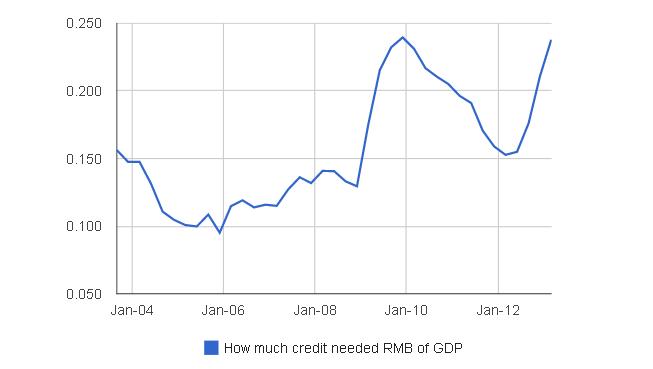

In fact, we can be quite sure the latest quarter of credit growth will have thrown the credit:GDP ratio because of this chart from HSBC’s Fred Neumann, via Beyondbrics:

This chart, unlike the second Bernstein one, does go up to Q1 2013. A key difference is Neumann compares credit issued against total GDP, rather than GDP growth. So where he comes up with a ratio of 1:4.7 in Q4 — that is, Rmb1 of credit issued equalling about Rmb4.7 of GDP — whereas Bernstein’s Werner (and others such as IHS Global Insight’s Thornton) have calculated this as Rmb1 of credit issued to about Rmb0.3 of GDP growth.

To do a very rough extrapolation, that would mean the ratio decreased by about 11 per cent.

So, in terms of new credit-to-GDP growth; we’re still in the realm of every Rmb1 in growth requiring about Rmb3 in credit for every Rmb1 of growth; only the ratio is edging further upwards and it’s something like Rmb3.3 for every Rmb1 in growth.

However, there’s always a bullish point to be found in the morass of numbers on a big China data release day. Firstly: if the numbers are so fake, why not make them look better?

More seriously: much of the Q1 credit surge was in March and so, perhaps it simply hasn’t kicked in. This is what Societe Generale are suggesting — but even so, they are hardly bullish:

We do not think Q1 marked the end of recovery, as the lagged impact of rapid credit growth in the past few months should kick in later. However, at the same time, the latest data firmly support our call for a weak and short-lived cyclical recovery of the Chinese economy in 2013.

Finally, perhaps we are seeing some evidence of China rebalancing away from its incredibly high level of investment towards a more consumption-based model?

Capital Economics, from whom the chart above comes, are not convinced however. They point out that for the past few years, consumption’s share of growth has jumped in Q1, only to fall back during the rest of the year. The chart shows this trend clearly.

One more big argument for the bearish case: the export component of that Q1 growth is probably overstated; a surge in exports to Hong Kong in recent months, and to a lesser extent to Taiwan, is believed to reflect attempts to get around China’s capital controls, together with a little tax rebate scamming.