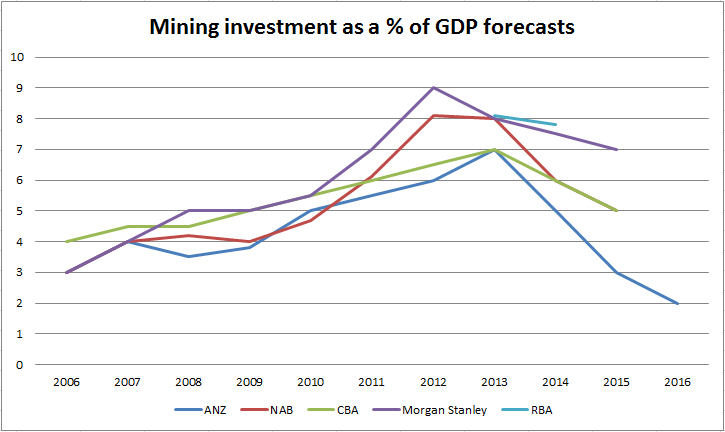

Regular readers will know that the Australian economy is approaching (or already over) the mining investment cliff. Here is my compilation of various estimates:

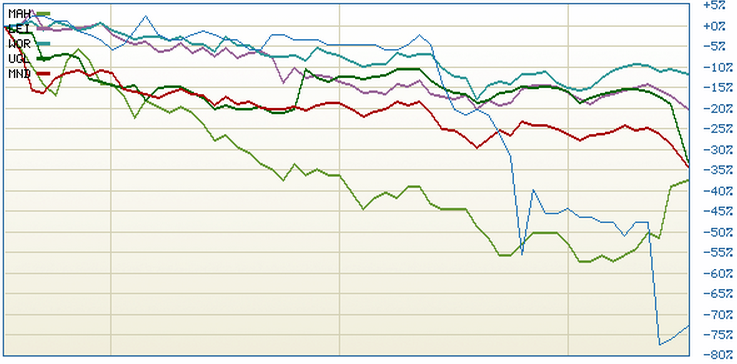

It is pretty clear that the cliff’s edge has arrived. It has been made equally clear this week and last by the gathering number of pledges from big miners that they’ll cut capital spending and by the number of profit warnings in the mining services sector. The last three months of share performance for the latter speaks volumes:

Advertisement

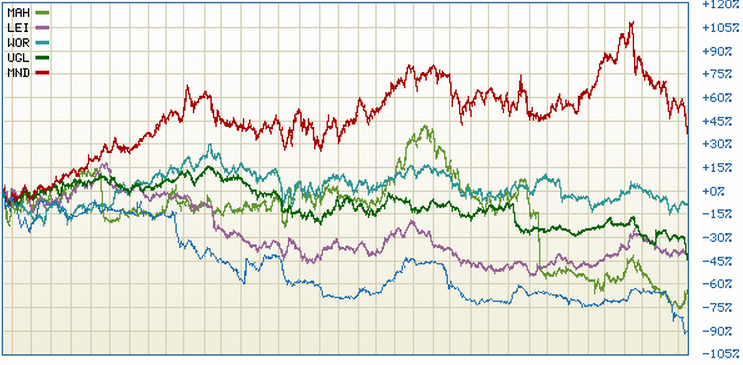

Though a three year chart shows plenty of downside left in this baby:

As a quick aside, anyone buying into or advising buying into this sector in the early months of 2013 (which there were clearly plenty of) should get the bullet.

Advertisement

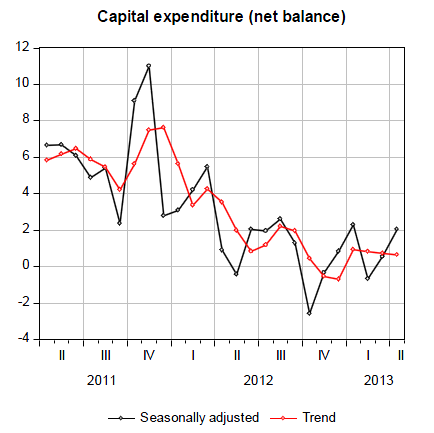

But back on point, there is mounting evidence of sharp cut backs in mining capital spending via delayed or cancelled projects. Also, this months’s NAB Business Survey suggested a sharp downside looms. The capex index rose slightly in April, but the internals were less reassuring:

The capex index lifted again in April – up 1 to +2 index points. Overall, this level remains relatively low compared to recent history, with the general softness largely reflecting the sharp downturn in mining capex reported over the past year or so. In fact, mining capex reported a sharp deterioration in April, down 12 to -5 points. Capital expenditure fell considerably in retail (down 18 to +1), while it lifted notably in manufacturing (up 9), finance/ business/ property (up 8) and recreation & personal services (up 6). In levels terms, capital expenditure was highest in recreation & personal services and transport & utilities (both +6), while it was lowest in wholesale (-8) and mining (-5).

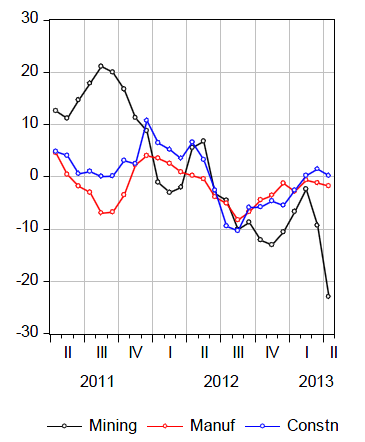

And if we look forward, using the proxy of business confidence as a rough guide to where capex intentions will go, the same survey already presented the mining cliff:

Advertisement

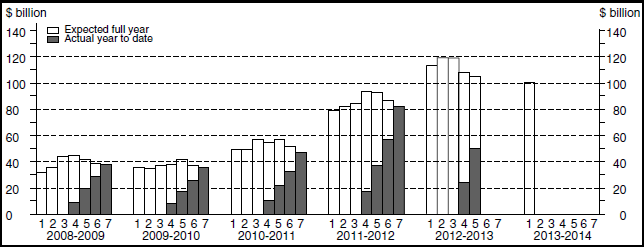

So, why May 30 as a potential cliff’s edge? You may have noted the RBA’s confident little line in the first chart, suggesting that we face not a cliff but a gentle down slope. That judgement is based upon the quarterly ABS capex intentions survey, which in the March quarter was still radiating confidence:

Mining fell 11.6% from the comparable estimate in 2012/13 but was still better than feared:

Advertisement

The clear bars are the capex estimates for the full financial year ahead as judged by mining each quarter. As you can see, the current estimate for 12/13 is a little over $100 billion. The 13/14 year is at $100 billion. If these two bars, especially the second estimate for 13/14 were to fall sharply then it will ring major alarm bells in financial markets, even if there is some offset in other industries.

That’s why May 30. It is the release of the updated quarterly capex report. Will it happen? Well…the point of the post is that there is circumstantial evidence in the market that it could.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.