Only the good “news”, err “opinion”, err whatever it is over at the AFR today:

The Australian dollar could be the boost the sharemarket needs as May shapes up to be the worst month in the past year for equities.

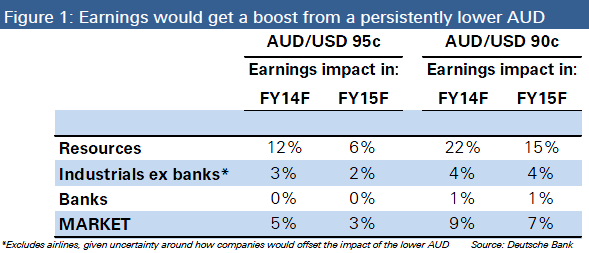

Deutsche Bank is the latest to run the numbers on the impact of a weaker currency for stocks and at US95¢ – only slightly below current levels – this translates to a 5 per cent increase in 2013-14 earnings. At US90¢, earnings improve 9 per cent.

The $A was buying US96.53¢ late on Tuesday. The prospect of an earnings upgrades is important because expectations for the next financial year are already vulnerable to downgrades.

The past month has seen the annual confession season play out with mining services companies and consumer discretionary stocks rushing to slash market expectations as projects are deferred or cancelled and the domestic economy betrays weakness.

This coincides with a volatile period for shares. However, Citigroup on Tuesday upgraded its forecast for the S&P/ASX 200 Index, defying recent sell-offs including a 3.8 per cent rout last week. The ASX 200 closed up 10.8 points, or 0.2 per cent, at 4970.7.

Citigroup strategist Tony Brennan raised his year-end target for the index to 5400 points and released a mid-2014 forecast of 5600 points.

…The much maligned resources sector is the clear winner from any Australian dollar dips, making commodity exports more competitive.

Citi also downgraded the ASX Underweight just last week. Then, suddenly, this yesterday:

Until a few days ago, our end-year forecast for the ASX200 of 5200 was being tested, after less than five months of the year. Now, there seems to be a feeling that the rally could be over, with signs from the Fed that QE3 could be stepped down in coming months. Realistically, the strong gains in the market were almost inevitably going to slow, but we don’t think the recovery is over, and have raised our end-year forecast to 5400, and put forward a mid-2014 forecast of 5600. The market should be able to maintain a close to average multiple, and continue to move higher with reasonable earnings growth, which still looks on track.

Equities don’t look expensive

Even before the pullback in the market in recent days, equities hadn’t looked overly expensive to us. The rally had taken the market multiple to a little under 15x one year ahead consensus earnings estimates, slightly above its average of the past two decades (the present era of low inflation and interest rates in Australia that we think provides the best benchmark for valuations). So the market multiple was a little on the high side, but not dramatically so, and it has also now come back (Figure 5).

The market fell about 4% in the interim and now Citi’s target has jumped 200 points higher than when the underperform order was issued 7 days ago.

Meanwhile, the Deutsche report that the AFR champions has one fatal flaw that the paper also fails to address. Why is the dollar falling? Cutting through the drivel, it is basically because the mining boom is over. There is a material risk that bulk commodities, especially iron ore, will keep falling with the dollar, cancelling out any gains. Like today, for instance.

Of course a falling dollar will help:

Just not the miners and banks that make up most of the market! Look to dollar exposed industrials with the lowest possible involvement in the Australian economy! That’s where better is available from Shaw Stockbroking today:

| Company | ASX Code |

Broad Business Exposure | |||

| Australia | US | UK/Europe | Asia/China/ Emerging | ||

| Aristocrat | ALL | 20% | 60% | 20% | |

| Amcor | AMC | 22% | 30% | 25% | 22% |

| Ansell | ANN | 5% | 55% | 40% | |

| Boral | BLD | 75% | 25% | ||

| Brambles | BXB | 40% | 40% | 20% | |

| Cochlear | COH | 5% | 55% | 35% | 5% |

| ComputerShare | CPU | 10% | 60% | 30% | |

| CSL | CSL | 10% | 60% | 30% | |

| Insurance Aust | IAG | 85% | 15% | ||

| James Hardie | JHX | 10% | 90% | ||

| Leightons | LEI | 65% | 35% | ||

| Lend Lease | LLC | 32% | 32% | 32% | 4% |

| Macquarie Bank | MQG | 45% | 15% | 20% | 20% |

| News Corp | NWS | 10% | 60% | 20% | 10% |

| QBE Insurance | QBE | 20% | 40% | 35% | 5% |

| Sonic Health | SHL | 60% | 20% | 20% | |

| Toll Holdings | TOL | 65% | 35% | ||

.