Yesterday afternoon, consultant Wood Mackenzie poured cold water over the view that Australia is on the verge of a mining investment cliff, whereby mining-related capital expenditures (capex) fall sharply from their current lofty level of nearly 7% of GDP (see next chart).

From the Wall Street Journal:

SYDNEY—Investment in Australia’s resources sector should remain strong over the next three years, according to consultancy Wood Mackenzie, which Thursday said fears of a sharp slide in spending after a 2013 peak aren’t likely to be realized.

While some major companies like BHP Billiton Ltd. and Woodside Petroleum Ltd. have been shelving resource projects due to rising costs and weaker commodity prices, Wood Mackenzie said it expected committed gas projects like the US$34 billion Ichthys liquefied natural gas project in Australia’s Northern Territory, and the resumption of previously deferred coal developments, to keep investment in Australia near historical highs for years to come…

“Today’s decision makers are faced with different challenges in a changing environment, [but] the outlook for the next three years confirms the strength of the Australian resource sector, as we see investments being made based on decisions taken during the boom years,” said Chris Graham, head of Australasia upstream research for the U.K.-based firm.

The energy and metals consultancy forecast resource sector investment here to peak in 2013 at 85 billion Australian dollars (US$84 billion), but to remain robust for a while thereafter.

“The high investment levels will be sustained over the next three years, surpassing the previous three-year period”…

While the coal industry remains under pressure due to weak prices, deferred projects would ultimately be revisited as prices recover and this, together with the development of new producing areas such as Queensland state’s Galilee Basin, would keep capital spending elevated until at least 2017, Wood Mackenzie said.

“This will drive an increase in coal’s proportion of overall capital spend in Australia, taking over iron-ore’s position as the commodity with the second-highest investment” after gas…

My only issue with Wood McKenzie’s analysis is that it seems predicated on a strong rebound in coal prices and the re-instatement of deferred capex projects. I cannot see this happening.

For starters, thermal coal exports are already under extreme competitive pressure from the United States, where the shale gas boom is displacing coal in domestic electricity generation, leading to high quality thermal coal being dumped onto the seaborne market, depressing prices globally. Indonesia, which is the world’s largest thermal coal exporter, has also ramped up production recently following significant capex (see next chart).

The demand outlook is also uncertain, with major importers – the European Union and even China – stepping-up efforts to limit emissions, which could significantly curb coal use.

In short, it’s difficult to see thermal coal producers committing to new capex when competition is high and the demand outlook is murky.

As for coking coal, it should (in theory) follow iron ore, since both commodities are used in steel production. With Chinese steel production growth tepid, and question marks over the robustness of the Chinese economy, it’s also hard to see why any producer would commit to significant new capex.

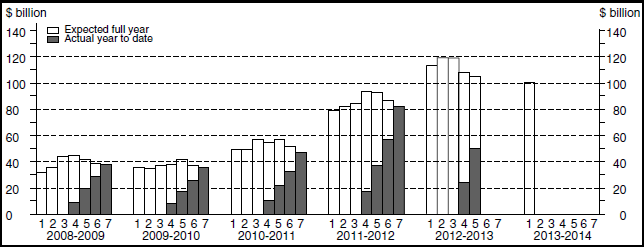

As noted by Houses & Holes yesterday, the ABS is scheduled to release its capex intentions survey for the March quarter on 30 May, which will provide insight into whether Australia is facing a cliff or plateau in mining capex.

The clear bars above are the capex estimates for the full financial year ahead as judged by mining each quarter. As you can see, the current estimate for 2012-13 is a little over $100 billion, whereas the 2013-14 year is also at $100 billion. If these two bars, especially the second estimate for 2013-14, were to fall sharply then it will indicate that Australia is facing a capex cliff.

For starters then, if Wood Mackenzie is right about $85 billion for 2013, that is already a mining investment cliff based upon official 2012 estimates. The only factor that can swing things in a more benign direction of ongoing higher investment is a substantial fall in the dollar.

unconventionaleconomist@hotmail.com