The liquidity squeeze in the Chinese banking system is staring to concern important people, though yesterday it was confirmed what Phat Dragon has been arguing for some time, that it is deliberate. As Simon Rabinovitch wrote for the FT:

The China Securities Journal, a major state-run newspaper, ran a front-page commentary saying China was at a turning point in monetary policy.

“We cannot use as fast money supply growth as in the past, or even faster, to promote economic growth,” the newspaper said. “This means that authorities must control the pace of money supply growth.”

And the PBOC is doing just that. On Wednesday it tightened the screws, or, to put it more accurately, it allowed them to tighten. Short-term interbank rates leapt more than 200 basis points, setting a record high of nearly 8 per cent for loans of one month or less.

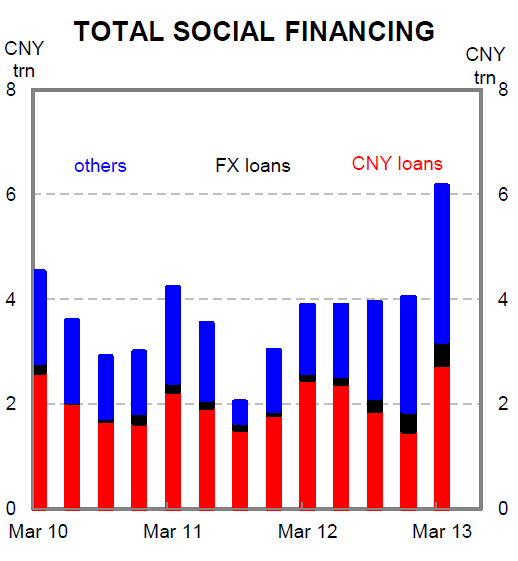

The consensus is that this is aimed reigning in the extraordinary surge in shadow bank financing in the first quarter that I’ve noted many times. Here’s the chart from the CBA:

This is effectively a rerun of what transpired at the end of 2011, at least in policy terms, if not in terms of the intended target (then it was banks not shadow banks). It is interesting how little discussion there is this time around about the consequence of a Chinese “hard landing”. It’s a bit weird actually, given that within six months of the 2011 crunch, Chinese growth had fallen 1.5% of GDP:

I see no reason to think we’ll not repeat the outcome. When was the last time you can remember any major economy strangling credit without hitting growth? China has the advantage of being able to order its banks to turn on the credit spigots very quickly and finance a new round of infrastructure growth and we can perhaps expect some of that again. Though it’s hardly likely to be large given the overall objective of switching to consumption drivers. And let’s think positive and assume that the credit crunch doesn’t actually turn into a bad debt crisis for the (shadow) banking system.

Even so, it seems to me reasonable to conclude that we have in place the variables for sub 7% Chinese growth by the end of this year.