Some more flash PMI data out of the Eurozone overnight and although the data continues to improve in terms of the rate of decline there is some worrying signs that not all is as good as the headline figures suggest. German data is at stall speed with weak future indicators.

Marginal growth in output was recorded in the German private sector during June, but latest PMI data pointed to declining new orders and a second successive monthly fall in employment. The seasonally adjusted Markit Flash Germany Composite Output Index posted 50.9, up from the reading of 50.2 in May. Overall growth in output was largely reflective of higher activity in the service sector (51.3), while manufacturing production was broadly unchanged (50.1).

In contrast to the expansion of output, new business decreased in June amid signs of weakening demand in both domestic and export markets. The rate of decline in new orders was solid, and slightly faster than in May. Services companies posted a stronger decline than manufacturers, despite goods producers reporting the fastest fall in new export orders of 2013 so far.

A further decline in backlogs of work was recorded during the month, although the pace of reduction eased slightly. Both sectors depleted outstanding business in June but, as with new orders, the rate of decline was sharper at service providers. Falling workloads led companies in Germany to reduce employment in June, with staffing levels decreasing for the second successive month. Moreover, both manufacturing and services registered faster rates of job shedding than in the previous month.

Germany also has the major flooding to contend with over June ( more details here ) and the overall effect of this should be caught in the next reading. On top of the weak future orders and employment outlook I get a sense that we could be about to see a roll-over in the German economy which, together with what we are currently seeing out of China, is a quite worrying sign for the zone.

That being said there is some reason to be optimistic with this months data continuing to be positive in terms of the deceleration of contraction and signs of more re-balancing across the region.

Advertisement

Flash Eurozone PMI Composite Output Index(1) at 48.9 (47.7 in May).15-month high.

Flash Eurozone Services PMI Activity Index(2) at 48.6 (47.2 in May). 15-month high.

Flash Eurozone Manufacturing PMI(3) at 48.7 (48.3 in May). 16-month high.

Flash Eurozone Manufacturing PMI Output Index(4) at 49.5 (48.8 in May). 16-month high.

The Markit Eurozone PMI Composite Output Index rose from 47.7 in May to 48.9 in June, according to the flash estimate, indicating the smallest downturn in business activity since March last year.

The sub-50 reading nevertheless rounded off another weak quarter. At 47.8, the average reading for the three months to June is only marginally higher than the 47.7 average recorded in the first three months of the year, suggesting that the eurozone’s recession will have dragged into a seventh successive quarter.

Although activity continued to decline overall, the third consecutive monthly rise in the PMI in June indicated that the rate of contraction is on a moderating trend. Manufacturing output fell in June at the slowest rate in the current 16-month sequence, registering only a very modest decline, and services business activity showed the joint- weakest fall since March 2012.

Adding to the picture of the downturn moderating, new business fell at the slowest rate for five months, the rate of decline having eased for the third month in a row. New orders in manufacturing fell only marginally, registering the smallest decline for two years, while the services sector saw the smallest fall for five months.

So certainly some reasons to be positive, as can be read in the wrap provided by Markit’s chief economist.

The flash PMI indicates that the Eurozone contracted again in June, rounding-off another weak quarter, but there are reassuring signs that the downturn is continuing to ease.

The survey data suggest that GDP is likely to have shrunk by 0.2% in the second quarter, similar to the fall seen in the first three months of the year and extending the region’s recession into a record seventh successive quarter.

Encouragingly, however, the rate of contraction has eased over the course of the second quarter, with the decline in June the smallest for 15 months. At this rate, the region could stabilise in the third quarter and return to growth in the fourth quarter.

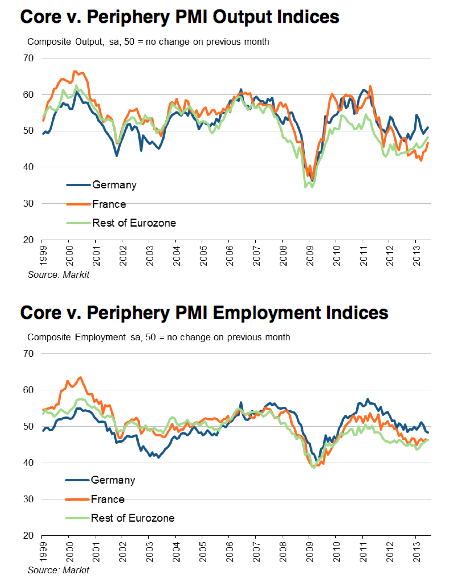

It is particularly welcome news that the rate of decline outside of France and Germany has slowed sharply in recent months, and is now the weakest for two years. The rate of contraction has also slowed sharply in France, while Germany is showing signs of faster, albeit still modest, growth.

Euro area policymakers will no doubt be encouraged by these improving indicators, suggesting the ECB will see no need for any further action in the near term.

Advertisement

I’m not so sure I share the same level of optimism. France, although improving, still looks weak and unemployment continues to climb. Italy also remains weak as does Portugal and the Dutch are continually downgrading their own estimates of economic growth. We certainly have seen some renewed export sector strength out of Spain, obviously at the expense of employment, but the issue for the Eurozone was never whether one or two countries could successfully implement a rebalancing, it was whether all of them could at the same time. As I’ve stated before Italy and France together have a GDP in excess of that of Germany, and although we are witnessing some improvement in the macro settings of some of the periphery nations, with the exception of employment, the problems have now made their way to larger economies which will require much larger compensating factors to counter-act these downturns.

In reality what is required is a further re-alancing from the creditor nations of the zone and , although we have seen some action in wage inflation in Germany, the country is still running massive trade surpluses which have to, in part, be recycled through opposing deficits within the Eurozone. The Eurozone has also been counting on an improving global economy to stimulate external demand, however after yesterday’s China PMI and what looks to be a possible credit crunch looming in the country that hope is looking increasingly shaky.

All up this data is still positive but, as witnessed in German future orders, there are once again looming dark clouds on the horizon of the global economy and Europe is in no shape to deal with an external demand shock.