Credit Suisse has a note today on the Newscorp split:

Action: We upgrade our NWS.AX TP to A$42 per share ahead of the split on 28 June 2013. Our TP is based on US$6 for new News Corp (US$24 post split) and US$34 for 21st Century Fox. In this paper we assess the earnings potential, valuation, risks, potential acquisitions, organic growth opportunities and capital management for new News Corp and 21st Century Fox. We retain an OUTPERFORM rating on NWS.AX heading into the split.

■ Investment Case: Good entry price for two dominant multi-media businesses with strong growth prospects, accumulate new News Corp on weakness post split. Our new News Corp investment thesis is shaped by the following considerations: 1) New News Corp will have a diverse asset mix of strong growth assets in pay TV and digital which will more than offset its structurally challenged assets in print and IMS (and allow investment to reposition print). 2) We see the potential for further acquired or organic growth not captured in our current valuation (such as a potential international acquisition by REA or improvement in Amplify). 3) We expect strong free cash generation and an attractive dividend. The US$500mn buyback is likely to provide a base level of support to new News Corp post split. Our 21st Century Fox investment thesis is shaped by the following considerations: 1) Fox is well positioned as premium content becomes increasingly valuable and pay TV penetration increases in emerging markets. It has a solid sports rights portfolio and is the market leader in key international markets. 2) We expect Fox to deliver the highest EBITDA growth among US media peers over the next five years due to strong growth in affiliate and retrans revenues.

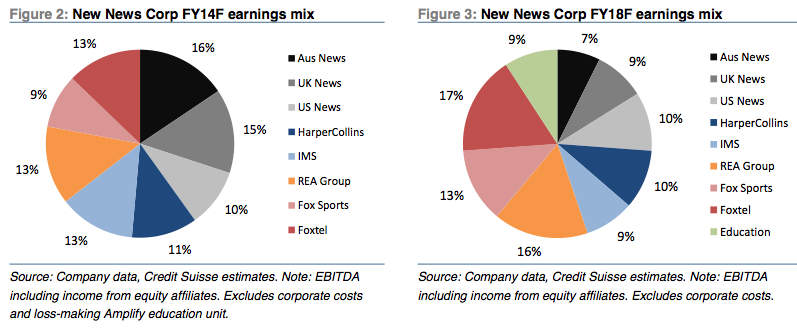

New News Corp

We value new News Corp at AUS$6 per share pre-split (equivalent to US$24 post split given the one-for-four ratio of the stock dividend). Although the stock is likely to face some pressure immediately post split as the shareholder base turns over, in our view there is significant scope for a re-rating of new News Corp away from a presumed ‘publishing’ multiple as investors become more familiar with the high growth assets contained within the new company. Our valuation implies New News can trade at ~8.5x adjusted EV/EBITDA on FY14 estimates.

21st Century Fox

We remain positive on 21st Century Fox based on our favourable view of its premium sports exposure, international growth opportunities, declining ad exposure, and potential upside to capital returns. In our view the company is likely to see further multiple expansion post-demerger as its conglomerate discount is reduced by the removal of the slower growth publishing assets. Overall, we are making minor estimate changes and raising our standalone DCF-based valuation US$4 to US$34 per share. This implies that Fox can trade more in-line with Discovery on ~11x EV/ FY14 EBITDA.

Investment Risks

■ Worsening macroeconomic conditions (in Australia, U.S., or U.K.) could impact New News given high exposure to advertising.

■ Secular challenges in print media have pressured both circulation and ad revenue. New News’ ability to stabilize these declines by moving to digital remains unknown.

■ Potential for dilutive M&A since we expect New News to be active given its cash position and investment needs.

■ Voting rights remain concentrated with the Murdoch family, an overhang that has historically caused NWS to trade at a discount. We apply a 10% ESG discount to our valuations for both 21st Century Fox and new News Corp based on governance concerns.

■ Both companies remain exposed to litigation risk at the UK newspaper business (given that 21st Century Fox’s is indemnifying new News Corp against costs related to civil claims).

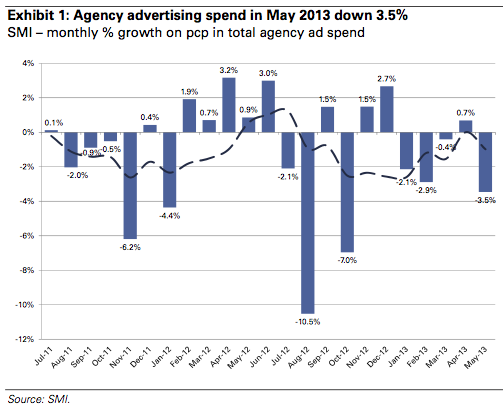

Note the big exposure to the Australian advertising market via print, Foxtel and realestate.com.au. Goldman yesterday released advertising buying data for May and it showed advertising bookings for May under pressure (as we know, marketing budgets go first when an economy softens):

Advertisement

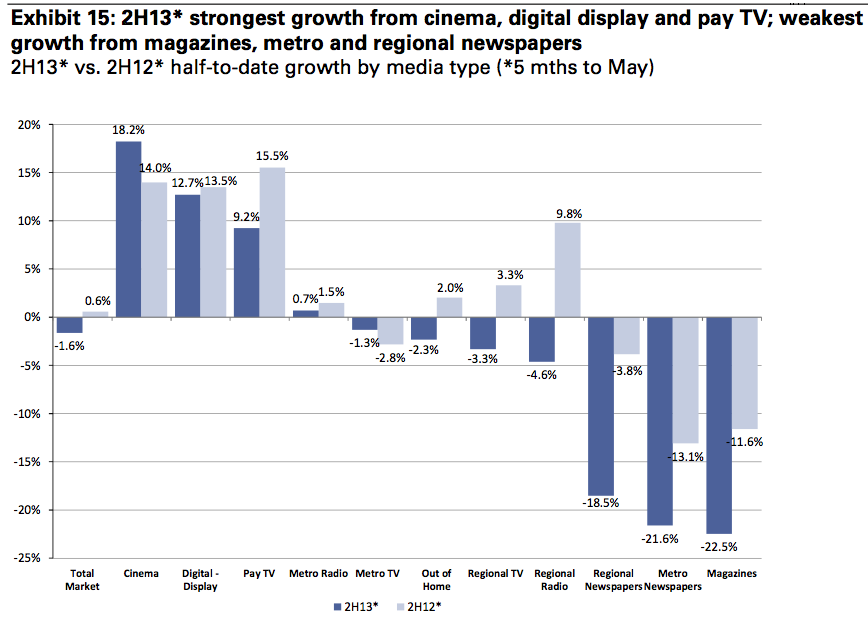

However, pay TV fared better in H1:

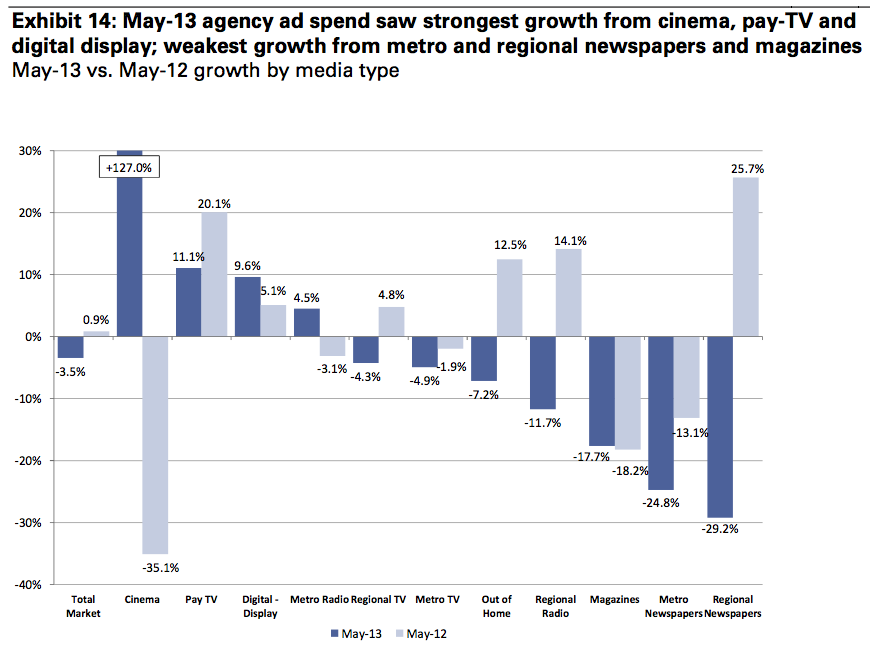

And is forecast to do so in H2:

There’s no getting around it, though. The new Newscorp is a serious bet on the Australian economy pulling off a smooth rebalancing trick. I have my doubts.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.