It’s sobering to recall that the Rudd government fell behind the Coalition in the polls only once during the RSPT debate. Compare that with the subsequent Gillard government, which managed to flop over the line with a minority government and has badly lagged the Opposition ever since. One can only wonder how Labor strategists sleep at night knowing that they deposed a leader on flimsy polling grounds only to entrench a far worse opinion of the party.

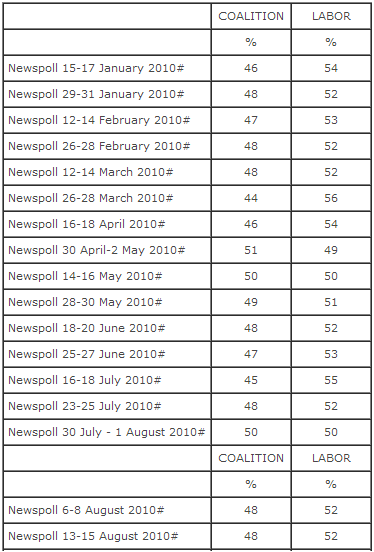

Second, it is pretty obvious that Rudd was rebounding from the RSPT debacle when he was deposed. The April through June 2010 series of two party preferred polls are 49, 50, 51, 52 and rather suggest that Rudd was winning the debate. Despite the extraordinary bias of the Australian business press against the policy, his polling had returned to pre-RSPT levels and was trending upwards.

Third, it is remarkable how this fact has been whitewashed from history (including by me in the above list). The propaganda has been so overwhelming surrounding the tax and the coup that we have all forgotten that Rudd was actually strengthening his electoral position when he was tossed out.

Thus, in the cold hard light of history, Rudd’s overthrow should be seen as an act of political bastardry not electoral necessity.

If that’s the case then it behooves us to contemplate the counter factual case of Rudd persisting in the job. Treasury estimates comparing RSPT and MRRT revenues into the future have shown a difference between the two taxes of as much as $100 billion dollars over ten years. There are higher estimates around as well. Is that the price we paid for a regime change that we neither wanted nor needed?

Probably not. Rudd was also negotiating with Andrew Forrest at the time of the revolution and the outcome of that would still have watered down the tax, presumably more to the advantage of FMG than the big boys. I nonetheless think it fair to suppose that that outcome would have been more advantageous to tax-payers than the sell-out document authored by the three big miners and rubber stamped by Gillard.

The other significantly reduced cost would have been the smaller tear in the fabric of Australia’s political economy. Gillard’s ascension declared loudly to every business in the country that rent-seeking was the new law of the land and although Kevin Rudd’s nanny state was encouraging similar behaviour, it was not with so loud a trumpet.

Basically. Gillard took power in a union coup that she has never been forgiven for. Other factors contribute to her unpopularity of course. But this is the fundamental hook upon which all other perceived errors hang.

Advertisement

Fast forward to today and Kevin Rudd has played a game of refusing to do that same to Gillard. He knows that Labor’s best chance of resuscitation is for the Party to implicitly acknowledge its mistake and ask him to return. Anything else will hit the Labour brand again. If Gillard steps aside then a wrong has been righted, underlined by the moral method of Rudd’s return.

It might be argued as well that it’s in the national interest for Gillard to step aside. As we approach the mining investment cliff, we need a new set of policies that Gillard is unable to deliver. Tim Colebatch has more today:

The Reserve Bank of old had a rule of thumb to focus on the biggest risk we face. Goldman Sachs chief economist for Australia, Tim Toohey, estimates that the risk of recession ahead is now 20 per cent, with the biggest risk in the first half of 2014. That is the biggest risk we face.

To cut to the chase, the Reserve faces the choice between risking recession or risking inflation. If we’re lucky, we might escape either. If we’re unlucky, we might get both: a dollar that plunges as a result of the economy sliding, resulting in high (imported) inflation at a time of stagnation or recession, when it is impractical to raise interest rates.

One way or another, by policy choice or market pressure, the dollar is going to fall a lot ahead, as mining investment subsides, and – you hope – the global economy finally gets its mojo back.

That will make our producers competitive again; it’s what we want to happen. But it will have unpleasant side-effects. A lot of things we now take for granted will become more expensive, maybe much more expensive.

The holiday in Europe we were planning could cost 20 per cent more, and become unaffordable. Petrol will be much more expensive. So will all the imports we buy: cars, computers, mobile phones, household goods, food and clothes.

Until now, the high dollar has made the Reserve Bank’s job easy by making imported goods cheaper. When the dollar falls, they will become more expensive, and inflation could rise well above the Reserve’s target zone of 2 to 3 per cent.

Prominent economist Ross Garnaut and Treasury secretary Martin Parkinson say the Reserve should ”look through” the inflation bubble created by the dollar’s fall rather than lift interest rates to combat it. But, with no other policy levers to restrain wages and prices, it’s not clear how the Reserve could be sure that higher import prices would not spark a new wage-price spiral.

The smart move would be to bring the dollar down now, when Australia’s standing is high, rather than see the market drive it down because Australia has gone pear-shaped. But to do that, the Reserve needs the government to put in safety fences, and tell Australians why they will have to accept rising prices without rising wages. Only a new leader could do that.

Advertisement

And only a new leader can break down the union hacks that back Gillard and stand in the way of this sensible platform.

There are many variables here. There is no guarantee Rudd would do any of this, either. He tends towards nanny state thinking and if he resumed the leadership may simply start talking stimulus. The three key independents may not want to go along for the ride. There is no obvious replacement for Wayne Swan, who would have to go as well. And the high probability is that Rudd would lose anyway.

But if it happened, it would outflank the LNP in policy terms and force the debate onto the territory that the nation needs it to occupy: how would our respective candidates for government each address the end of the mining boom differently?

Advertisement

It is more natural territory for a reform-minded Labor Party than an austerity-driven LNP.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.