Deutsche Banks’ China economics analysts are pondering why their forecast for 8.5 per cent growth next year is well above consensus (and even well above the IMF’s 7.7 per cent and the World Bank’s 8 per cent).

They have come up with a list of reasons why everyone else might be overlooking some positive possibilities for future economic growth. We’re not sure if we agree, but bear with us (haha) anyway.

Advertisement

The broader argument is that China is just experiencing a cyclical slowdown, and one that will be alleviated by things like a return of export demand from the US and EU later this year, receding temporary factors such as the corruption crackdown and bird flu fears, and of course the “possibility of some policy easing”.

The DB analysts, Jun Ma and Michael Spencer, go on to list a number of possibilities for stronger growth that have been overlooked. They start by using a ‘potential growth’ argument, starting with trying to figure out what the country’s output gap might be. Given the lack of good employment data from China, Ma and Spencer had to come up with another way to estimate this:

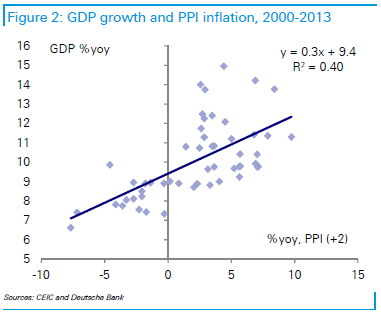

Since 2000, PPI inflation has averaged 2.1%. If we take that as a “normal” rate of inflation, then the historical relationship between GDP growth and PPI implies that “potential” growth could be as high as 10%. That relationship between growth and inflation has been stable over the past 15 years.

Advertisement

They point out that Chinese inflation lags growth by two to three quarters, and that using CPI data would give a similar result. We’re really not sure if the causal relationship is on their side, here. They don’t sound too sure, either:

This is not an especially scientific method, but we think is sufficient evidence that the growth in China has been below its potential growth rate for nearly two years. Having said that, we do agree that China’s potential growth rate is probably slowing. Economists know embarrassingly little about what determines potential growth – consistently the most important determinant of growth potential is the gap between GDP per capita and GDP per capita in the advanced economies. That is to say, the further an economy is from the production possibilities frontier, the faster it is likely to grow as it ‘catches up’ with the more advanced economies.

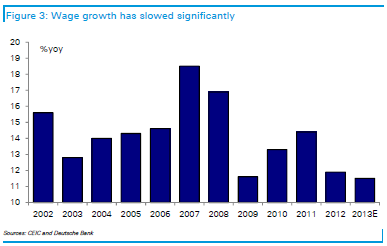

Wage growth has slowed (although still faster than GDP growth; and productivity gains would probably be required to offset that).

Pollution policies would be a net positive (especially by lengthening life expectancy in the north), but this could be quite a while away. As we saw from Ma’s interesting research on pollution risks and policies in March, there’s a big cost in the near term — but Deutsche merrily argues at the end that it will all be okay because the country will transition to a more service-based and less energy-intensive economy, just like the UK did before it. Which is something of a contradiction because that very transitionisn’t compatible with the sorts of high single-digit growth rates that Deutsche is predicting.

Advertisement

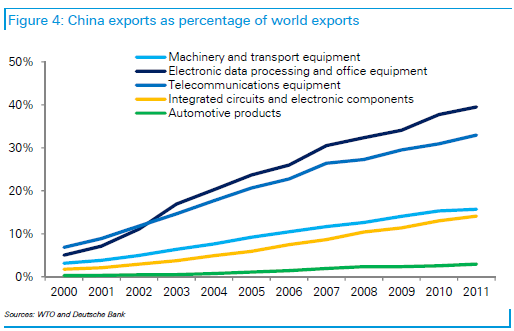

They also argue that China is moving up the value chain:

We’ve seen, however, that this is not showing up in trade data — both exports and imports slowed much faster than expected in June. Ma and Spencer

Advertisement

Finally, they are optimistic about debt. Local government debt growth has slowed. Fine, but remember, three-quarters of maturing local government loans were rolled over at the end of 2012, so it would be frankly alarming if it was continuing apace. Ma and Spencer argue that there can and will be a ‘fiscal resolution’ to the problems of debt incurred by local government financing vehicles. We pointed out last week that the central Chinese government does indeed have some resources to manage and contain debt crises. The question is whether that can go on for long enough that other forms of growth will take over.

It kind of works if one makes the following assumptions:

You discount the possibility that credit growth could be reaching limits

You predict that export demand will return to previous trends

You disregard the idea that China’s economic imbalance means continuing high rates of growth are unsustainable.

Advertisement

On that last point, there seems to be a lack of consistency in this approach. They seem to agree that the economy needs to rebalance — judging from their comments on pollution and the importance of addressing “unreasonably low interest rates on deposits and loans that force households to save and encourage everyone to over-invest”. Yet they don’t address how high growth can be maintained while investment inevitably slows as a contributor to GDP. Plus, they point out that investment growth has been maintaining a fairly steady growth rate and is even strengthening of late. That doesn’t help rebalancing, either.

There are certainly some interesting arguments here. But is difficult to argue that the slowing demand for exports will reverse strongly, or that a likely weakening of China’s international labour market arbitrage advantages will be addressed, along with falling return on capital and massive barriers to allocating investments in ways that will boost productivity.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.