Cross-posted from Kate Mackenzie at FTAlphaville.

The short answer: the June trade numbers missed expectations by a long way, and the details did nothing to provide reassurance. Here’s a long-ish term view, courtesy of SocGen:

Coming so soon before the Q2 GDP data, which is due next Monday, the data have raised the possibility — noted by the FT’s Simon Rabinovitch — that China might actually miss its growth targets for the first time in 15 years.

The 3.1 per cent contraction in exports, compared to June 2012, was in stark contrast to expectations of 3.7 per cent growth. Imports fell by 0.7 per cent and expectations were for 6 per cent growth.

Some of this could well be due to the crackdown on mis-invoicing, used to disguise illegal capital flows, which had been artificially boosting trade data and which SAFE cracked down on in early May. Last month’s trade data showed, for example, that exports to Hong Kong — one of the key destinations for the invoicing ruse — were down 7.7 per cent. This month, exports to Hong Kong fell 7 per cent. US-destined exports also fell more than in May, but exports to Japan and Europe were slightly better compared to May (albeit both were still negative year-on-year).

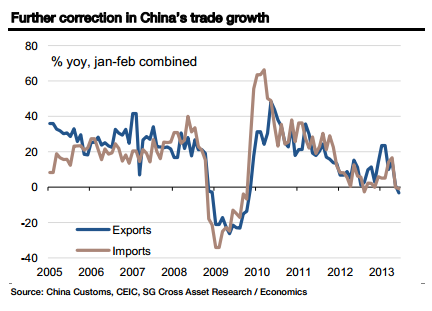

We could expect the year-on-year monthly figures to be affected by the baseline effect for June, and for many months to come. However there’s a few reasons why this doesn’t offset a picture of declining trade. The first is that we like to think that the clever people responsible for the consensus forecasts would have factored this into their estimates. And although the trade data for “special custom zones” like Hong Kong and Taiwan began spiking about a year ago, the effect wasn’t huge until late 2012 and early 2013:

[Update, moving goods in and out of the special customs zones on the mainland was a way of overstating exports to make a carry trade on high yielding WMPs – without even having to export the goods. But Hong Kong and Taiwanese destination data from the Chinese trade figures show a similarly strange pattern, for similar and otherreasons.].

Meanwhile the sequential data from May to June — which would presumably remove most of the effect of the fake invoicing — is even worse than the year-on-year change. From Simon, again:

Compared with the previous month, China’s June trade figures were even more anaemic. Exports shrank 4.6 per cent from May, while imports decreased 9.3 per cent, according to the customs administration.

Finally, let’s take a closer look at the import data. Year-on-year imports fell much less than exports — just 0.7 per cent — and, like exports, the yoy number is probably worsened by the baseline effect of the clampdown on fake invoicing. Apart from that, the news is not much better.

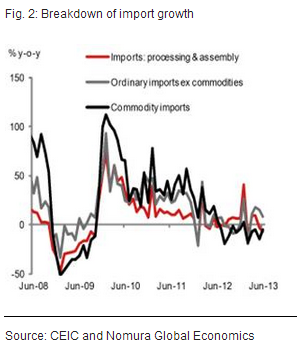

China’s import data is helpfully divided into ‘ordinary’ and ‘processing’ — the latter means goods that are assembled in China for re-export. Both categories are significant; the ‘processing’ numbers hint at what’s to come in exports, while the ‘ordinary’ numbers give an idea of how domestic consumption is faring. Both, again, showed a big decline in the year-on-year data. Imports for processing and re-export were -7 per cent in June, compared to -3.2 per cent in May. Goods for consumption (ex-commodities) grew, but at only 8 per cent in June, down from 15.2 per cent in May.

One last thing: there may, in fact, be a small sign of growth within the June trade numbers. Commodities imports, another category separate from processing and domestic consumption, fell only 5.2 per cent, much less than the -14.5 per cent in May:

Here’s Societe Generale’s Wei Yao:

Imports of crude oil and copper were growing again yoy, in both value and volume terms. Declining commodity prices were probably one major factor that revived China’s commodity appetite. We still wait for more data to confirm if such a recovery does suggest any genuine improvement in investment activity.

Whether resurgent investment activity is a good or bad thing might depend on whether you are looking at the short term or the long term (ie, rebalancing).

Yao makes a point that this has implications for the renminbi:

In our view, one key policy take-away from this trade report is probably that the strength of the yuan can hardly be justified. Also as capital inflows are curtailed, the balance in the currency market should tilt towards yuan depreciation.

Nomura’s Zhiwei Zhang believes the GDP figures next week could be a testing time for the government’s nerve, in terms of slower growth:

The government will likely hold a meeting early next week to set its policy stance for H2, which is critical for the growth outlook. So far, it has sent consistent signals that the policy stance will remain tight to contain financial risks. As macro data weaken further, next week will be a testing time for the government in revealing just how much of a growth slowdown it is willing to tolerate.