Three reports today from the “official” economic analysis sector show two things: the mining cliff is upon us and that if you wait to be told such things by consultants your ship will be sunk before you’ve been advised to batten down the hatches.

The first is the illustrious Deloitte/Access major projects report which has finally registered that it’s not all good after all. From the SMH:

The mining investment boom is winding down sharply, with the next few months set to be a turning point for the Australian economy, a report by a leading business advisory group has found.

The value of planned projects, those under consideration or possible, fell 14.3 per cent, or $68.3 billion, from the last quarter, said Deloitte Access Economics in its Investment Monitor June-quarter report, published on Tuesday.

The total value of resource projects in the researcher’s database slipped for the second straight quarter, the first time that has occurred in a decade. It dropped by 5.6 per cent from the first three months of the year to $877.1 billion. Mining projects for the quarter were down 4.7 per cent from a year ago.

The value of definite projects that were under construction or committed grew 3.7 per cent to $468.1 billion, the highest on record.

”The profile of work in the Investment Monitor database suggests a peak in activity through 2013-14 is likely,” Deloitte Access Economics partner Stephen Smith said in the report. The database contains 947 investment projects with a total value of $877.1 billion.

”Still, the value of work in the pipeline remains remarkable. At almost $200 billion, there is scope for a further lift – a last hurrah – before the peak.”

Advertisement

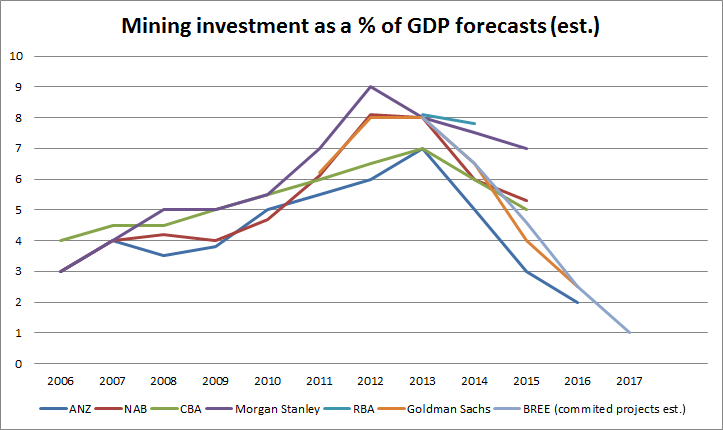

Nope. No last hurrah. The Roy Hill vanity project and perhaps a watered down Arrow LNG are the only two that I can see proceeding. That would slow the decent a bit but that’s all. Here’s the chart you’ve had at MB telling you what’s really going on:

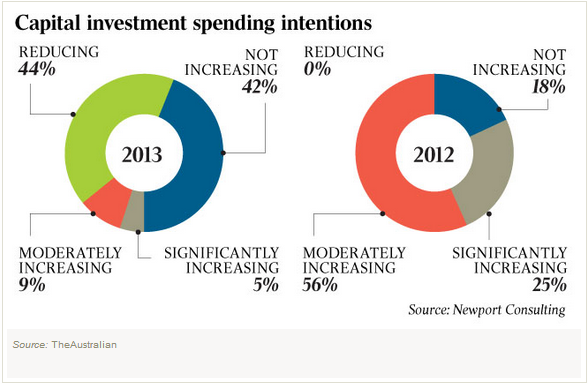

Another consultancy, Newport, is out with its annual survey of mining insiders and it discovers an ugly picture:

Advertisement

CONFIDENCE in the mining sector is in “free fall”, with top executives displaying a gloomy outlook and slashing capital expenditure, an influential report has warned.

The 2013 Mining Business Outlook report by Newport Consulting has revealed a sharp negative shift in sentiment among industry leaders over the past year. It is also the first time in the report’s four-year history that miners have declared they are reducing capital expenditure — not just postponing or moderately increasing it.

A key driver for the spending halt was the uncertain economic climate. The report warned that if that hold on investment continued, Australia would reinforce its status as a less attractive investment destination.

It’s important to be influential. But not so late the game.

Meanwhile, the eternal bull of economic consultants, BISShrapnel is out with a mea culpa – well, not really – pushing its dwelling construction boom out another year :

Advertisement

The report came as a survey by industry researcher BIS Shrapnel said the transition away from mining-led growth towards other sectors such as building construction was expected to be ”uncomfortably slow” and a ”real nail-biter”.

The forecaster said total national building starts were expected to grow at 3 per cent in the 2013-14 financial year and a further 3 per cent in 2014-15.

Home construction was seen as not responding to lower interest rates as was expected, with a mixed outlook for the states and territories likely to lead to dwelling starts falling by 2 per cent in 2013-14. Residential construction was expected to grow 9 per cent in 2014-15 and 4 per cent in 2015-16.

It’s interesting to look back a year or so to compare:

Across the country new dwelling construction growth is forecast to dip by 13% in 2012 but will wipe out this deficit in 2013 with a 13% gain.

Housing construction will rebound by 12% in 2013 following an 8% dip in 2012, while units will rebound by 15% in 2013 following a 15% drop in 2012.

In its report, BIS Shrapnel says household income growth has slowed over the past couple of quarters, but still remains solid.

“We expect it to start increasing again through the second half of 2012, driven by higher wage inflation and a return to employment growth,” the report says.

…“We expect the annual rate to drift down to around 6% by the end of 2012, before it accelerates again. This will continue to support solid growth in household spending.”

BIS Shrapnel forecasts an average standard variable mortgage rate of 7.4% in 2012, rising slightly to 7.8% in 2013.

Advertisement

Official forecasts have served all well for many years. But the economy has changed much faster than yesterday’s star prognosticators seem able to.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.