Is it just me or was the price action in gold and the US dollar over the first day of the week and the data from Japan a little sign that maybe a safe haven trade might be gaining a bit of traction once again.

Lets think about what we have to drive this type of trade and whether or not I’m just ex-poste rationalising to fit the price action:

- The Fed signalled last week the taper is coming this year. Maybe next month but certainly coming unless the data weakens.

- Stocks have been unable to kick on with the new highs they are setting for themselves and these highs have been gained on the back of weak volume

- There is open questioning of when the decline will begin or like this morning on MarketWatch a question of whether it has already begun

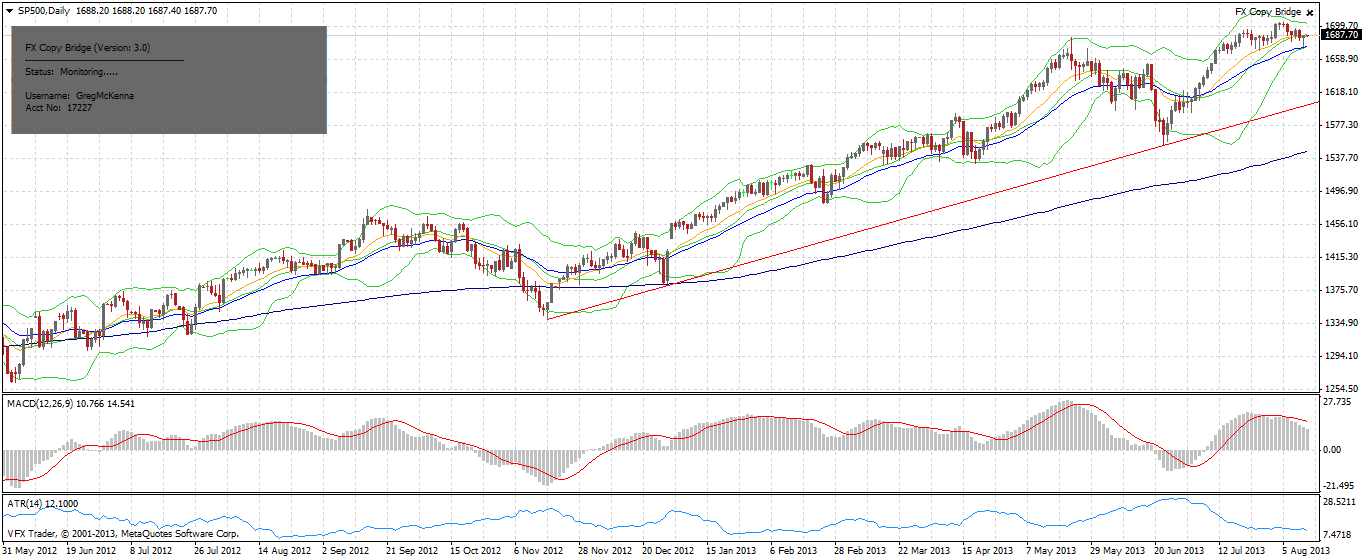

- My S&P 500 cahrt looks like it wants to go quite a bit lower and the long I got stopped into 3 or so weeks ago is a couple of points away from being stopped out of for no gain.

- The rally is coming from margin expansion in PE ratios not earnings

- Bond’s can’t rally in the US and are looking vulnerable to QE

I reckon there is a retracement coming and I reckon it is going to be good for the US dollar and gold particularly as measure in terms of other tradeable assets.

The key to all of it is the S&P 500 and based on my technicals its is going to retest 1670 again soon and if it gives way we have a 50 point move in the offing and then we’ll see if the trendline support holds. Of course it should and we respect trendlines (ones with at least 3 touches) unless or until they break.

From where I sit I reckon the needle moved a little more toward fear in the past day or so – time will tell.

Looking at overnight price action the US dollar was generally stronger gaining 0.26% against the euro which is at 1.3303, 0.25% versus the pound sitting at 1.5463 and 0.5% versus the Aussie dollar 0.9130. Against that the yen it is up 0.8% at 97.10.

Indeed as I note above if you look at that yen move, the US dollar generally and the move in gold (+1.66% @$1336 oz.) you get a sense that the weaker than forecast GDP which came in at just 2.6% annualised with a still negative deflator and with weak industrial production and capacity utilisation released later in the day, I reckon you can see a bit of a fear factor in markets with the weaker growth in some jurisdictions yet chances of taper in the US as early as next month top of mind.

Looking specifically at the AUD I ask if there are there any EliottWavicians out there? Because you might be seeing in the AUD a nice set up for the 5th wave higher if the four hour chart is any guide. I confess to not being much of an Elliott waver but there are some very strong similarities between Elliott Wave trading and the kind of Fibonacci retracement and projects that myself and many others practice.

I have put the Fibo levels on what you might call wave three and we are probably in wave four on this move with a five to come – maybe. But there are some really big key levels to watch.

0.9104 is the 38.2% retracement of last weeks big move and a reasonable level for the Aussie to get back to and still have a topside bias as the dailies suggest it does. Below that 0.9067 is the 50% level. Topside if the Aussie can, big if but if it can, get through yesterday’s high at 0.9219 then we are heading back to the top of the box at 0.9333.

My view is we’ll see this move into the low 91 region and then we’ll see if there is decent support down there.

On stock markets at the close the Dow (-0.04% @15,420) and S&P (-0.14% @1689) were both marginally lower while the Nasdaq (+0.27%) was up a little. In Europe Frankfurt (+0.25%) and Milan (+0.44%) were both higher but the FTSE (-0.14%), CAC (-0.11%) and IBEX35 (-0.2%) were all lower.

As noted above, on commodity markets gold was higher but it was silver that had another huge day rising 4.57% to $21.38 oz. Copper was quiet but the Ags continue to prove Mandelbrot right, volatility begets volatility with Soybean jumping 2.46% while corn rose 1.02% but wheat was a lot more circumspect rising just 0.16%

On the data front today my favourite indicator of the Australian economy in the NAB Business survey is released but before that we get that the BoJ minutes and Japanese machinery orders. German CPI and PPI is out along with similar data in the UK and Spain before the EU IP and German ZEW data are released. In the US its retails sales, business inventories a speech by Dennis Lockhart and import and export prices.