From the AFR today, Warwick McKibbin appears with new evidence for the argument I put earlier this week that Australia’s fiscal strategy should shift away from the cuts and surpluses of Howard/Costello and towards an outcome focused on spend quality.

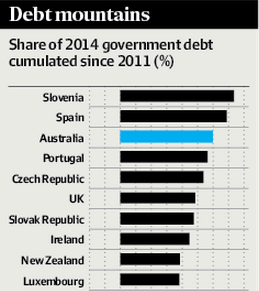

McKibbin acknowledges Australia’s low stock of public debt before offering the following chart which expresses the:

…debt forecasted by the OECD to be cumulated by all OECD countries during the period 2011 to 2014, expressed relative to the stock of debt forecasted by 2014.

McKibbin points out that so long as the rate of return on the spend exceeds the cost of borrowing then the debt stock doesn’t matter (the new debt is self-liquidating). But, he concludes:

Advertisement

If a government has consumed the funds generated by the borrowing then clearly taxes have to rise to pay off the debt. There is no other source of revenue available. If there was little investment of the borrowed funds then there is no way to finance the debt except higher taxes, with all the problems that generates for fiscal drag and negative incentives in an economy. This is the problem that Australia faces.

As we know, McKibbin has previously endorsed borrowing to build infrastructure as a way of bridging the mining investment cliff. He is right. Don’t cut spending, change it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.