Another “business leader” – those who specialise in group think – has declared that the dodgy economy is all the election’s fault:

WESFARMERS boss Richard Goyder is hoping the federal election will usher in a new era of pro-business policy that recognises it is companies that create wealth and jobs.

Speaking after the parent company of Coles supermarkets reported a net profit of $2.26 billion for the 12 months to the end of June, Mr Goyder said he was hopeful that an end to political uncertainty would help buoy consumer spending after the election next month.

“Interest rate reductions have helped, and getting the election out of the way will help,” he said.

“I just hope that towards the end of the year we start to see some improvement in consumer confidence, but who knows? A lot will depend on the external environment, I think, beyond Australia.”

But he said the key to improved economic performance was a stable, pro-business government.

“For the country, the best thing that can happen in government — either federal, state and in some ways local — is leadership which is long-term, which is fiscally responsible, where there’s an acknowledgement that the wealth creators in the economy are the businesses,” he said.

This would foster “an environment that allows business to thrive and in doing so, invest in infrastructure, the community and people”, he said.

Wesfarmers’ result yesterday missed on every metric and it can’t think of anything better to do with its capital now than give it back to shareholders (who can get 4.5% in the bank) so it’s more than fair to put Goyder in the same camp as Virgin boss John Borghetti, both of whom appear to be hiding lousy results behind the election.

Is there actually any evidence for the conventional wisdom that the election will trigger a resurgent economy? A little but most points in the other direction.

In the positive corner we have improving global growth and a little bloom in commodity prices, as well as rate cuts, local house prices and the election result itself.

On the first, there is solid improvement in developed economies – Europe, Japan and the US – but it is equally clear that some of this growth is either taking from other economies (in the case of Japan taking market share from other North Asian exporters) or is likely to fall back as monetary policy begins to normalise (in the case of the US)

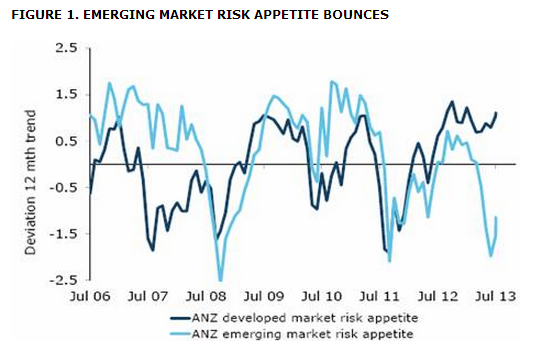

Anyway, emerging markets are far more important to commodity prices and with China set to continue its structural reform, the great supply response reaching a head, and the US dollar likely to firm on slow monetary tightening, commodity prices will continue to fall away. The ANZ runs a series of leading indicators that captures the divergence nicely:

That leads me to believe that local rate cuts and house price gains are up against it. There appears to be enough momentum in housing markets to carry price gains into next year, and with the Spring season approaching, things may even accelerate. But the structural shift in consumer saving is likely to continue , especially as unemployment keeps rising, so these house prices are unlikely to offer more than a modest boost to consumption and growth. The dwelling construction recovery will also help modestly next year. But in the meantime both of these will prevent sharper interest rate cuts and a much needed rapidly falling dollar.

The election itself could lift spirits a little. But how much, really? As the new Abbott government enters power, it is banking on tax cuts to revive the economy but I don’t see them working as stimulus, either. Scrapping the carbon tax will not lower utility prices. I doubt it will lower many prices at all given the redress to climate change will go on and those businesses effected have every right to expect greater costs anyway. They will keep the greater margins. The mining tax cut will do nothing for growth. The company tax cut will help, though not for big business, which will be giving it back for paid parental leave policy.

With the Greens still likely to hold the balance of power in the Senate, Abbott will have to go to a double dissolution election to repeal both taxes, delaying them anyway. Exactly how is going through all of this, all over again, going to boost the economy?

There is greater scope for a growth boost in infrastructure. If the Abbott government pursues innovation in public private partnerships to get us building much needed roads, rail and ports.

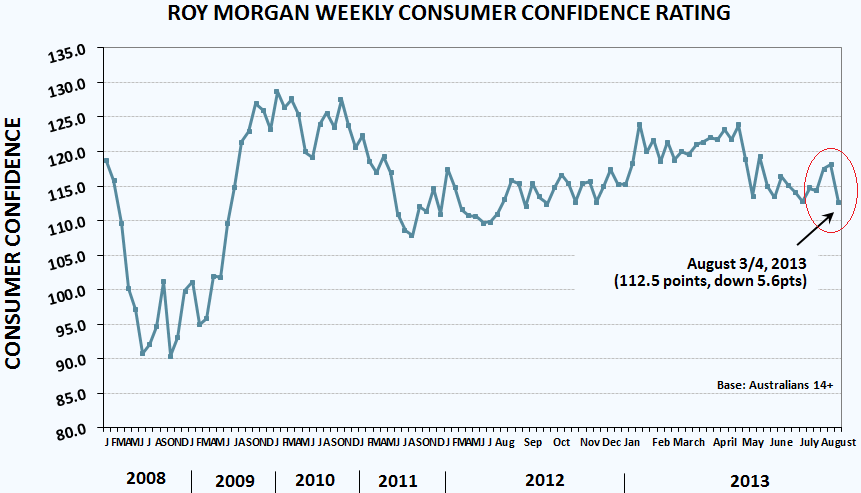

But all of these positives will be dragging the anchor of the yet to be announced fiscal cuts. Abbott has promised a better bottom line than Labor and lower taxes meaning he’ll have to come another $20-30 billion in savings from his current position. As well, who would bet against the new elected Abbott government discovering a few more Labor “black holes”, which may or may not result in further cuts, but are unlikely to boost confidence. This week’s Westpac consumer sentiment saw a lift on the last rate cut but it was conducted before Labor’s Economic Statement, which was just such a black hole revealing process, and hit confidence hard according to the more frequent Roy Morgan measure:

And that’s before we address any further fiscal instability as the terms of trade fall.

So, what are the negatives then? I’ve run through most already. But the big one is the mining investment cliff, which will suck 1.5-2% out of GDP in each of the next three years. As the RBA recently made clear, it no longer sees a plateau for mining investment:

In the third phase of the ‘mining boom’ and post the credit boom, our economic challenges are changing in nature. In the next few years our task will involve supporting, so far as it is in our power, a change in the sources of demand that affect the economy. As resources sector investment declines, other sources of demand need to strengthen, but in a way that is sustainable. The fact that consumption is likely to provide only a modest impetus to any acceleration in domestic demand suggests that other areas will be important. As I noted earlier, at least some of the conditions are in place for stronger trends in dwelling investment and, in time, non-resources business capital expenditure. And exports of resources will continue to pick up strongly.

But successful ‘rotation’ of demand will probably also involve more net foreign demand for other Australian output of various kinds. Given that, the recent decline in the exchange rate seems to make sense from a macroeconomic perspective. It would not be a major surprise if a further decline occurred over time, though of course events elsewhere in the world will also have a bearing on that particular price.

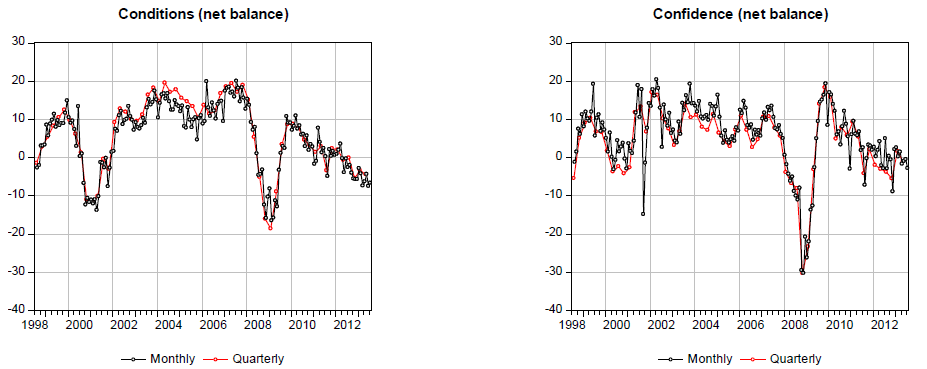

Yes, Glenn, it will take a lower dollar but how is it going to get there without more rate cuts which are being pushed back by house prices? As far as I’m concerned Australia’s domestic economy has already stopped growing. That’s what we’re seeing in the NAB Business Survey:

Accounting entries like net exports prevent the data from showing it but real activity is under considerable pressure, which is showing up in employment in the year on year flat-lining of hours worked.

Following the election we’ll be coming into Christmas and with rising house prices we’ll get ourselves a little retail bounce. And that’s the clear upside risk to these thoughts. That punters loosen the purse strings if house prices continue to rise. Perhaps there is pent-up demand.

But I remain skeptical that the election can boost consumer spending beyond a modest gain given it has struggled since ever since the GFC stimulus was pulled. Without it, it will be impossible to turn a tough 2013 into anything less difficult next year.