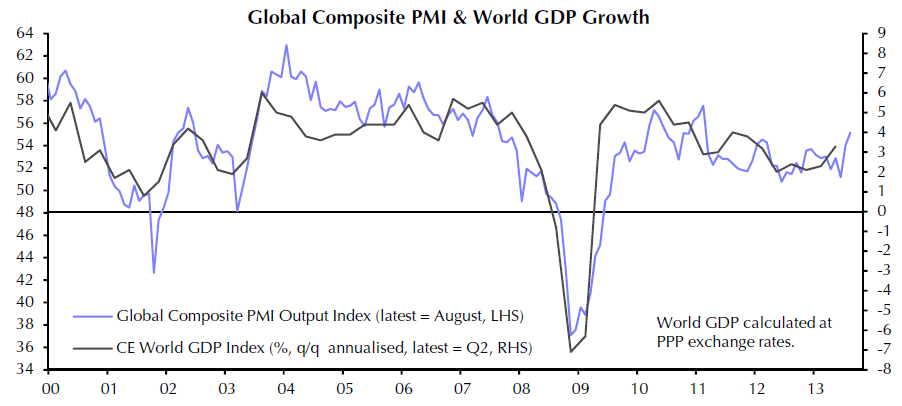

Well, the past two weeks have thrown up enough positive data for me to improve my outlook. As I said earlier this week, there is nothing to suggest the structure of the global and local economies is improved. But there’s plenty to suggest authorities everywhere are generating a cyclical bounce that will have momentum for a while. Starting at the top, here is a composite chart of global PMIs this month from Capital Economics:

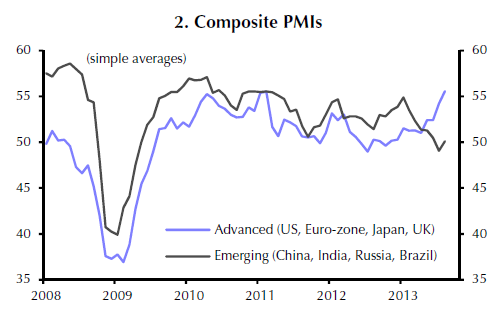

It’s still not tearaway, but it sure is improved and the downtrend in global growth is broken. Moreover, this understates the extent to which developed economies are leading:

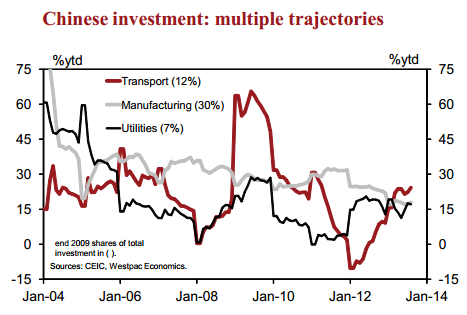

Emerging markets will follow some way behind via their exports and because China too has turned with its mini-stimulus (which is not that small!). It’s now growing comfortably in the 7.5% range via renewed fixed asset investment in transport, environmental improvement and utilities:

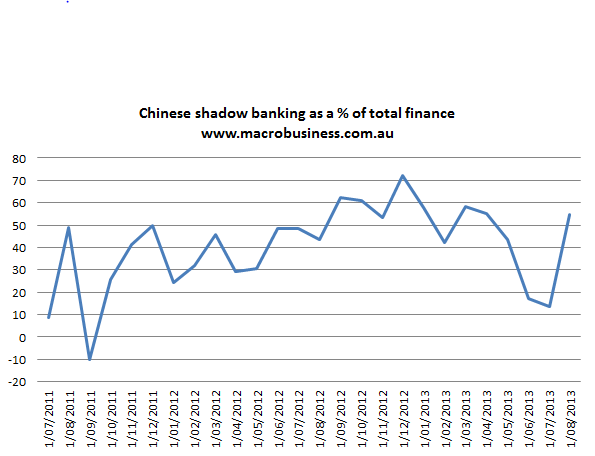

There is nothing sustainable in this growth, as Premier Li Keqiang admits today, and questions about rebalancing and weakening growth will be back as the stimulus winds down through next year but there’s momentum here for now. I remain convinced that China will rebalance to its benefit and our detriment but it is not a story for this year. The dead giveaway is the removal of its boot from shadow banking activities, which have sprung to life after three months of regulatory suppression:

I think it fair to say that the emerging markets bounce will trail development economies by some distance, weighed down by a flight of capital as interest rates rise, but some catch-up can be expected meaning a little more upside in the commodities rally is plausible.

Which brings us to Australia. The capex cliff we have discussed for the last 18 months remains locked in, severe and prolonged, as Morgan Stanley put it. I expect a 1% downdraft to GDP from mining alone next year. As well, the global supply response in bulk commodities is real, huge and and prolonged. Coal will remain weak and the iron ore will come under increasing pressure.

But it would be foolish for me to ignore the strength in the Chinese steel market this year. It’s overshot my projections by some 6% or 40 million tonnes. It’s clearly still overproducing and China is not building any more steel mills but more growth next year is a reasonable bet with a solid stimulus still unfolding, more in the range I expected this year, in the low single digits. That will not be enough to prevent the iron ore price from beginning its long decline. But it may be enough to prevent a rout for another few quarters.

That, in turn, means Australia’s terms of trade hold up better than I feared next year and it means that Tony Abbott’s budget will not require further downgrading after Treasury’s new found conservatism in the pre-election Economic Statement. With the massive jumps in post-election business and consumer confidence this week (bigger than I expected) one has to acknowledge that the political circus of this year has played a role in weakening economic activity as well.

Also, the budget now has $30 billion in deficit spending locked in for 2013/14 and $24 billion for 2014/15. For all the talk of austerity, pollies are simulating their butts off.

With budget instability lifted for a year there is a real chance of a sustained lift in confidence and the appearance of a little pent-up demand. Stocks are also at new highs for the cycle. Housing is bubbling. I expect consumer prudence to persist and the savings rate to remain high, but an easing up in paying down debt may be in prospect, freeing up some extra spending. From yesterday’s Consumer Sentiment release:

We also survey households’ assessments of the wisest place for savings. In September this showed a marked decline in the

proportion of households who see ‘low risk’ options as the wisest place for savings. The proportion preferring bank deposits fell by 4.6ppts to 29.3%. That proportion is now down by 9.7ppts sinceThe proportion favouring ‘pay down debt’ was down 2ppts to 13.8% and is now down by 6.7ppts since September last year. At the same time the proportion favouring real estate rose from 24.6% to 27.5% with this now up by 7.7ppts since September last year. Even shares were marginally more popular, up from 8.4% to 8.8% and up 3.3ppts over the year.

I remain very cautious on real estate. To me it’s obvious that this cycle is far from healthy with first home buyers absent. An investor driven rally smells to me of financial repression, speculation and “weak hands”. This is not a liquid market with ease of entry and exit. Those playing the space are genuine cowboys.

As well, Perth is going to slow and roll, Melbourne has horrible fundamentals, Canberra will get whacked on job cuts, and there’s no under supply in other major cities. Sydney is the core of the bubble now with its genuine supply side paralysis. Could in infect the nation? Maybe, but I’m unconvinced.

The rally in new construction finance is also solid if unspectacular and likely to continue that way. The contribution to growth will be modest to moderate.

This will raise imports and take away some of the expected growth in net exports but it will contribute more to growth than I reckoned a few months ago via consumption. I still expect Australian growth in 2014 at a sub trend pace but above stall speed and the risk of an external shock has receded for the first half. That should keep unemployment from blowing past Treasury estimates of 6.25%.

As for interest rates and the dollar, this is where the story gets sticky. The dollar is not going to fall if these settings play out. Yet it is far too overvalued to engender a genuine recovery in tradables. Interest rates will also be at the bottom, though the RBA will be loath to raise them and will only do so if the house price bounce gets out of control. The RBA’s failure to embrace macroprudential policy is as reckless a move by a central bank that I can recall in a era of reckless central banks.

There are risks of course. If house prices go nuts, we’re in deep shit. Hiking interest rates into the mining cliff will mean recession. The Fed’s taper is clearly slowing its housing market and that will slow the global recovery into next year. That puts at risk its stock market as well. If the Fed tapers it’s going to be very gentle.

There is also the US Congress and its debt-ceiling, Italy’s woes and the German election, as well as emerging market capital flight. But these all look like tail risks to me at this point.

The world has kicked the can. Enjoy it while it lasts.