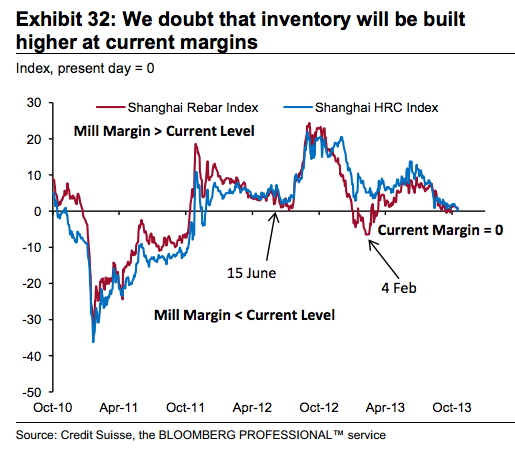

It is worth noting that mills’ margins appear to have retraced to levels similar to those which triggered the Q2/Q3 2012 and Q1/Q2 2013 destocking cycles. Given the importance of seasonality – steel production generally accelerates in Q1 while iron ore is less readily available – we doubt that mills will now run another full destocking cycle. However, it does seem very unlikely that mills will pay up to build inventories significantly higher.

We do not therefore expect rising apparent demand to lift prices. A more likely outcome is for September to have marked the cyclical peak and for steel production to slow into the end of the year; though possibly distorted by the national holiday, CISA’s estimate for the first ten days of October registered a 1% decline from the last ten days of September.

This would allow mills to build inventory cover without substantially increasing their purchasing. At the same time, it would reduce the weight of supply on the steel market, likely alleviating some of the margin compression caused by low steel product prices. Under this scenario, lacking additional strength on the bid, we would expect iron ore prices to ease lower over the coming weeks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.