Earlier this week, FT Alphaville published an article questioning the notion that London housing is in the midst of another boom/bubble, instead arguing that prices may have crashed:

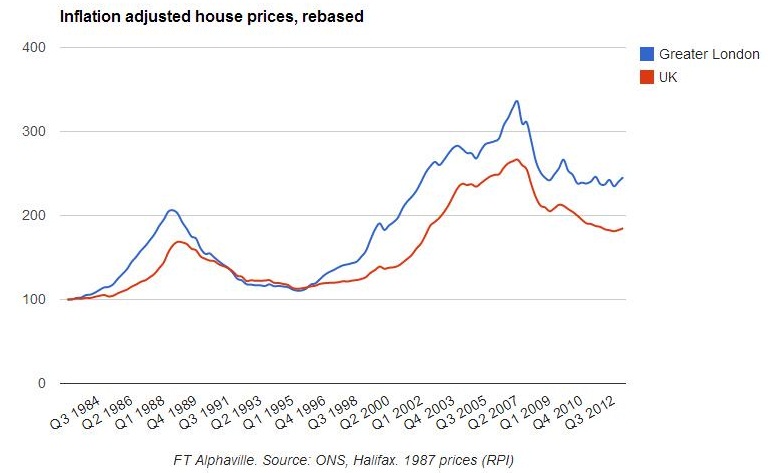

London is in the grip of a terrible and deep housing bust that has only just begun to turn. Greater London house prices, adjusted for inflation, are fully 27 per cent below their peak in the summer of 2007…

Greater London prices dropped 30 per cent, in real terms, before turning at the start of this year. Even though they rose far less in the first place, adjusted for inflation, UK house prices are still down more than 30 per cent from the top in 2007.

Advertisement

Getting a good read on the London (or UK) housing market can be difficult, since the major house price indices that track London/UK house prices tend to differ significantly from one another.

It is interesting to note that the Halifax index quoted by FT Alphaville – a hedonic (quality-adjusted) index based on mortgages issued by Lloyds Banking Group, the UK’s biggest mortgage lender – is the most negative of the major UK house price indices (see next chart).

Advertisement

While Halifax suggests that London house prices were 27% below their peak in real terms as at June 2013, Nationwide (a quality adjusted index based on a different sample) shows them 12% below peak and the Financial Times (aka Acadametrics) index (which is based on average prices from the whole market) shows them at an all time high in real inflation-adjusted terms.

It’s a similar story for the broader UK market, with Halifax again providing the most negative assessment. It has UK house prices 30% below peak in real terms, whereas Halifax has them 25% below peak and the Financial Times (aka Acadametrics) has UK housing 16% below peak in real terms (see next chart).

Advertisement

In any event, London housing is set to heat-up, fueled by a combination of rampant foreign demand and the implementation of the government’s “Help-to-Buy” shared equity scheme for first home buyers and the Bank of England’s “Funding-for-Lending” program, which will continue to artificially increased demand and push against the constipated supply system to further inflate prices.

Of course, with supply highly rigid and unresponsive to changes in demand, London housing (and the UK more generally) is basically a volatility machine prone to boom/bust cycles whenever demand shifts. Certainly this has been the experience over the past 40 years, and it is set to continue as long as the supply system remains.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.