Westpac’s November Red Book is out and paints a fairly predictable picture of a marginally improving intent to consume:

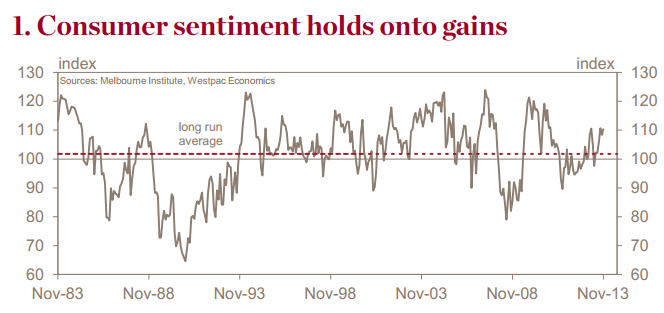

― The Westpac–Melbourne Institute Index of Consumer Sentiment rose 1.9% in Nov to 110.3, a solidly optimistic level.

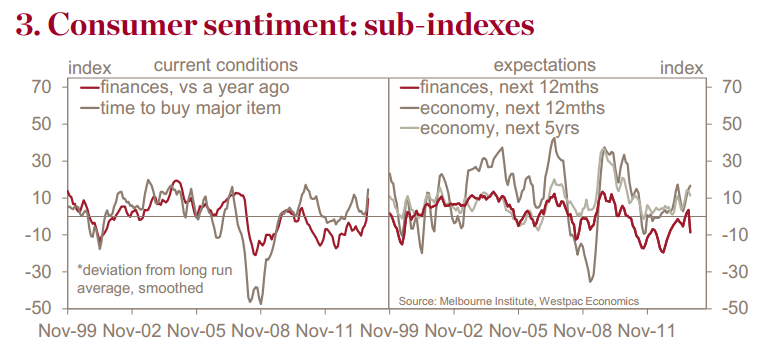

― The rally in sentiment following the Federal election is so far showing few signs of waning. Instead, the survey detail suggests confidence may be consolidating with a marked improvement this month in consumer assessments of family finances vs a year ago. The housing upturn in particular appears to be giving more support to confidence.

― The detail though shows a highly uneven consumer mood. State variations are particularly large, reflecting several influences including the uneven housing upswing (much stronger in NSW) and diff ering exposures to the mining slowdown.

― CSI±, our modified consumer sentiment indicator, which we favour as a guide to spending momentum, posted a 2.2% rise in Nov taking it to a new post-GFC high. It remains consistent with a pick-up in consumption growth to the 3½-4%yr range by mid 2014. While we agree with the direction we expect a more muted acceleration to 2½- 3%yr with ongoing labour market weakness and associated job security concerns a key inhibiting factor.

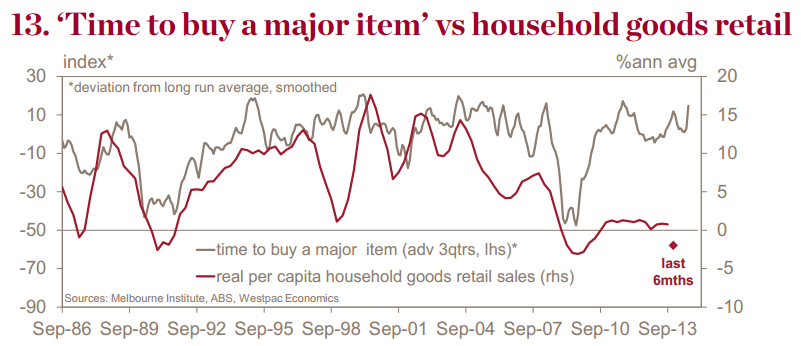

― Consumer attitudes towards ‘time to buy’ remain upbeat with the indexes tracking ‘time to buy a major item’ up 4.4% and ‘time to buy a car’ up 4.7%. Both are well above their long run average. However, the readings are difficult to interpret with continued subdued actual spending on durables and vehicles again suggesting that these upbeat buyer attitudes reflect low prices and the availability of cheap finance rather than an intention to buy.

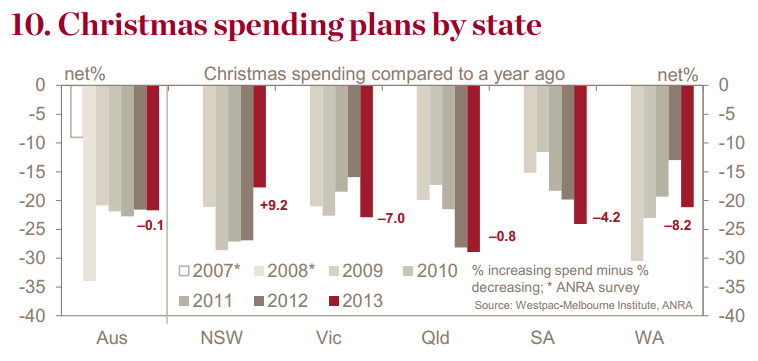

― The Nov survey included an update of our annual question on Christmas spending plans. This showed a continuation of the ‘restrained’ approach to spending plans evident in the last 4yrs with 35% of consumers planning to spend less than they did in 2012, against 14% planning to spend more.

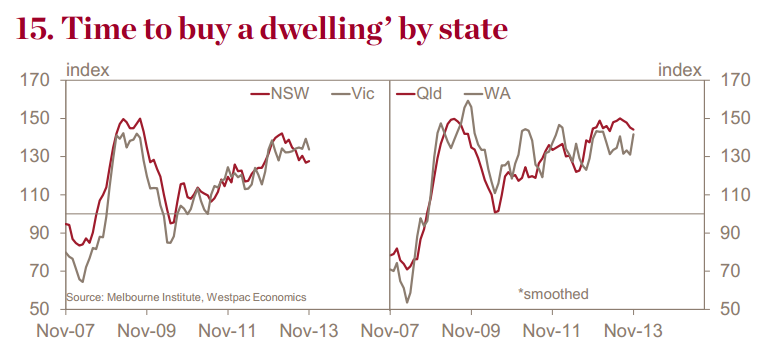

― The index tracking views on ‘time to buy a dwelling’ posted a welcome 4.2% partial rebound from Oct’s surprisingly sharp 10.3% drop. The Index remains at a high level by historical standards although some moderation does appear to be showing through, particularly in NSW where stronger price growth and associated affordability pressures are starting to affect buyer sentiment.

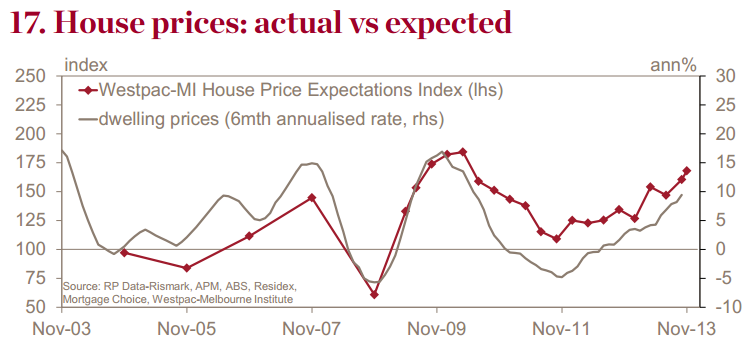

― The Nov survey included an update of the Westpac-Melbourne Institute Consumer House Price Expectations Index which rose from 159.2 in Oct to 164.2 in Nov, a new cycle high but still well below the peak in Apr 2010. Price expectations remain relatively closely clustered. Vic consumers showed the sharpest rise in expectations between Oct and Nov with price expectations more subdued in Qld and WA, the latter still down on its Apr 2013 peak. Note that this Index will now be compiled on a monthly basis having previously been a ‘special’ question run every third month.

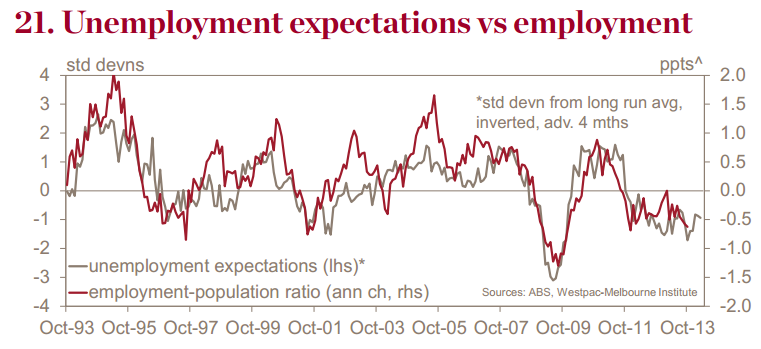

― The Westpac-Melbourne Institute Unemployment Expectations Index nudged up 0.9% in Nov to 144.7, remaining at a high level well above the long run average of 128.8. Consumers continue to brace for a significant weakening in labour markets.

And finally, Westpac’s summation of what it all means:

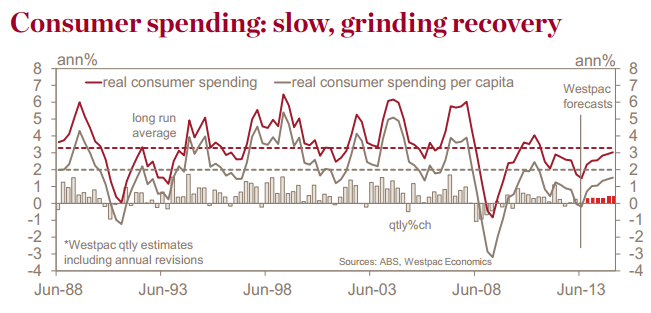

Westpac has got this right, I think. The structural adjustment to lower household consumption growth is very obvious in these charts (look at 13!) and it’s not going to change even with higher house prices easing the tension somewhat.

To translate what kind of contribution that Westpac’s forecasts for consumption will make to GDP, you need to roughly halve the growth figure. I come up with the following GDP guesstimates (not forecasts!):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.