Sigh, the market economists and commentators that dominate our media are losing perspective. Everywhere now the talk is of recovery. Even sensible commentators have been infected. The AFR’s David Bassanese has done a good job over the past year of reading the bearish economic trends and dovish rate environment but no longer! From the AFR over the weekend:

Springtime in Australia is not just causing the flowers to bloom – a range of economic indicators also suggests the green shoots of recovery may be emerging across the economy. After a year of sluggish economic growth and rising unemployment, recent surveys report a big bounce in business confidence after the federal election.

Home-building approvals have also lifted strongly and even retailers had a little more to cheer about last month. And despite this week’s soft employment report, more forward-looking indicators or labour-hiring intentions appear to be bottoming out. Meanwhile, both house prices and share prices are moving higher, underpinning gains in household wealth.

With the mining investment boom turning down, the strength in non-mining sectors such as housing is encouraging, and not before time if we’re to avoid larger increases in unemployment. Financial markets have become convinced the Reserve Bank of Australia has finished cutting interest rates and the next move will be up – sometime late next year. Of course, whether that’s true remains to be seen, as the signs of economic improvement are still tentative.

Indeed, on Friday the RBA cut its economic growth forecast for next year further owing to persistent strength in the Australian dollar – which is hurting exporters – and deeper cutbacks in miner’s investment plans. With Treasurer Joe Hockey warning of a further budget deficit blow out due to weak tax revenues, the RBA also knows Canberra won’t be spending up big next year.

That said, the fact remains that the impact of low interest rates is being felt – slowly but surely – across the economy, and at most the interest rate might only drop a little further next year. The next big move in interest rates in the next year or so will be up: in short, the economic landscape is changing. AMP chief economist Shane Oliver says: , “Interest rates have been cut enough, as the housing sector is recovering and confidence is moving in the right direction.”

Ahhh, if only. There is no doubt we’re seeing a cyclical turn in the housing sector, finally. But, in all honesty, it is next to nothing compared to what we have in store over the next three years. Under the MSM froth, authorities are beginning to realise it.

The overriding message from last week’s RBA SoMP was that the mining capex cliff is getting steeper and longer. That’s why they downgraded their 2014-15 growth forecasts. The central bank is now seeing virtually two years of below trend growth ahead. On the balance of probabilities this will get worse still. 2015/16 will also be tough as the capex cliff goes on, driven by the new cost-out deflation trend in mining, and as the calamity in manufacturing reaching its zenith with the departure of the car makers.

The Government is also beginning to realise how difficult this is going to be. Joe Hockey was not encouraging on Friday as he primed the Keynesian pump. Also from the AFR:

“2014-15 is hugely important. We need the mining projects to happen in 2014-15. If significant mining projects that were proposed for 2014-15 do not proceed then we are facing a growth challenge.”

“But like the RBA, we are up for it. That’s one of the reasons why we need to roll out a significant investment program that lays the foundations for the infrastructure of the nation.”

…“We cannot allow red tape, state or federal, to impede our ability to roll out infrastructure. We are fully aware of the growth challenge two years out. We are fully aware of the growth challenge of years ahead.”

With respect, Joe, it’s not a “growth hole”, it is a “competitiveness hole” and until it is addressed the Australian economy will not properly recover.

The cyclical bounce we are seeing in the economy right now is not enough. An economy grows by increasing its productive capacity via investment. Juicing house prices, consumption and infrastructure spend can only work for a little while when you’re already so indebted.

I am in favour of a material infrastructure investment that is thoroughly analysed as productivity positive but even Joe’s rushed and poorly designed roads agenda will not get us through because it is attacking symptom not cause.

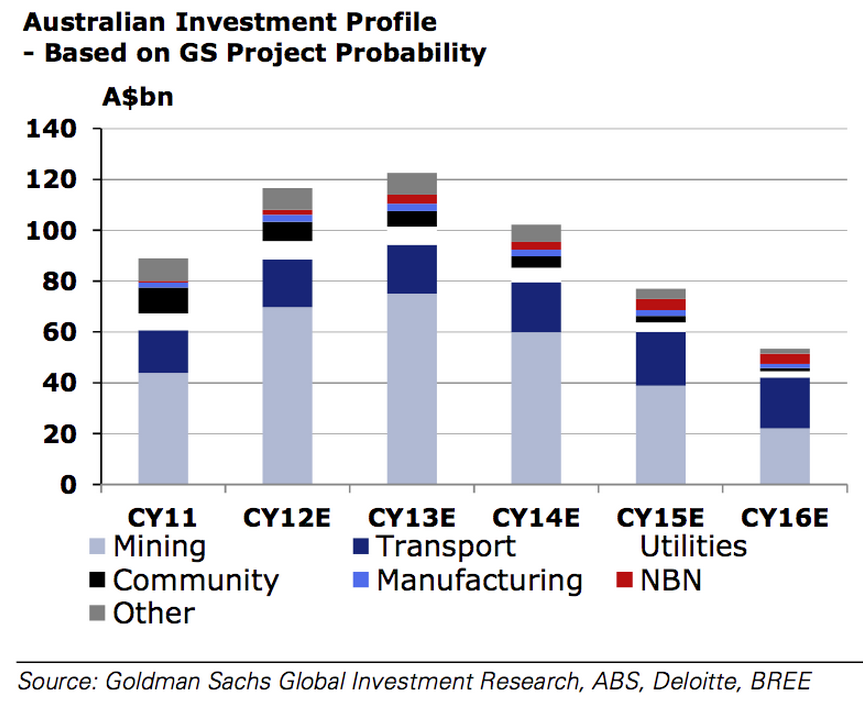

Here, again, is the investment cliff in all of its hideous glory, including Joe’s roads and a decent housing construction recovery (from Goldman Sachs):

Returning to Bassanese, the balance of probabilities remains that the RBA is not going to raise interest rates in the next year or maybe not the year after that either, even with some turnaround in non-mining capex. Consider how weak the economy has been over the past year with capex falling a few percent. It’s not hard to imagine how it will struggle as investment falls 15-20% per annum relentlessly.

And there is another problem. Not only will growth likely be weak, its composition will make it seem weaker still. It is universally agreed that much of future GDP growth will be supported by net exports. But one percent growth contributed by net exports is very different to the same amount via investment. The former reduces jobs, the latter boosts them. If we use the RBA growth median of 2.5% but have a composition of growth that is the functional equivalent of 1.5% in the labour market then you start to get the picture.

There is one exception to the ‘lower for longer’ argument. If the Sydney house price blowoff spreads then the RBA may have to jack rates briefly to put a lid on it. That would raise a very high risk of recession as the froth evaporated from household activity and exposed the investment cliff beneath. Rates would resume falling shortly afterwards. That is one reason why I put a higher probability than most on the RBA getting together with APRA and introducing macroprudential measures then cutting rates further to lower the dollar.

That’s the rub. There really is only one way to renew the business investment needed for a genuine recovery and that’s to increase our competitiveness. It can be done via recession. It can be done via internal measures like wage restraint and an engineered lower dollar, below 70 cents for an enduring period. But until it is done, fits and starts of activity will be under pressure to revert to the underlying downward trend for growth and rates.