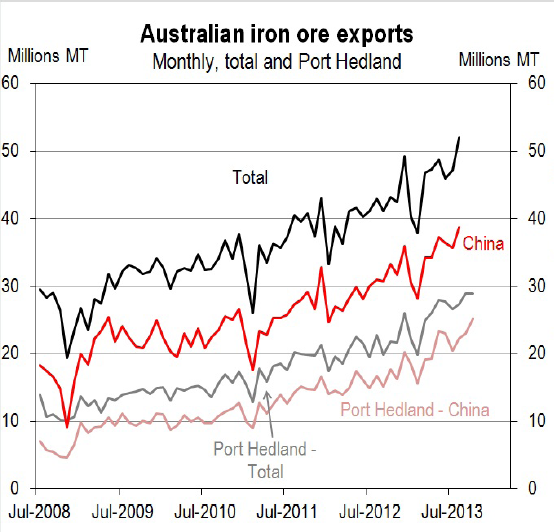

Paul Bloxham has a useful note out quantifying the recent link between iron ore prices, growth and incomes:

With 2013 almost complete, it looks as though Australian iron ore export volumes are likely to have risen by around +16%, while prices appear likely to have risen by around +7% on average relative to 2012. Taken together, this suggests iron ore exports are likely to have boosted Australian incomes (nominal GDP) by around +0.9ppt in 2013, which follows a drag from the sector in 2012 as prices fell sharply.

The risks to the iron ore price outlook are, however, to the downside. On the demand side, Chinese fixed asset investment is expected to slow. Our China economics team has growth in fixed asset investment slowing from +20.5% in 2013 to +19.0% in 2014. At the same time, iron ore supply is set to continue to ramp up. Australian official forecasts, based on capacity that is being built, suggest an expected pick-up in export volumes of +17% in 2014.

Our colleagues in the equities team are forecasting that iron ore prices could fall from USD134 this year to USD115 in 2014 (see ‘Metals quarterly: Q4 2013’, link below). This would still leave iron ore prices high relative to history, at 780% above their 1990s level, consistent with our view that the recent commodity prices super-cycle has been more super and less cycle (see ‘Global commodity prices: More super, less cycle’, link below). Nonetheless, lower prices would be a cyclical drag on Australian incomes.

In principle, a fall of this magnitude could knock -0.6ppts off Australian income growth in 2014, assuming everything else constant. However, this fall would be offset by the expected pick up in export volumes (+17%), leaving the overall iron export contribution to income growth broadly flat. Another key offsetting factor would be any likely fall in the AUD, which would increase the AUD price of exports. Our FX team have in mind that the AUD/USD cross rate will average 88 cents next year, down from 95 cents this year (see Bloom, D. et al (2013) ‘Currency Outlook’, 10 October, link below). Nonetheless, it seems likely that iron ore exports will contribute less to Australian income growth next year than they did this year. As a result, the economy will be more reliant on other sectors and growth will need to continue to rebalance.

I more or less agree.