The Productivity Commission has released a new report warning of a Budget crisis unless reforms are made to raise the aged pension and compel retires to pay for more of their own health costs. From The AFR:

Launching a major study into the policy effects of Australia’s ageing population, Productivity Commission chairman Peter Harris said state and federal government budgets faced “inexorable and major impacts” without major changes to policy.

The commission has proposed increasing the eligibility of the age pension to 70 years, as well as finding productivity savings in the health sector and allowing retirees to draw on home equity to help fund aged care costs.

…the Productivity Commission’s report found that the demands of an ageing population would add an extra 6 per cent of gross domestic product to government budgets by 2060 if not dealt with. In today’s terms, that amounts to $90 billion.

Changing the eligibility age of the age pension to 70 years would reap $150 billion in savings over the period from 2025-26 to 2059-60 and increase participation rates among older workers by around 3 to 10 per cent, the report found…

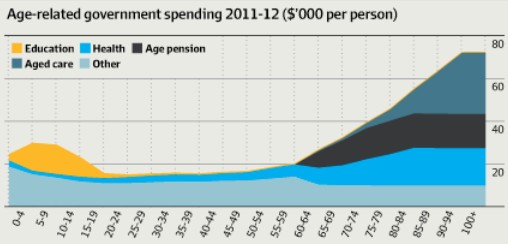

The capital investment required to meet the needs of the expanded and aged population by 2060 is expected to reach some $38 trillion, five times more than that required over the previous half century…

One innovative suggestion to address the issue could be allowing retirees to draw on the equity in their home to make co-contributions to their aged-care costs, thus reducing the need for age pension payments.

Advertisement

Separately in The Australian, David Uren reports that taxes would need to increase by 21%, according to the Productivity Commission, unless mitigating reforms are made, whereas the working share of the adult population would decline steadily from around 64% currently to around 59% – a level not seen since 1978 – hence reducing the tax base whilst raising aged-related costs.

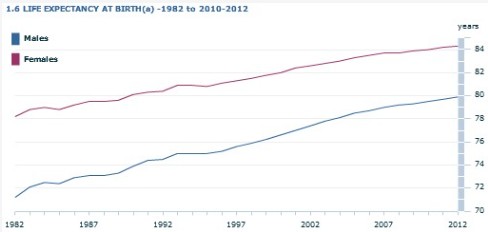

Without a shadow of a doubt, the Federal Budget is facing an emergency unless reforms are made to retirement policy. As noted a few weeks back by the ABS, Australian life expectancy has increased dramatically (and will continue to do so):

“A boy born today could expect to live 79.9 years, while a girl could expect to live 84.3 years. For those approaching retirement age, say 65 years, males could expect to live a further 19 years and females a further 22 years”.

Advertisement

The falling worker share will shrink the tax base, just as health and ageing-related outlays grows inexorably. Accordingly, remedial policy action must be undertaken, and raising the retirement age is a good start, although it will unlikely be anywhere enough.

In my view, the Productivity Commission has been overly timid with its policy prescriptions. As argued repeatedly, other key issues working to make Australia’s retirement system unsustainable are: 1) the 15% flat tax on superannuation contributions, which provides the lion’s share of concessions to those who need them least (i.e. upper income earners), costing the Budget a fortune in the process; and 2) exempting one’s principal place of residence from the assets test for the pension, resulting in wealthy retirees receiving benefits.

Therefore, in addition to raising the retirement age, why not: 1) make concessions on salary sacrificing into super 15% for everyone; and 2) means test all of one’s assets (including the family home) when working out who receives the pension?

Advertisement

If the family home was included in the pension assets test, then there would be no need to compel retirees to withdraw their home equity, which risks unintended consequences and could potentially worsen inter-generational equity (as explained here).

The fundamental issues around superannuation concessions and means testing of the aged pension must, therefore, also be addressed if Australia’s retirement system is to become sustainable.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.