Credit Suisse advises you give up reading MB and get yourself a stock advisor instead:

After a number of years of macro-driven stock markets, micro now matters more. Traditional top-down signals, while still important, are having less influence on stock prices and the investment process. This is also the case in Australia where classic bottom-up focused investors, Long-short funds, are generating stronger returns. The switch to microdriven markets is entirely consistent with falling stock price correlations and a low profit growth outlook we forecast for Australia.

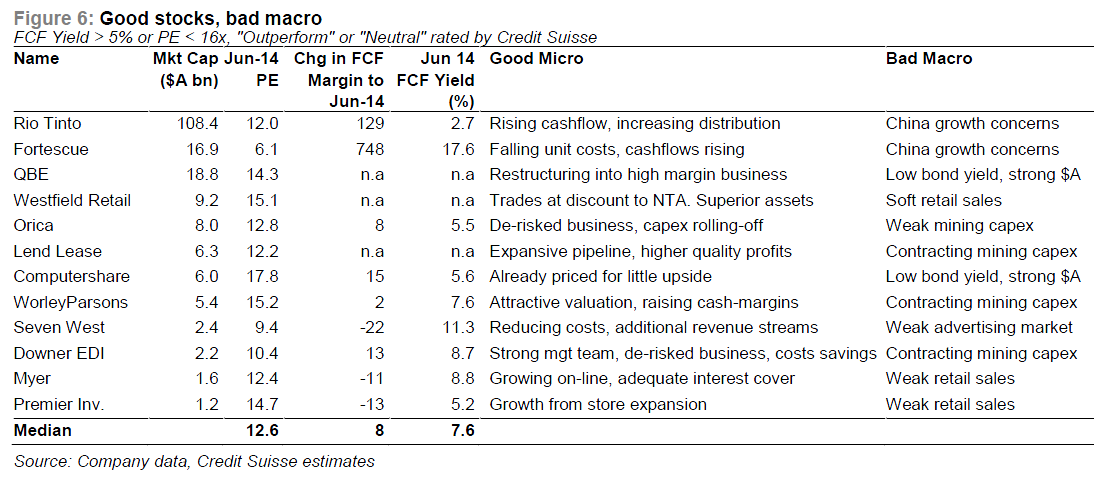

With waning top-down influences, it is an opportune time to look at “Good Stocks with Bad Macro”. These stocks have positive bottom-up drivers. However, they are held back by macro concerns such as a strong Aussie dollar, sluggish Chinese demand, weaker mining investment and low bond yields. Our stocks trade on Jun-13 P/E of 12.5x and a FCF yield of 7.6%. This compares to 15.4x and 4.4% for the ASX 200. As markets become less macro-driven, investors should speak to stock analysts more and listen to central bankers less.

RoRo is dead

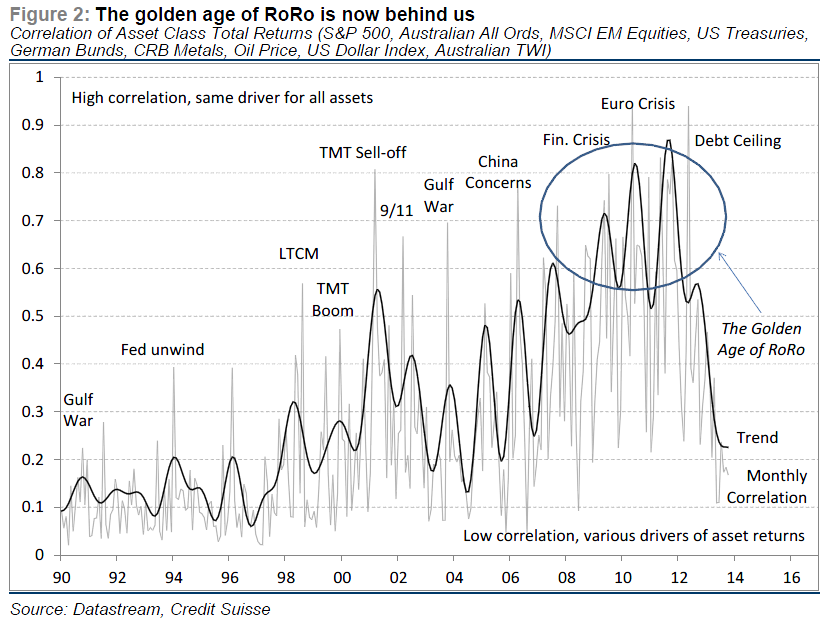

Risk-On, Risk-Off has dominated markets for much of the past six years. It has become so ingrained in financial circles that we have even developed a silly acronym for it — RoRo. During the golden age of RoRo – 2007-12 – asset returns were highly correlated. So when Lehmans collapsed the equity market sold-off, the Aussie dollar depreciated and bonds rallied together. When central banks announced coordinated liquidity injections, asset prices reversed. The financial crisis led to the euro crises and provided a fantastic multiyear setting for RoRo. As we show in Figure 2 this was an unusually long period of high asset price correlations. We haven’t seen anything like this for more than 25 years.

The golden age of RoRo was a time when top-down investors performed well. Maybe they could understand the potential significance of these major macro events more clearly. Perhaps they were more in tune with timing the markets wild swings. Either way the signals top-down investors were looking at were the ones driving markets. Global macro funds returned 9% p.a. from 2007-11.

…Bottom-up factors matter more. While top-down influences should not be ignored, it is clear they are becoming less important in driving stock prices in Australia. We believe our group of good-stocks-with-bad-macro will perform well as investors focus more on bottomup issues. Orica’s result this week shows how much alpha this strategy can generate. The time has come for investors to pick up the phone to the analyst and spend less time listening to central bankers.

It’s a sort of reasonable argument. I could say that my recent miss of the big iron ore rally is a case in point. But not really. The rally was driven by macro factors that I misread and fundamentals.

And that’s the main point. You can’t do stocks without macro. Most returns come from asset allocation, not stock picking, which is a fool’s errand in my view.

Advertisement

Fading top level asset correlations are only the tip of the iceberg. After all, are you really happy to pile into an Australian mining stock if the Fed is going to taper and China rebalance?

RoRo may have eased but the top-down era has just begun.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.