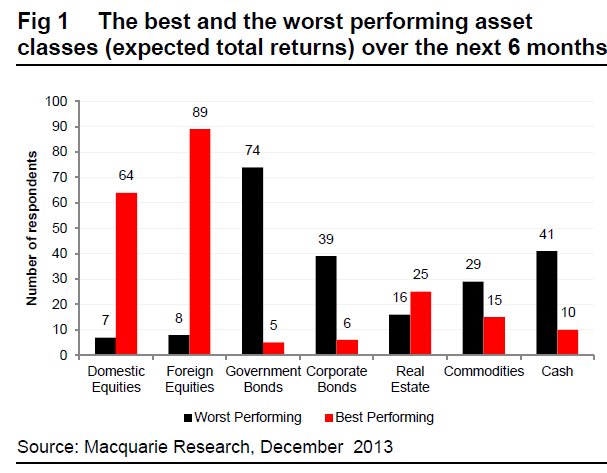

A fascinating juxtaposition today in a couple of equity strategist notes from investment banks. The first by Mac Bank is based upon a survey of local money managers:

We assess the results of our recent global macro survey of senior analysts and investment decision-makers. Our survey focuses on the outlook for the global economy and central bank policy actions over the next six months. Impact

The global economy is expected to expand faster over the next six months largely supported by positive outlook in the US and Euro area economies. Expectations of ongoing global expansion and continued liberal liquidity conditions are also underpinning a continued favourable view in terms of risk appetite and growth assets.

Our global macro survey results come at an important juncture for the global economy and financial markets, notably in the wake of the US Federal Reserve’s decision to begin winding back its QE asset purchase program in January 2014.

Indeed, the overall tone of the 150 survey respondents was bullish with almost all anticipating that the global economy will expand at a faster pace over the next six months and that the US Fed will move to wind back quantitative easing (QE) measures over the period.

In distilling the overall sentiment of our survey respondents, we have identified several key themes that are likely to influence investment decision-making in 2014; namely:

ongoing liberal global liquidity conditions;

sustained appetite for risk and growth assets;

caution about risks associated with episodes of macroeconomic instability;

absence of pricing power in terms of the production and supply chain; and

caution about large negative output gaps and high unemployment in the major developed economies.

Those look like appropriate conclusions in an oversupplied and deflationary world to me! And the asset allocation looks about right too, a point I will come back to.

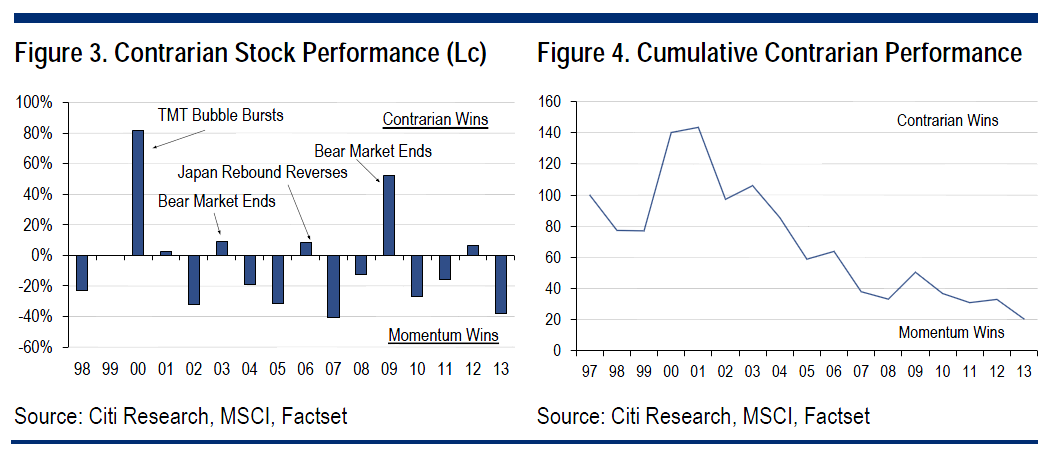

Such a survey is, by definition, capturing consensus, so let’s now turn to our second note, by Citi, which looks at the performance of contrarian investors over time:

Advertisement

Contrarian Strategies Tend To Underperform — While simple contrarian strategies often perform very well at big macro turning points, they tend to underperform the rest of the time.

Contrarians Punished In 2013 — Contrarians were punished in 2013. An extension of a two-year 40% rally in global equities has made this one of the biggest momentum years since 1998.

Contrarian Calls For 2014 — But that won’t stop the contrarians trying. Their big trade for 2014 will be to buy (again) the commodity-related stocks and Emerging Market countries. At a global level, we would have more sympathy with the latter trade. We are overweight EM and neutral global Energy and Materials in our current allocations.

Regional Menu — 2013 was a bad year for contrarian stock pickers within all major markets. Going into 2014, contrarians in the US will be buying large tech companies and selling biotech and internet stocks. In Europe and EM, they will be buying commodity stocks and selling a mix of industrials, consumer and tech stocks.

Watch Out For The January Effect — While contrarian stock picking strategies are unsuccessful most years, they do tend to outperform in January.

This is kind of absurd in-so-far-as Citi is selecting the contrarian calls on very limited criteria. Here’s what they offer about 2014 for instance:

Contrarian strategies have had one of the worst ever years. They have not been successful over the longer run either, especially at a stock-picking level. But that won’t discourage the contrarian Christmas lunchers from trying again in 2014. Memories of big pay-offs in the financial crisis and the subsequent recovery have not faded yet.

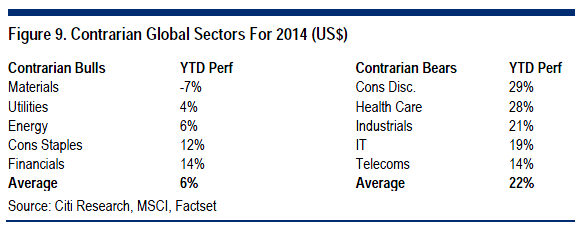

…There was not a really clear cyclicals versus defensives global sector theme in 2013 and that is reflected in the sector calls for 2014 (Figure 9). A contrarian sector strategy for 2014 is long both commodity sectors and selective defensives. Sector shorts include defensives (Health Care and Telecoms) and cyclicals (Consumer Discretionary, Industrials and IT). Financials and Telecoms are on the border of the long/short list.

Advertisement

Using myself as example, then, I’m bearish materials (consensus), bearish on financials (contrarian), bullish on IT (contrarian) and bullish on consumer discretionary (consensus).

Back to the Mac Bank survey, I agree with the themes presented but I’ll bet I’m less sanguine about the system’s ability to right itself than the many of the surveyed, meaning I would allocate differently based upon risk assessments than they would, despite filling the same shoes.

From this sample of one I have to ask is there really anyone out there that fits Citi’s criteria? And if not, what’s the point of it?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.