The news today is that another big brand manufacturer appears headed to the wall in SPC Ardmona:

The future of the SPC Ardmona cannery in Victoria’s Goulburn Valley appears bleak after Prime Minister Tony Abbott said the business should get its own house in order rather than seek government assistance.

Mr Abbott’s tough approach comes despite an expert panel comprising business figures Dick Warburton, Catherine Livingstone and former ALP industry minister Greg Combet recommending the government give SPC the $25 million it was seeking.

The panel agreed SPC, which is owned by Coca-Cola Amatil, was not seeking a bailout per se but had put together a viable proposition involving new products and markets. Coca-Cola Amatil says it will provide $150 million if the federal and Victorian governments contribute $25 million each.

Advertisement

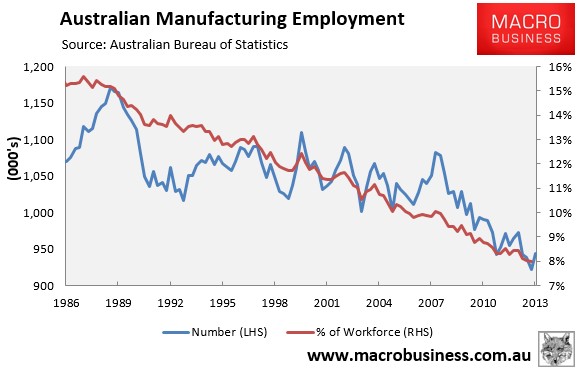

In addition to the recent announced closure of big names like the Ford and Holden assembly lines, as well as the Electrolux refrigerator factory in Orange, the quarterly employment data from the ABS clearly shows an industry in contraction, with the total number of people employed in manufacturing and the industry’s employment share falling sharply over the past 30-years, from nearly 17% of total employment in 1984 to just 8% as at November 2013 (see next chart).

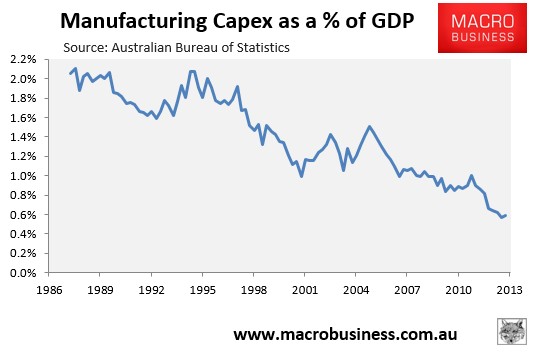

Manufacturing capital expenditures (capex) has also tanked, falling from 2.1% of GDP in 1987 to only 0.6% of GDP as at September 2013 (see next chart).

Advertisement

Upon announcing Holden’s closure in December 2013, general manager Mike Devereux, cited the below reasons for the decision:

“Australia’s automotive industry is up against a perfect storm of negative influences, including the sustained strength of the Aussie dollar against almost all major trading currencies, the relatively high cost of production and the relatively small scale of the local domestic market… building cars in this country is just not sustainable”.

Advertisement

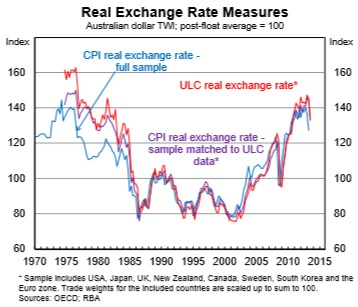

Yesterday, the Reserve Bank of Australia (RBA) released a series of documents under Freedom of Information on Australia’s exchange rate. Locked away on page 27 of the PDF is the below gem showing just how uncompetitive Australian manufacturing costs have become when compared against other nations:

Although the level of the real TWI can be largely ‘explained’ by its medium-term determinants, it nevertheless remains at a high level. This observation is robust to the choice of deflator, with a unit labour cost (ULC) based measure presenting a very similar picture to the standard CPI-based measure. This is particularly evident when using a matched sample of countries (the ULC data are available for a relatively narrow sample of countries and, in particular, are not available for China).

ULCs are a commonly used – albeit partial – measure of cost competitiveness. The OECD publishes these data for a number of member nations, calculated as the ratio of total labour costs to real output. These data show an increase in Australia’s ULC measure (in domestic currency terms) relative to most of Australia’s OECD trading partners over the past decade or so. This has exacerbated the effect of the appreciation of Australia’s nominal effective exchange rate on Australia’s overall international competitiveness.

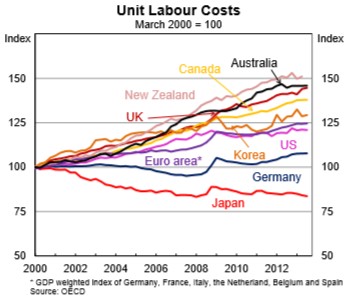

The decline in Australia’s ULC-based measure of cost competitiveness has been even more pronounced for the manufacturing sector. However, it should be noted that the Australian manufacturing sector accounts for around 7 per cent of GDP, compared to an average of around 15 per cent for Australia’s OECD trading partners.

New Zealand and Canada have also recorded relatively strong increases in their ULCs alongside marked appreciations of their nominal effective exchange rates over recent years. In contrast, the UK’s strong increase in ULCs has coincided with a depreciation of their nominal exchange rate.

The above analysis from the RBA confirms Holden’s Mike Devereux’s concerns. It also highlights why the Australian dollar must continue to devalue if Australia’s non-mining economy is to remain competitive and how that devaluation must not be lost to rising wages, as well as the need for ongoing structural reforms aimed at improving productivity.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.