By Tom Conley, Senior Lecturer, Griffith Business School. You can follows Tom’s blog here.

The Reserve Bank has recently published a historical comparison of the terms of trade in Australia entitled “Macroeconomic Consequences of Terms of Trade Episodes, Past and Present” by Tim Atkin, Mark Caputo, Tim Robinson and Hao Wang.

Now while such articles may make many people’s eyes glaze over, there are few concepts that are more important in understanding the Australian economy than the terms of trade and Australians could learn a lot by reading this excellent paper. The authors’ conclusion (quoted below) is on the optimistic side of the debate about Australia’s economic future and it doesn’t canvass the possibility that the extended duration of a high terms of trade and exchange rate have caused significant damage to non-mining sectors of the tradable economy.

The terms of trade is the index-measure ratio of the average price level of exports to the average price level of imports. It effectively reflects the capacity of a given quantity of exports to pay for a given quantity of imports, and provides an important indication of the strengths and weaknesses of the economic structure. A rising or falling terms of trade indicates the possibility of improving or declining living standards, because if what we sell earns relatively more than what we buy, we will be relatively wealthier. Because the terms of trade is a ratio, increases can be a result of export prices increasing at a greater rate than import prices, or export prices increasing while import prices are declining, or export prices declining at a slower rate than import prices. Of course, a rising terms of trade doesn’t stop us from buying more things than we sell, which we have made a habit of for much of our history! Improvements in the terms of trade are not reflected in GDP figures, but improvements do contribute significantly to increases in national disposable income.

Basically Australia has been lucky enough to have a high terms of trade for an extended period of time, but the ratio is now on the way down, with the consequence of declining income for Australians. The extent and rapidity of the descent will have a very large bearing on the economy and by extension on all of us.

We took the view in the 1970s – it’s the old cargo cult mentality of Australia that she’ll be right. This is the lucky country, we can dig up another mound of rock and someone will buy it from us, or we can sell a bit of wheat and bit of wool and we will just sort of muddle through … In the 1970s …we became a third world economy selling raw materials and food and we let the sophisticated industrial side fall apart … We must let Australians know truthfully, honestly, earnestly, just what sort of international hole Australia is in. It’s the price of our commodities – they are as bad in real terms since the Depression … If this government cannot get the adjustment, get manufacturing going again and keep moderate wage outcomes and a sensible economic policy, then Australia is basically done for … If in the final analysis Australia is so undisciplined, so disinterested in its salvation and its economic well being, that it doesn’t deal with these fundamental problems … Then you are gone. You are a banana republic.

Keating used the sense of crisis to further the case for economic reform. The subsequent financial, trade, competition and labour reforms of the 1980s and 1990s helped Australia deal with the current boom, providing a flexibility to adjust to externally derived price shocks.

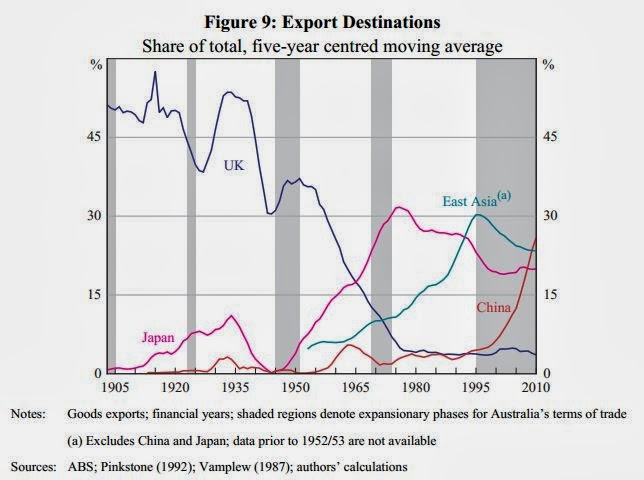

Form the 1960s, the rise of Japan, followed by South Korea and Taiwan, Singapore, Malaysia, Thailand and other non-communist countries of Southeast Asia had provided significant expansion of export markets for Australian commodities, but had not led to a sustained structural increase in their prices.

Betting on China

The major story of recent years, however, has been the rise of China. It is possible that China, India and most of the rest of Asia will continue to grow rapidly as the authors suggest for the next decade or so, but it is unlikely that this growth path will be smooth. China is actively seeking to diversify its sources of supply of the key resources it imports from Australia. Price increases eventually produce supply increases, which often then lead to oversupply and falling prices. And so on. This is the nature of the commodity cycle. China currently appears to be slowing and restructuring its economy away from commodity-intensive development. The debate over the extent of these changes is controversial but the outcome will be very important for us.

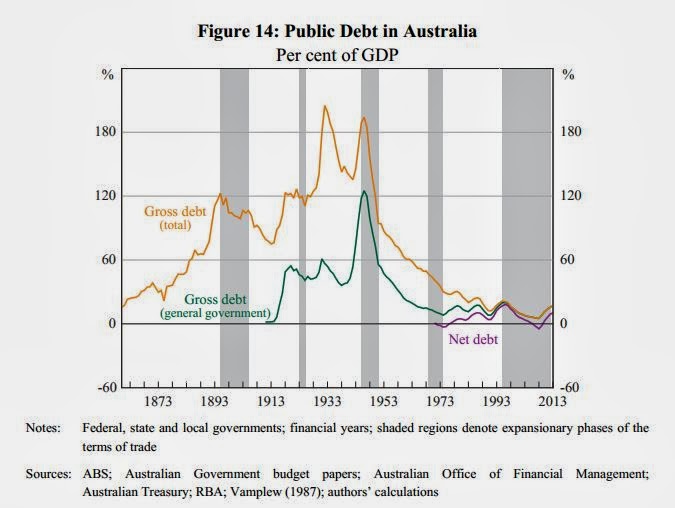

A long-term look at public debt shows that the current situation is relatively benign when compared with the past, despite continual scare-mongering by policy-makers and commentators. According to the authors: “The primary reason for the large size of public debt in the past was the legacy of major conflict and the ‘settler nature’ of the Australian economy, the latter requiring high rates of social and economic infrastructure. In contrast, public debt in the current episode is at low levels. It could be argued that there is significant room to move to build the physical and mental (health and education) infrastructure to make Australia an economic powerhouse in the 21st century. But this certainly can’t happen when public debt is seen as bad regardless of how it is used.

Another major difference of the recent boom was that earnings did not increase in tandem with the increase in commodity prices, as they had done in previous episodes. Undoubtedly, this helped macroeconomic management. Given the hefty wage increases in mining related industries it begs the question as to who was keeping the average down. Obviously some workers were not doing quite so well! According to the authors:

The institutional structure of the labour market during the current episode has been the most flexible over any expansion since Federation; a considerable increase in relative wages in the resources sector and a more decentralised industrial system facilitated a relatively low unemployment rate during the upswing in the terms of trade without creating substantial inflationary pressures.

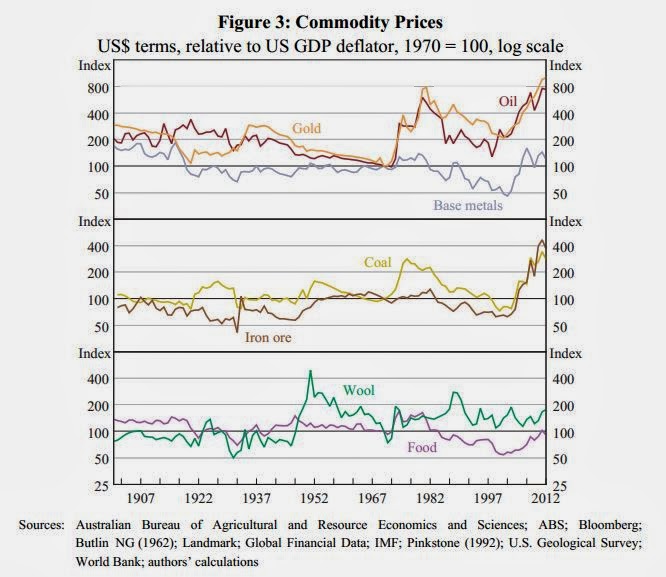

Australia’s current terms of trade cycle has parallels with earlier episodes. Historically, large movements in the terms of trade were mainly driven by changes in export prices, particularly wool, which reflected strong demand from industrialising economies, coupled with adverse supply developments, such as drought. Upswings in the terms of trade have generally boosted domestic demand, usually with a sizeable contribution from investment, probably reflecting both a direct response to higher commodity prices and the associated improvement in wealth and confidence. In some episodes, growth in immigration and pent-up demand following war also supported growth in investment. Typically, net exports have contributed little to economic growth during the upswing in the terms of trade; sluggish supply responses are exacerbated by the real exchange rate appreciation, which dampens growth in other exports and supports imports. Many of these features have been present in the current episode.

The current episode, however, has some distinct features. One is that it has been mostly related to bulk commodities, instead of rural commodities. Consequently, the sluggish response of supply partly reflects the characteristics of resources investment – namely long periods to plan and gain approval for projects and the need to develop infrastructure. However, just as Australia was the world’s major source for internationally traded wool throughout previous episodes, today it is the world’s largest exporter of steel-making materials and it is likely that Australia will also become a major source of liquefied natural gas exports in the coming years. A decline in the terms of trade is therefore, to some extent, the result of new supply from Australian producers coming on-line.

The most recent upswing was the largest sustained increase of the terms of trade on record, and the Australian economy is likely to continue to be a beneficiary of strong growth in Asia. Indications suggest China’s industrialisation and urbanisation process, which has underpinned the increase in demand for steel-making commodities, is likely to continue for a number of years, although it may well grow more slowly than in the past. Chinese infrastructure needs remain large; an example is that steel demand for residential construction is not estimated to peak until around 2024 (Berkelmans and Wang 2012). While the path of economic development is not always smooth, it is important to remember that this is not the first episode during which one country and a narrow range of commodities have been of particular importance to the Australian economy; rather, that is the norm.

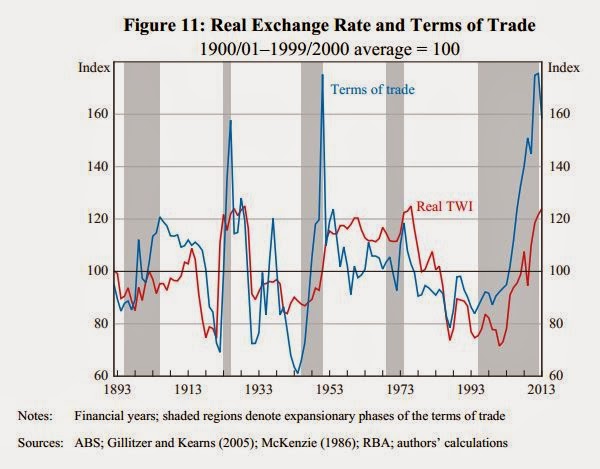

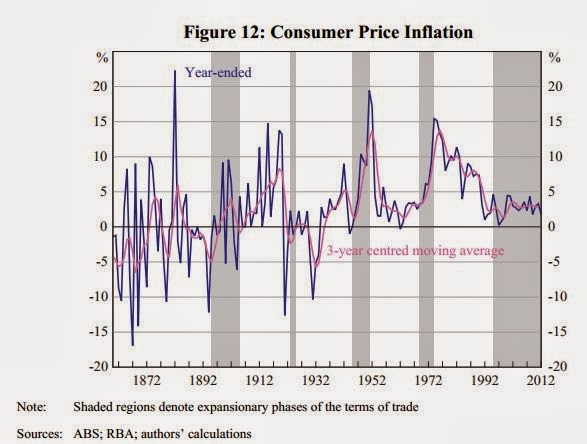

Another stark difference is that despite the unprecedented movement in the terms of trade, the macroeconomic adjustments in Australia have been relatively smooth. Inflation, for example, has remained contained, in contrast to many previous experiences, such as the Korean War wool boom. Furthermore, inflation expectations have remained relatively low and stable. Factors facilitating this include the greater flexibility present in the labour market, the inflation-targeting regime adopted by the RBA, and the flexible nominal exchange rate, which has enabled the necessary appreciation of the real exchange rate to occur in a less disruptive manner.

Historically, for several years following a peak in the terms of trade, growth in investment and output per capita tends to be below average. As we have emphasised, the real exchange rate and the terms of trade generally move together.

Consequently, the expected easing in the terms of trade, reflecting growth in the global supply of the bulk commodities, may be accompanied by falls in the real exchange rate. More generally, an increase in Australia’s competitiveness would help facilitate the macroeconomic adjustments necessary during the transition from the investment to production phase by providing support to sectors outside of the resources sector, thereby helping to rebalance growth in the economy. Reflecting the unparalleled magnitude of the expansion, the transition necessary is considerable and is likely to pose challenges to both firms and policymakers. The current policy frameworks and institutional structures, which were important in facilitating better macroeconomic outcomes during the upswing than occurred historically, may also assist this transition.