From the China Securities Journal:

According to CISA statistics, by the end of early February inventory of the key steel manufacturers amounted to a record high of 16,328,400 tons, up 20.02% MoM. Insiders say due to multiple factors including dropping steel prices, fewer orders and difficult transport, early February saw a sharp rise in steel stocks. Considering the iron ore inventory, which exceeded 100 million tons to a record high days ago, the steel market is facing huge de-stocking pressure this year.

With early February coinciding with the Chinese New Year holiday, closed market and suspended steel shipment have forced mills to pile up inventory.

According to CISA statistics, at the end of early February the inventory of key steel manufacturers went up by 20.02% month-on-month and 42% year on year to 16,328,400 tons, hitting a record high. In late January the inventory stood 13.605 million tons, 4.3% higher than the same period last December.

…Data show that in early February the crude steel daily output of member companies averaged at 1,761,500 tons, up 102,100 tons or 6.15% over the previous ten days. The average national daily production of crude steel is estimated at 2.066,1 million tons, up 102,100 tons or 5.2% over the previous ten days.

In this regard, analysts believe that as the Spring Festival holiday draws to an end and steel production in early February gradually picks up to normal level, the crude steel production has risen significantly. Although it can’t compare with the average 2.13 million last year, a 5.19% month-on-month growth 5.19% and 4% year-on-year growth have been achieved.

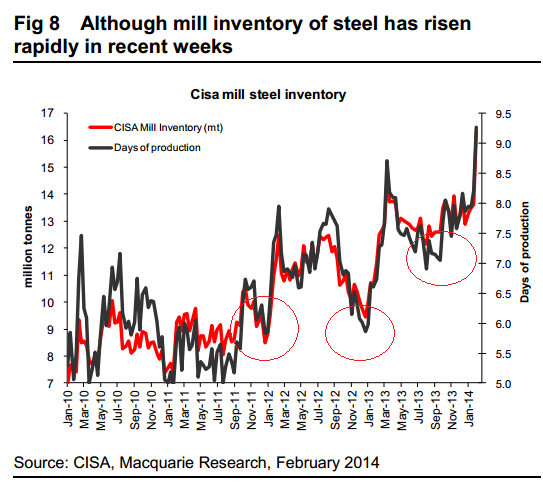

This data is a week or so old now and is a normal seasonal build up so that’s not why I’m posting it. A few points are worth making in light of the struggle in iron ore markets. The stockpile is now at record highs but it has had to add relatively less output to get there than in past years because inventories were so high coming into the year (chart from Mac Bank):

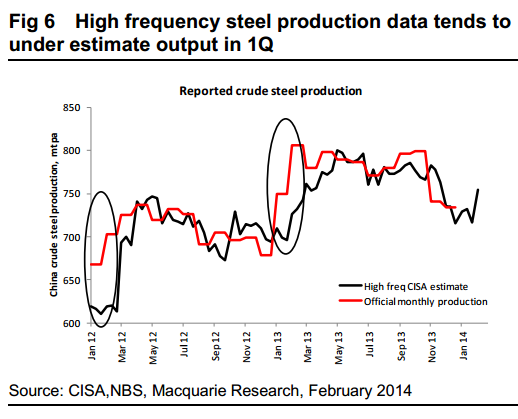

That could be seen as evidence in support of the low daily run-rate of steel production, in turn implying underlying demand is less than robust, or certainly not growing. Contrary to this, Mac Bank has been arguing that the daily run rate of steel output is likely higher than that described by CISA:

Difficult to know yet, but it matters because if underlying demand isn’t growing then the steel and iron inventories will be under greater pressure to destock, as the CSJ describes, meaning greater price weakness for both.