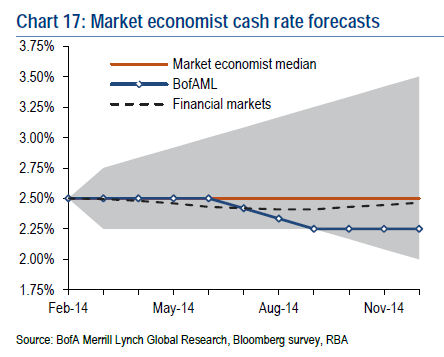

The RBA meets today. With a few notable and intelligent exceptions, market economists are increasingly of the view that the RBA will have to round up its growth and inflation forecasts, and prepare the ground for interest rate normalisation. In this view, rebalancing is underway and the housing and consumption cycle will gain traction and persist as interest rates rise. Here is a chart from Saul Eslake showing roughly that

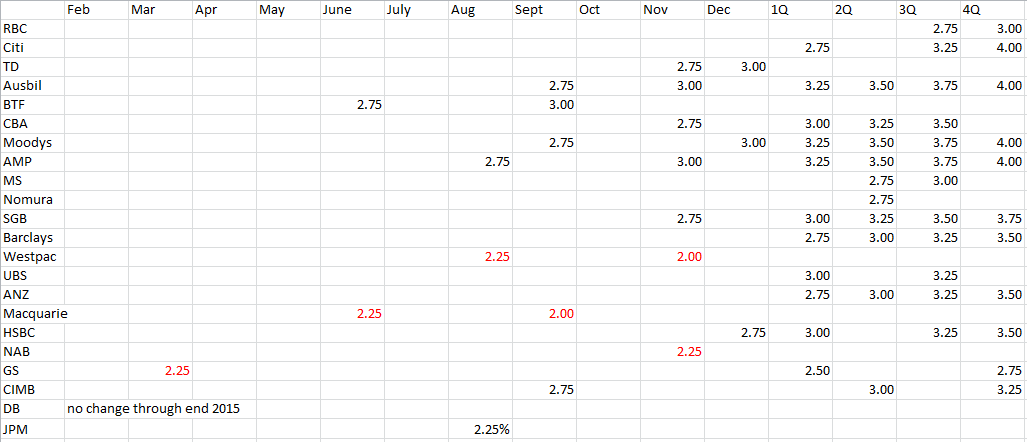

And from Dow Jones the major player’s outlooks:

This consensus ignores one vital point: the economy is in a post-boom phase of structural adjustment with further falls ahead for the terms of trade and even greater falls in mining investment. In effect that means that national income will keep falling, and that the moment any housing and consumption activity slows, the full force of the capex cliff will come to bear on a persistently soft labour market.

Hence the economy will be unusually sensitive to interest rate hikes; a sensitivity made all the more pointed by the dynamics driving house price gains, with speculators in control and new households conspicuously absent.

The last time the housing market was in this situation was in 2003 Sydney and it took just two rate hikes and a little jawboning to bust the market. Yes, the cash rate range at the time was higher by 2.25% but the real interest rate in mortgages was only 60bps higher because the banks have widened their margins to the cash rate so much since the GFC. Moreover, I think it fair to posit that lending standards were looser then and consumer sentiment was stronger (or more profligate) as seen in comparable savings rates.

It’s certainly the case that the broader economic settings were on precisely the opposite trajectory with the mining boom just taking off. In short, the neutral cash rate in 2003 was much higher than it is today so “normalisation” is much lower as well.

The RBA’s primary emerging challenge is growth not inflation. It is unlikely to be rounding up its forecasts for the former even if it does a little for the latter. There is no need to panic on inflation. While tradable prices are going to rise, the recent spike was as much seasonally based in dry weather for fruit and veg and holiday prices. Wage growth is still at recessionary levels as well. Having said that, the dollar is likely to outpace most forecasts to the downside this year so tradable inflation will keep bubbling up.

The real challenge for the RBA in this hobbled growth, rising inflation circumstance is rhetorical. What the bank needs to do, and has already begun, is to shift expectations for the post-mining boom Australian economy away from cyclical factors and towards the structural so that it can improve competitiveness and lift non-mining investment over time.

It’s an oratorical shift potentially as large as the one it managed in 2009, only in reverse. Back then, the RBA released a swath of research and undertook a number of speeches explaining why Australia was going to need higher interest rates for longer to undergo a “structural adjustment” to mining-led growth. This time it will be about why interest rates cannot rise despite restive tradable inflation, as well as why wages can’t rise to match inflation either as we seek to rebalance growth away from mining via improved competitiveness.

This is no small task but it has begun. Last week the RBA released a new study examining post terms of trade adjustments and it concluded:

Historically, for several years following a peak in the terms of trade, growth in investment and output per capita tends to be below average. As we have emphasised, the real exchange rate and the terms of trade generally move together. Consequently, the expected easing in the terms of trade, reflecting growth in the global supply of the bulk commodities, may be accompanied by falls in the real exchange rate. More generally, an increase in Australia’s competitiveness would help facilitate the macroeconomic adjustments necessary during the transition from the investment to production phase by providing support to sectors outside of the resources sector, thereby helping to rebalance growth in the economy. Reflecting the unparalleled magnitude of the expansion, the transition necessary is considerable and is likely to pose challenges to both firms and policymakers.

There it is, in black and white. Expect much more of this to come and the implications are threefold.

First, so long as the RBA can rely upon quiescent wages, it will “look through” tradable inflation as price rises pass like a “pig through a python”.

Second, as the RBA has been pointing out for years, the structural control of wage inflation is not its responsibility. That is the job of government via micro-economic reform, be it labour market regulation or other market structures or boosting productivity. If it is left to the RBA and interest rates to dampen wages then in current circumstances recession is inevitable.

Third, the RBA itself will need new tools to contain housing inflation without boosting the currency, meaning macroprudential policies such as those working so well in New Zealand are coming here too. As Glenn Stevens outlined late last year:

Well, we’ve thought about these issues and we have had, as well, preliminary discussions at a working level with APRA and other agencies about if we needed to do something like that, what kind of things would they be, and I don’t – without wanting to go into the fine details of that, I think we’ve got a sense of the kind of things that might be effective if we need to do them. My general attitude to macroprudential tools is I think they’re potentially a useful adjunct to other policy tools that help you manage some of these tensions for a period of time. I think it would be a bit naïve and contrary to the lessons of history to expect that prolonged use of regulatory tools, and that’s what they are, they’re regulatory tools, and we know that regulatory tools over a prolonged period to try to make up for the fact that the price of credit is, in some sense, not in the right place.

We know that ultimately, that’s not very effective. We know that from our own country’s history. That was the history of the days prior to liberalisation where the price of money was too low and we tried all sorts of regulatory devices to stop the banks lending it and non-banks [inaudible] to lend it and so on. So we know that history, but that’s not to say that you can’t use them for shorter periods to kind of get you through a period where you’ve got some of these tensions. I think they’re probably useful in that setting, as long as we’re realistic about what we can expect.

These three pillars of adjustment require significant national explanation to be most effective. They are also a framework for burden sharing to ensure the adjustment is distributed evenly. The government is so far offering no help on that front, stuck as it is in a reductive narrative of surplus politics, boats and benefits for key stakeholders. Beyond calculations of fairness, that may not be entirely unhelpful to the RBA if the narrative results in a reasonable timetable for budget repair and that helps keep wages quiet. A brewing war on unions may also help, though forced wage restraint will cause them to fight harder than were it done via collaboration.

The opposition is no better, focused upon placing tactical blame on the government without any broader explanations of circumstances.

The RBA will once again have to lead the nation and deliver the bitter message from the pulpit. If it is concerned about such things as legacies, it is in its interests to do so. It does not want to have to hike rates too early in this cycle and cop the blame for the fallout.