As noted briefly by Houses & Holes, the Australian Bureau of Statistics (ABS) has released the Consumer Price Index (CPI) data for the March quarter 0f 2014, which registered a modest quarterly increase in prices, with the result also coming in well below economists’ expectations.

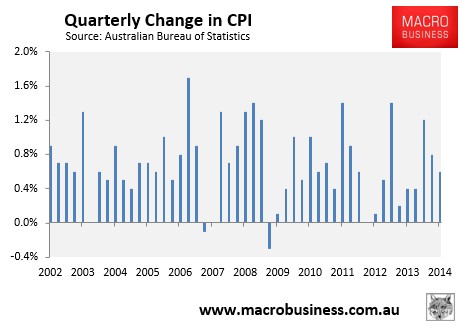

According to the ABS, headline CPI rose by a modest 0.6% in the March quarter, which follows December’s strong 0.8% rise. The 0.6% increase in the March quarter was 25% below analyst’s expectations of an 0.8% increase over the quarter.

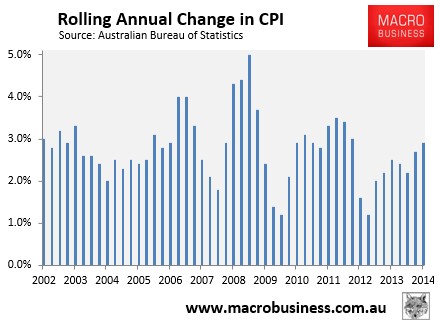

On an annual basis, headline CPI growth rose to 2.9% from 2.7% in the December quarter, which is at the upper end of the Reserve Bank of Australia’s (RBA) target of 2% to 3% growth over the medium term (see next chart).

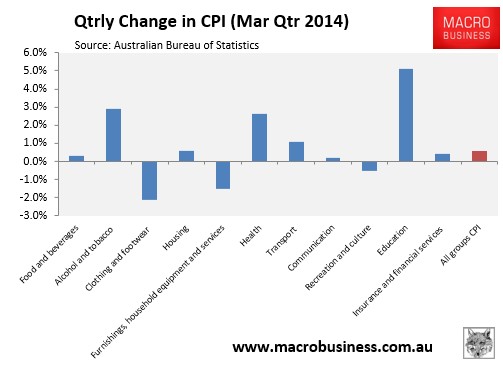

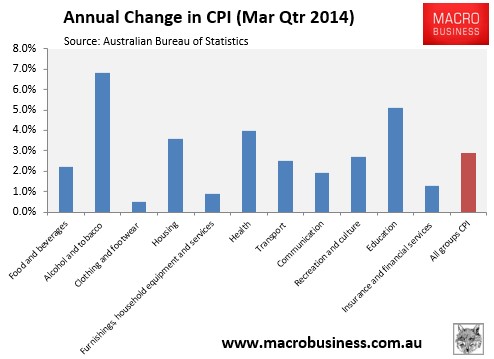

Looking at the core components, you can see that the quarter’s inflation was driven by rising Education, Health and Alcohol & Tobacco prices, partly offset by falls in clothing & footwear, furnishings, household equipment & footwear, and recreation & culture:

Over the year, prices rose across all key components, but were strongest in Education, Health, Alcohol & Tobacco, and Housing (see next chart).

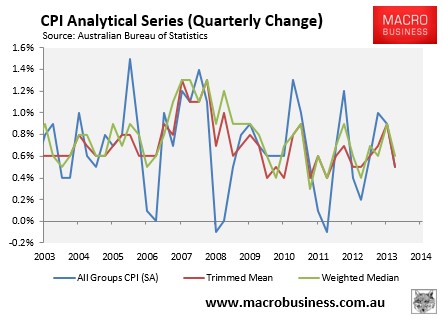

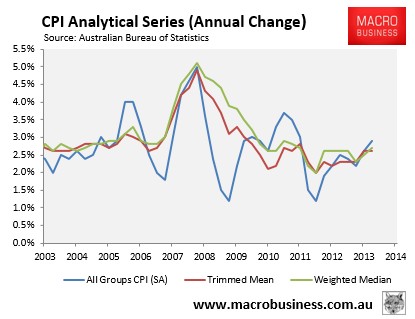

The ABS includes an ‘analytical series’, which provides alternative measures of underlying inflation in the economy. These measures – namely the trimmed mean and weighted median – aim not to measure the size of inflation (which is captured by the headline figure), but the breadth of price inflation across the basket of consumer goods and services.

The purpose of these measures is to exclude unusually large price movements (in both directions) of just a few of the subgroups, which may have quite an impact on the headline CPI. By excluding these outliers, you can get a feel for how widespread across the consumer basket inflation really is (see here for further details).

According to the ABS, the trimmed mean and weighted median measures were little changed from the headline result, rising by 0.5% (trimmed mean) and 0.6% (weighted median) in the March quarter and by 2.6% and 2.7% respectively over the year – just above the middle of the RBA’s inflation target (see below charts).

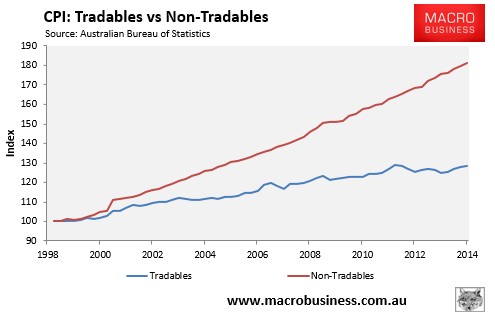

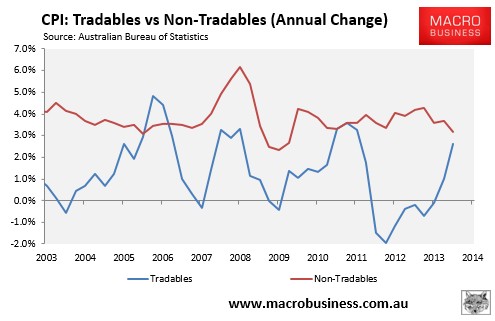

Finally, the below charts show CPI broken-out by tradables (mostly imports) and non-tradables (mostly services). As you can see, tradable inflation (circa 40% of the CPI basket) has barely shifted over the past decade or so – held down by the rising Australian dollar:

However, with the Australian Dollar falling over the past year, tradable inflation has begun to rise, offsetting the modest fall in non-tradable inflation:

In summary, inflationary pressures across the Australian economy appear to be in-check, with the headline, trimmed mean and weighted median CPI measures all tracking within the RBA’s target band. The outlook looks fairly benign also, with the potential for rising tradable inflation (assuming the Australian dollar resumes falling) likely to be offset by a weakening domestic economy, with rising unemployment and excess capacity.