RP Data’s Cameron Kusher has written an interesting analysis of recent supply-side trends in the Australian housing market, which points to ongoing constipation:

Across individual capital cities, the 2011 Census reported that on average; Sydney, Brisbane and Darwin had 2.7 persons per household, Melbourne, Perth and the Australian Capital Territory had 2.6 persons per household and Adelaide and Hobart had 2.4 persons per household. Returning to the original findings, over the year to June 2013, the capital city population increased by 313,387 persons and 114,825 dwellings were approved for construction. If we adjust for average household sizes as per the 2011 Census, to match population growth there would have ideally been a slightly higher 119,135 approvals over the year. If we then further adjust for the assumption that we should approve 15% more homes to replace demolitions, there should have been 137,005 dwellings approved for construction last year, a shortfall of 22,180 capital city approvals.

As the above chart shows, the supply of new dwelling approvals was generally quite sufficient through the 1990s however, throughout the 2000’s new dwelling approvals have been insufficient in relation to the level of population growth. We are now seeing rising dwelling approvals on the back of escalating housing demand and rising home values which is encouraging however, it will have to continue for many years to make up for the insufficient supply response over the past decade or so. In Sydney and Melbourne, there was one home approved for every 2.72 and 2.48 new residents respectively indicating a level of supply closer to equilibrium with demand over the most recent year. New supply remains very much insufficient in Brisbane and Perth where 1 new home was approved for every 3.26 new residents in Brisbane and 3.45 new residents in Perth…

A further important consideration when looking at the relationship between population growth and dwelling approvals is the type of product that is being developed for the market… Over time, we are seeing a shift away from greenfield housing development in most capital cities towards infill higher density development…

The 2011 Census reported that across the separate house category, the most prevalent number of bedrooms is 3 bedrooms (49.6%) and 4 bedrooms (32.4%). When you combine the results for semi-detached and units the most prevalent number of bedrooms is 2 bedrooms (50.1%) and three bedrooms (28.6%). To look at it another way, 88.8% of detached houses have three bedrooms or more compared to 66.9% of units having 2 bedrooms or fewer. The point here is that if you are going to deliver more units to the market, they typically have fewer bedrooms and therefore are likely to have a smaller average household size than a detached house would. As a result, it is likely that as the delivery of units increases there actually needs to be a greater number of units constructed in order to cater for population growth than there would have been if houses were exclusively built.

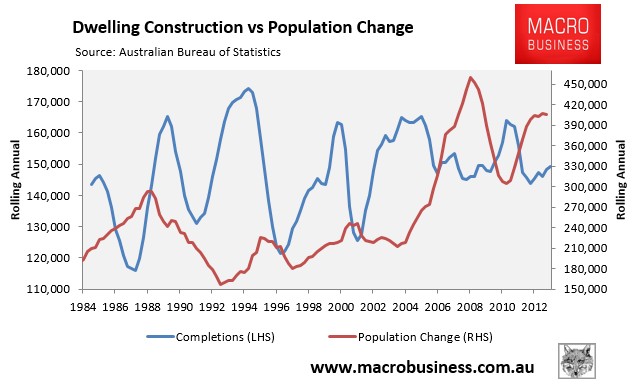

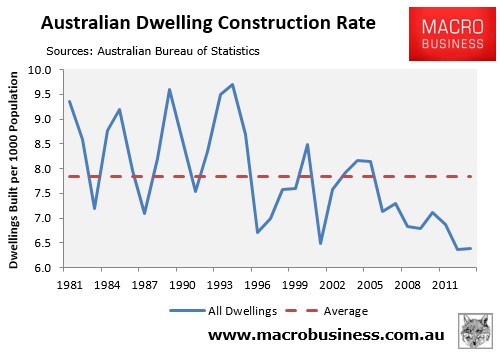

Any objective analysis of Australian population and dwelling construction data would conclude that Australia’s supply response has been very disappointing, particularly in light of the massive surge in values since the late-1990s (which in any well-functioning market would have induced more supply).

Advertisement

The below charts, plotting actual dwellings built against population, highlight the problem, with population growth far out-stripping actual supply, as well as the rate of dwelling construction collapsing over the past 15-years:

Advertisement

Kusher’s comment about the shift of construction towards apartments requiring more dwellings to be built is also a good one.

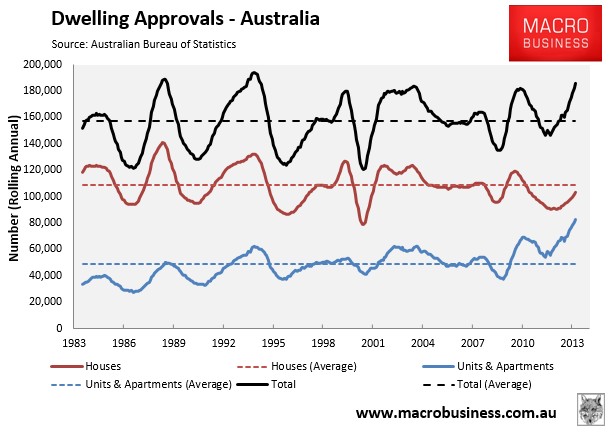

As shown in the next chart, the share of approvals taken up by units and apartments has risen to the highest level in history, hitting a record 45% of total approvals in the year to February 2014:

Advertisement

Given that apartments are much smaller than houses, any pick-up in construction going forward will need to be bigger in number terms than previously has been the case, in order to keep pace with Australia’s fast growing population.

All of which highlights the dire need for fundamental reform to Australia’s constipated supply system, including relaxing artificial restraints on land supply and the first-user-pays-all approach to infrastructure provision, as well as introducing a broad-based land tax.

Without reforms of this nature, new developments will continue to be priced above what many buyers are able or willing to pay, resulting in a disappointing supply response.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.