Oliver argues that there is very definitely evidence of overvaulation. On the basis of the ratio of house prices to rents adjusted for inflation relative to its long term average, he says, Australian housing is 27 per cent overvalued.

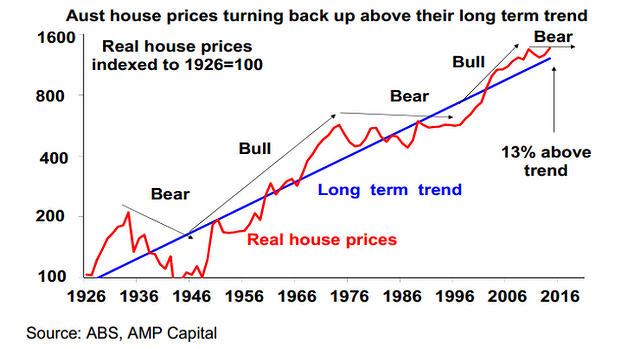

The chart below shows some of that overvaluation, along with his hypothesis that, with interest rates possibly starting to rise from later this year, property prices are likely to be “stuck in a 10% range around a broadly flat trend that we’ve seen since 2010”.

Like Bloxham, he points to an undersupply of housing as a prop for prices.

On the basis of the other two criteria for a bubble, Oliver points out that credit growth has been reasonably subdued, certainly compared to the big run-up in the late ’90s and early 2000s.

In terms of exuberance, he notes that: recent house price strength has been focused in Sydney and Melbourne, and then only really for one year; Aussies are paying down debt rather than using their homes as an ATM; and cooking shows are still out-rating home renovation programs.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.