Treasury Secretary Martin Parkinson’s defining speech at the Sydney Institute last night outlined in great detail the stiff headwinds facing the Federal Budget, which is facing decades of heavy deficits without major reforms to taxes and expenditure, as well as rising productivity:

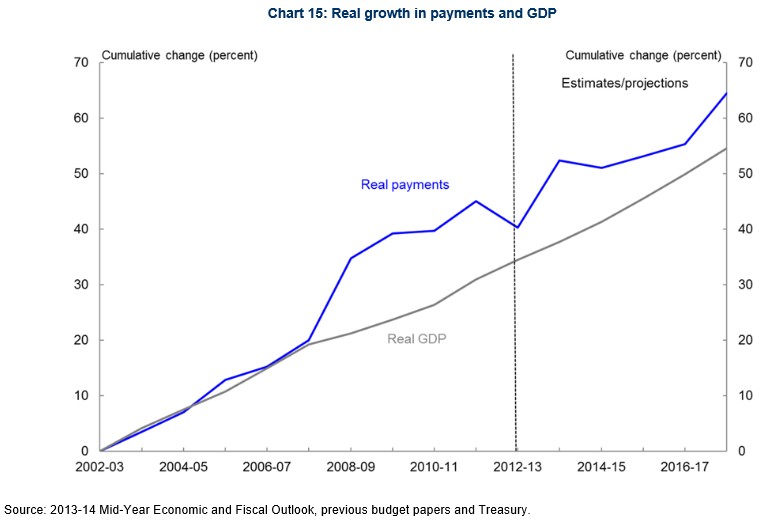

The case for action on the expenditure side can be seen by assessing growth in the share of real resources being used by Government between 2002-03 to 2017-18 (as measured by real growth in government payments and real GDP growth).

Even with the withdrawal of GFC-related stimulus measures by the end of 2012-13, real spending increased significantly more (40 per cent from 2002‑03) than real GDP (34 per cent from 2002-03).

This indicates an underlying increase in Government spending relative to Australia’s real GDP – in other words, growth in the real resources controlled by Government.

Furthermore, underlying growth in expenditure on social programs (driven partly by population ageing and, in the case of health, by technological progress and the rising demand that comes with rising incomes) will place added pressures on fiscal sustainability over the decades ahead. Let me illustrate some of these pressures.

It is widely known that the NDIS and School Reform funding will add $3.1 billion and $2.8 billion to total spending over the forward estimates, with the net cost to the Commonwealth of the NDIS to be $11.3 billion per annum by 2023-24, and with a total net cost of around $64.5 billion over the decade to 2023-24.

What is less well understood is that total Commonwealth expenditure on health is anticipated to rise from $64.7 billion in nominal terms in 2013-14 to $74.6 billion in 2016-17, and to $116 billion in 2023-24.

Similarly, our three main pension payments – the aged pension, disability support pension and carers’ payment – grow at an annual rate of 6 per cent per annum in nominal terms over the forward estimates, adding around $13 billion to annual payments by 2016-17, and another $39 billion to annual payments by 2023-24. Of this nearly $52 billion in additional payments in 2023-24, compared to 2013-14, over half is a result of indexation with the remainder due to increases in the number of recipients of the three payments.

So, what about action on the revenue side?

I have said before that, were revenue as a share of GDP to be at pre-GFC levels, much of our concern about fiscal sustainability might ease – at least for the immediate future.

But we cannot magically get back to those revenue shares.

For example, capital gains tax collections are around ¾ of a per cent of GDP lower than before the GFC, due to falls in asset prices and accumulated losses over the last half decade.

Some have suggested that if only personal income tax cuts had been avoided in the 2000s things would be better.

As a tautology, it is hard to fault that logic.

But if we had held on to that revenue, it may well have been spent on outlays rather than on tax cuts, meaning average earners would have faced higher marginal and average tax rates than they do now.

Even more importantly, had we held on to that revenue, it could have opened up another sort of problem.

That is, an ever greater than historical reliance on personal income tax to fund government spending.

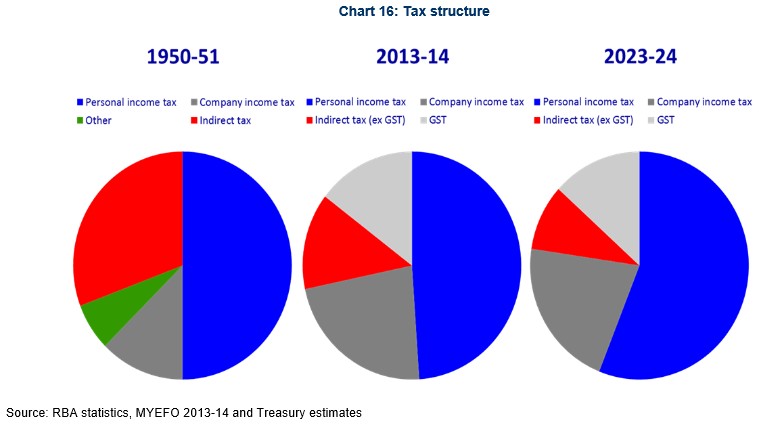

This chart shows the contribution made by personal income tax, company tax and indirect taxes to Government revenues in 1950-51, today, and as projected in 2023-24.

What we can see today is that, despite reforms that broaden the tax base (such as the GST), and decisions that have lowered corporate and personal tax rates across the decades, the share of direct and indirect taxes (as well as Australia’s reliance on income taxes) has changed little since the 1950s.

Australia has relatively high reliance on direct taxes as a proportion of revenue raised when compared to other OECD countries.

Research consistently says that reduced reliance on income taxes and increased reliance on other, more efficient sources of revenue, including indirect taxes, can support higher growth and higher living standards by increasing workforce participation and lifting productivity. Such a shift in Australia’s tax mix could also be achieved by lowering income taxes (offset by lowering spending) and leaving other taxes unchanged.

But if we turn to the far right panel of the slide, we see that, without conscious change, Australia’s tax mix will move in the opposite direction as personal income tax increases through fiscal drag.

We will move even further in this direction if, as we anticipate, the relative share of total indirect taxes (including GST) continues its long-term decline. Contributing to this decline is the non-indexation of fuel excise (unlike other excise rates) and a rising proportion of consumption outside the GST net, for example, in increased health expenditure.

It is hard to argue that this is either desirable or sustainable.

Continued increases in the personal income tax burden will hit lower and middle income earners with higher marginal and average tax rates. This will have adverse labour force participation impacts, while sharpening incentives for tax minimisation by higher income earners.

Meanwhile, in our increasingly globalised economy, Australia, like other countries, will face pressure to reduce the company tax rate to maintain competitiveness and reduce incentives for profit shifting – obviously, such actions would come at the cost of further eroding government revenues.

Given the pressure to return fiscal drag and to reduce the burden of corporate income tax, it will be a challenge to maintain the current levels of revenue over the medium-term, let alone the increases required to achieve the budget projections…

Dr Parkinson is right on the money. With Australia’s population ageing, the Budget is facing a tight squeeze from both lower receipts and higher aged-related spending.

Advertisement

This is why I keep calling for a range of reforms to the retirement system, which is one of the biggest and fastest growing areas of Budget expenditure, and also the area of expenditure that is most poorly targeted. Such reforms should include tighter means testing of the aged pension, such as inclusion of one’s owner-occupied home in the assets test (or part thereof), as well as reducing superannuation concessions for higher income earners. Otherwise, today’s generation Xers,Ys and Zs will become a generation of tax slaves, forced to pay more tax (and consume less) in order to pay for the generous entitlements provided to the old.

Reforms also need to be undertaken to broaden the tax base and shift some of the burden away from workers, whose relative size is shrinking as the population ages and the proportion of retirees rises.

As illustrated beautifully recently by The Guardian’sGreg Jericho, Australia has one of the highest reliance on company and personal taxes in the OECD, but also one of the lowest shares of revenue raised through consumption taxes:

Advertisement

Of all nations in the OECD, we rank third in the amount of company tax revenue we raise as a percentage of our GDP. While we are less highly ranked on income tax revenue, what is really striking is how little we raise through value-added taxes – like our GST. Of the nations that have such taxes (the USA doesn’t), Australia takes in the second least amount relative to its GDP. And, given Japan’s consumption tax is about to rise from 5% to 8%, pretty soon we’ll be the lowest.

What is worse, the proportion of revenue raised from personal taxes is set to rise through bracket creep, whereas the share of taxes raised through the GST and fuel excise will fall over time. The share of GST revenue will decline due to the exemption of the faster growing areas of consumption expenditure – food, health and education – whereas the share of excise revenue will fall because it is no longer indexed to inflation.

Raising the rate of GST and broadening its base is a sensible approach. As the Henry Tax Review showed, both company tax and personal taxes have “a high marginal excess burden” (i.e. a big loss in consumer welfare relative to the net gain in government revenue). This is because company taxes are “applied to capital, which is highly mobile”, whereas personal taxes can discourage work. By contrast, GST is relatively efficient, since it is broadly applied, is difficult to avoid, and does not significantly distort behaviour (see next chart).

Advertisement

While there are potentially negative equity effects from raising or broadening the GST, since the burden of reform would fall most heavily on lower income earners, the same could be said for allowing income taxes to rise via bracket creep. As illustrated by Ross Gittins earlier this week:

The average full-time wage next financial year, 2014-15, will be about $76,000. On the basis of reasonable assumptions about the growth in wages over the three years to 2017-18, you can calculate that someone on half the average wage would see the proportion of their wage that they lose in tax increase by 3.5 cents in the dollar.

For someone on the average wage the increase would be 2 cents in the dollar. On twice the average wage it’s 1.1 cents. And on six times the average wage it’s 0.8 cents.

Now that’s regressive.

Advertisement

That said, a broadening of the GST tax base to health could be problematic, since Governments already subsidise health to the tune of 70¢ in the dollar. Therefore, increasing the cost of health means you also raise the cost to government, effectively creating a money round-robin.

Nevertheless, there are compelling reasons to raise the GST (or broaden its base) on Budget sustainability grounds, to reduce the tax burden on the shrinking working-aged population, and to improve efficiency and productivity.

Other sources of taxation that should be considered are broad-based land taxes and mineral rent taxes (back to the future, I know). While not shown in the chart above, both taxes would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since they would be applied to a tax base that is completely immobile – land. In fact, the only loss in efficiency cause by land taxes would come from them being applied non-uniformerly to different land users (as occurs with municipal rates), thereby distorting the pattern of land use. They are also more equitable than consumption taxes.

Any discussions on tax reform should, therefore, include implementing taxes on land/resources alongside raising/broadening the GST, in place of less efficient and/or inequitable sources.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.