From the SMH:

…According to the latest data compiled by the Australian Securities and Investments Commission, short sellers appear to be circling Atlas rather than their traditional target in times of iron ore weakness, Fortescue.

The percentage of Fortescue shares sold short has barely changed since the bull market for iron ore in late October 2013 and was standing at 5.45 per cent at the last count on May 12. The percentage of Atlas shares sold short over the same period has more than doubled, from 4.84 to 11.53 per cent.

The differing mood appears to reflect growing confidence in Fortescue’s ability to service its debt. Atlas was debt-free in September 2012 but now has a fully drawn $272 million debt facility.

Atlas’ inability to secure a rail solution for some of its stranded iron ore deposits also appears to have attracted the shorts.

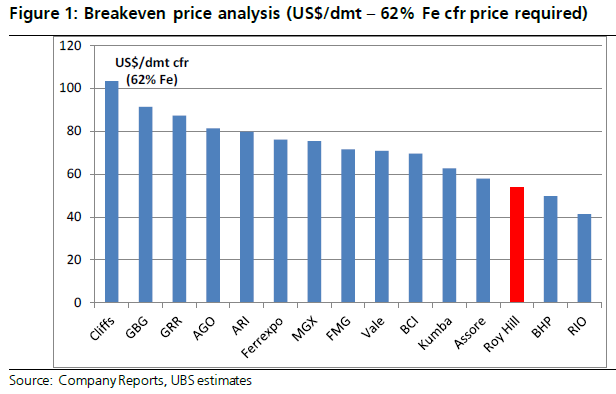

For the most part I focus on the basics of the cost curve in judging which miners will be in trouble. AGO is rightly under more pressure than FMG but I still reckon both are fighting for their lives. To me the debt is only half of the story, the supply surplus and what it’s going to do to the spot price is the other half. Again, here’s the UBS gauge of break even costs:

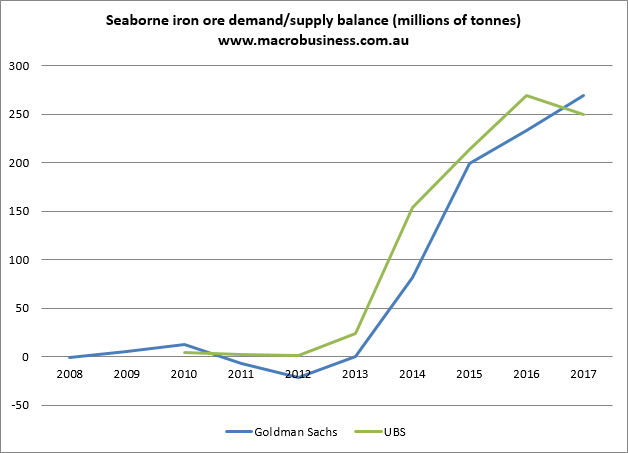

There are roughly 90 million tonnes per annum (mtpa) of iron ore ahead of FMG on the seaborne cost curve, which sounds reassuring. But here are the Goldman Sachs and UBS estimates of the coming surplus in seaborne ore:

Remember that this already assumes a decent amount of Chinese ore being knocked out and that steel output keeps growing in the low single digits.

Markets guess that the current surplus hitting the price is somewhere above 50 million tonnes. Imagine what 250mt will do.

It’s just not going to happen. The three majors – BHP, RIO and Vale – have sunk their costs already and are going to pump come what may. Take out the 90 mtpa above FMG and you still have a massive surplus roughly the equivalent of FMG’s entire output.

Make of that what you will.