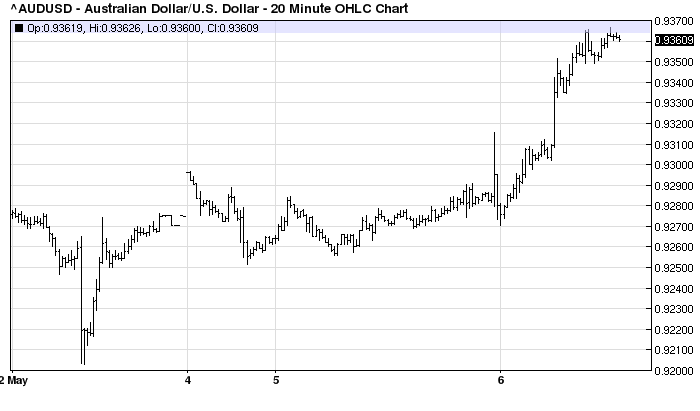

You can’t keep a good battler down and the Aussie is refusing to buckle. A benign central bank, war in Ukraine, Chinese property bust and tumbling iron ore price is just not enough!

More seriously, the source of local currency strength is easy pinpoint today. It is weakness on the on the other side of the coin, the US dollar:

The greenback basket has quite suddenly tanked and is sitting on a very important support level with a very bearish descending triangle chart. There was no apparent weakness in data for the move but a swag of sell side banks all downgraded US Q1 growth to -0.6% at Goldman and -0.8% at JPMorgan. That seems to have convinced markets that taper and/or rate rises are, at best, delayed.

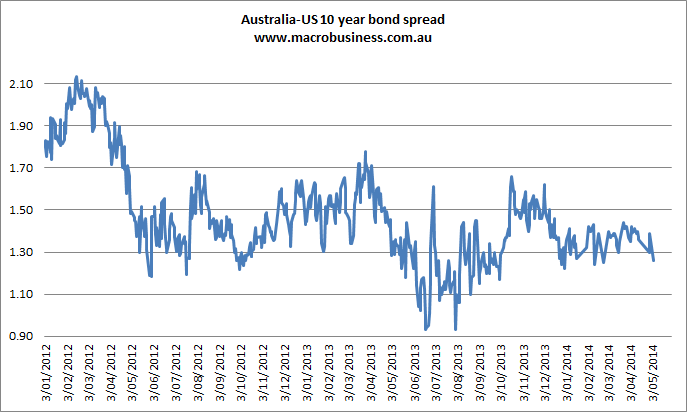

The forex move is all the more whacky given that the yield spread between the US and Australia is falling and threatening to break down:

We might take some comfort from the fact that the US dollar also fell heavily against the pound, loonie, krona, real, kiwi and the usual “risk on” suspects but none of them outpaced the South Pacific peso.

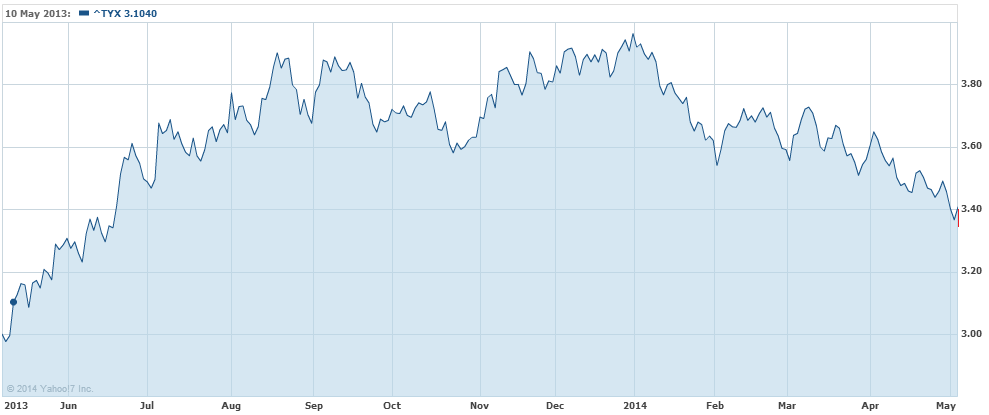

Markets are all over the place, frankly. It may be risk on in forex but it’s risk off in bonds and stocks. The latter fell 1%, led by more Nasdaq pain. The US 30 year was bid strongly again and yields are in free fall at 3.37%:

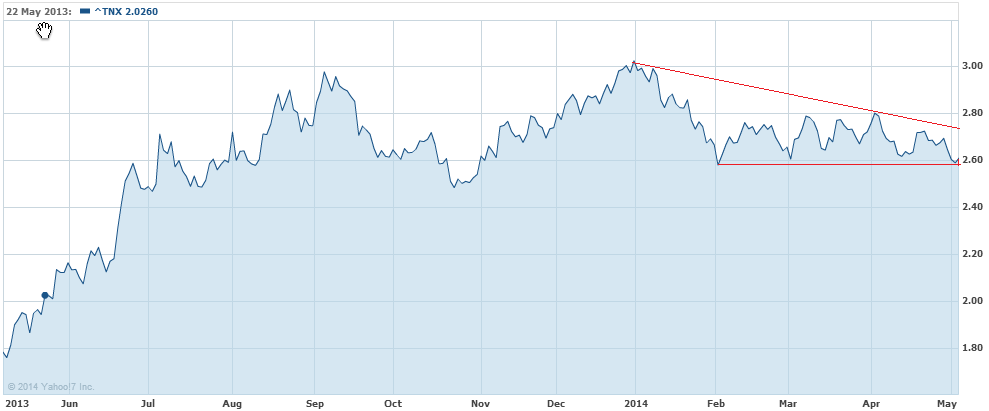

The 10 year yield is right on crucial support at 2.59% and looks likely to break too:

Deutsche offers 11 reasons why:

(i) The Fed was right – the ‘stock’ effect is more important than the ‘flow’ effect, and the Fed’s large bond holdings, particularly at the back-end, will suppress yields far into the future;

(ii) The ‘flow’ is also bullish, given the scale of Fed QE relative to the shrinking deficit/issuance; and relative to the buying from other players including:

(iii) Central bank purchases of Treasuries;

(iv) Pension funds that are underweight duration and overweight risky assets after last year’s equity gains;

(v) Fed H.8 data shows Commercial banks are buying securities again, seeking yield/carry.

(vi) Against the above, there are very large net short leveraged positions – record CFTC Eurodollar shorts and very large 10yr equivalents;

(vii) Inflation data remains soft. Last week’s soft average hourly earnings and ECI data was notably benign.

(viii)The China/ BRIC/EMG impetus for global growth is still on the wane.

(ix) The Ukraine. The impact here may be subtle, at a minimum making Treasury shorts cautious.

(x) Equities reduced traction, has encouraged a global search for yield while lower vol has encouraged a shift toward carry.

(xi) Ongoing speculation of a lower terminal funds rate, including all the ‘secular stagnation’ talk.

Take your pick!

I see the move in the Aussie as part of a broader momentum trade in markets that will pass in time as the fundamentals of a grinding improvement in the US and grinding deterioration in China and Australia re-emerge.