I’m not going to pretend I know everything about iron ore. But I know enough to identify a novice when I see one. Business Spectator offers two today in Brian Soh and David Walker of StocksInValue:

Looking forward, the possible upside to the iron ore price is that the bad news could now be priced in and any unexpected good news would likely trigger a squeeze of short positions. This could happen, for example, if the Chinese authorities introduce fresh stimulus to meet their growth forecast of 7.5 per cent.

The downside is further weakness in iron ore, caused by bullish production guidance by miners, renewed softening in China’s property market and slippage in China’s economic growth.

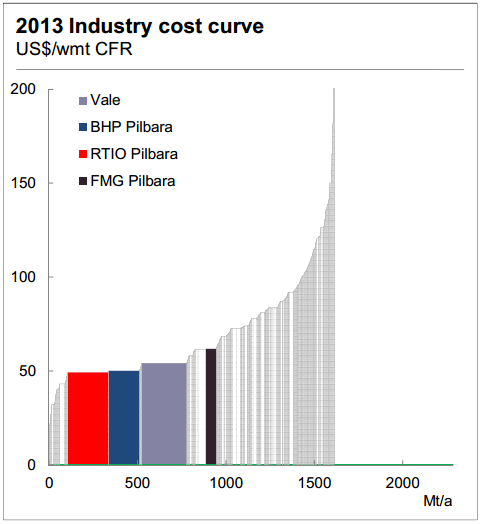

We can see that BHP Billiton, Rio Tinto, Fortescue Metals and Brazil’s Vale are at the lower end of the global cost curve and are well-positioned, as they remain profitable down to $50-60/tonne.

That cost curve is in wet metric tonnes. It is not China CFR which is a truer indication of break even points. FMG will get killed with iron at $70, let alone $50-$60.

UBS estimates its break even in the low $70s. But you also have to factor in that it does not receive the 62% benchmark price for all of its ore, much of which is below benchmark grade. These grade discounts mean it would struggle if the benchmark price is at $80 for a sustained period (all things equal such as the dollar).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.