Here are the Budget’s major economic assumptions:

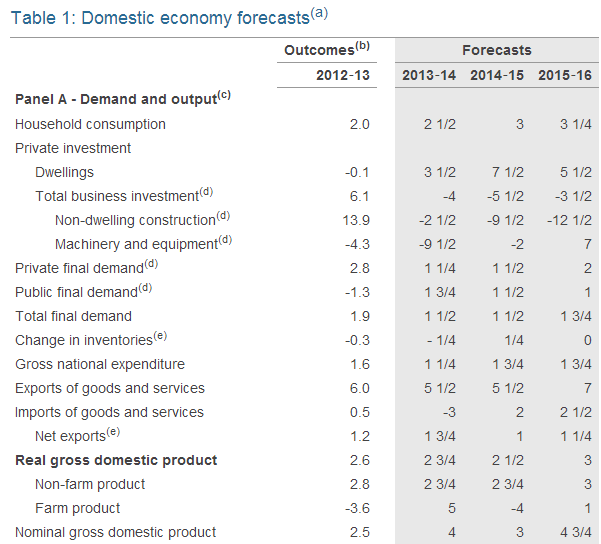

Growth for this year has been rounded up slightly from 2.5% to 2.75%, whereas growth in 2014/15 and 2015/16 has been left unchanged from the MYEFO at 2.5% and 3%. Somehow, we’re supposed to grow at 3.5% after that.

Perhaps most importantly, despite swings and roundabouts, public final demand has actually risen from MYEFO’s 1% this year and next, to 1.75% and 1.5% next year. The Budget has been stimulating more than reckoned this year though the fiscal drag will kick in as we move into next year and beyond.

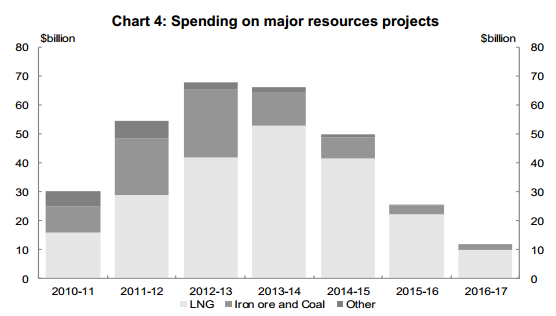

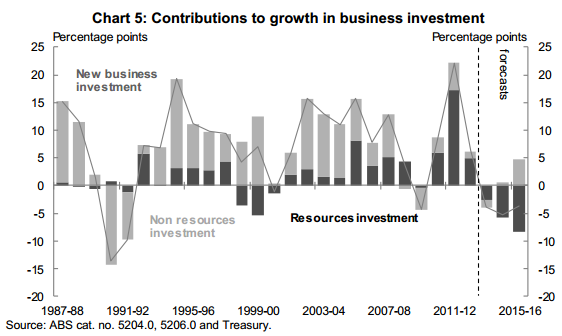

The capex cliff has finally been acknowledged with sizable write downs from MYEFO. The original saw business investment falling 1.5% in 2013/14 and 2% in 2014/15, they have now become -4% for this year, -5.5% for next year and still -3.5% in 2015/16. This is despite rounding up the housing investment component. Finally, they are credible:

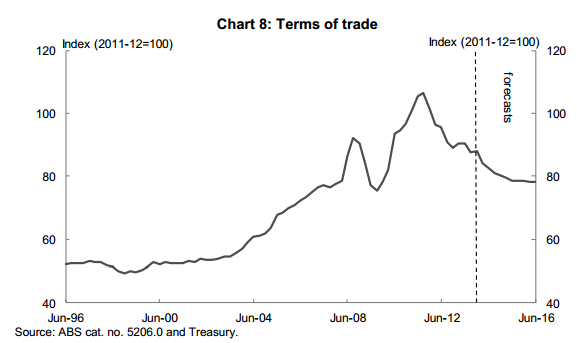

The terms of trade correction has also been written down further still from -5% this year and next in the MYEFO to -5% and -6.75% next year:

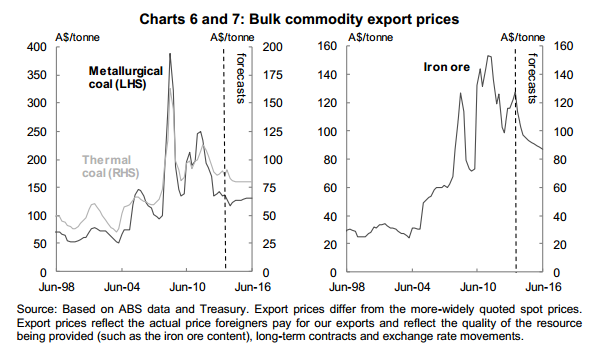

The reasons are appropriate with coal prices expected to remain weak and the iron ore price expected to keep weakening:

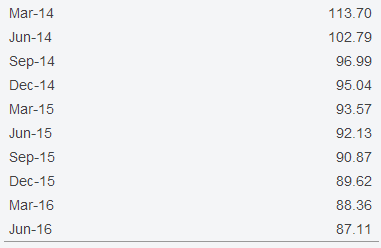

Note that these are realised prices, not spot, that take into account contracts, quality discounts and are in Australian dollars. Here are the assumed prices:

Add $7 for the equivalent spot price. Treasury is still too bullish.

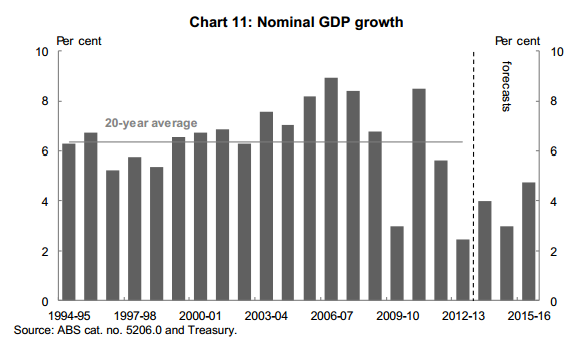

The weak terms of trade are nonetheless enough to keep nominal growth very soft. The changes from MYEFO are significant. This year has been rounded up from 3.5% to 4%. Next year has been cut from 3.5% to 3% and 2015/16 rounded up to 4.75%:

This will be the figure that most aggravates Labor media attack dogs. But it is right in my view.

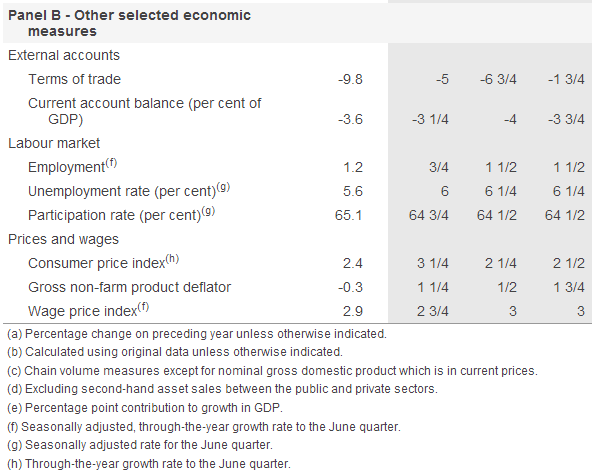

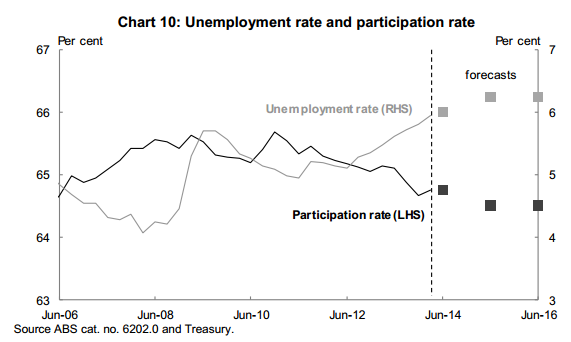

Unemployment projections are unchanged at 6% for this year and 6.25% for the next two years, despite ongoing declines in the participation rate (which is fair enough given the aging population):

Also reasonable given the capex cliff and unwind in major project employment.

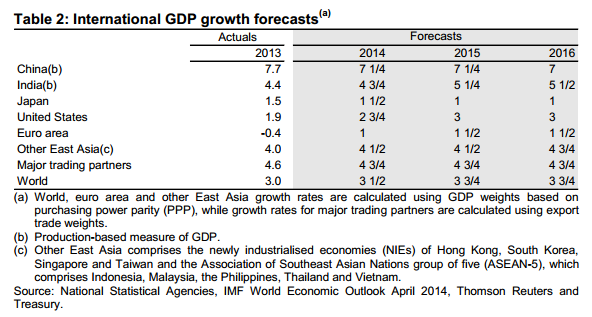

Finally, global growth projections are on the bullish side:

If China makes those rates of growth it will have completely failed to rebalance. Japan and Europe look fair and the US slightly aggressive. I would have had Chinese growth at 6% next year and hence would also have iron ore and the terms of trade lower. But the Budget also assumes that the dollar will remain at 93 cents, which it will not if I’m right about China and iron ore, so the contingency of lower Chinese growth and lower commodity prices is insured via an aggressive dollar forecast.

All in all, these assumptions are more than reasonable and the basis upon which Budget rebuilding can take place for the first time in three years.