Westpac and MNI recently launched a new Chinese consumer confidence gauge, which was quite bright of them, and its first result is out today:

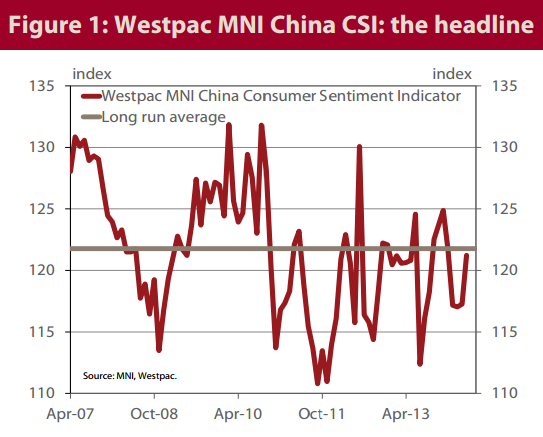

• The Westpac-MNI China Consumer Sentiment Indicator, hereafter the Westpac-MNI China CSI, rose from 117.3 in April to 121.2 in May, a 3.4% change over the month and 0.4% over the year. The May outcome is 0.3% below the long run average. The survey indicates that the anxieties gnawing away at the Chinese consumer through the first four months of the year lessened considerably in May.

• The current conditions composite increased by 3.1pts to 114.3 and the forward looking composite increased by 4.5pts to 125.8. Both current and forward looking family finances improved by more than the headline, as did business conditions one year ahead. Buying conditions for major household items and business conditions five years ahead lagged the rate of improvement seen in the above items, with the buying conditions index recording a relatively sluggish 1.2% gain over April. Business conditions versus a year ago (not part of the composite) moved 3pts higher, offering a useful cross-reference for the unexpectedly large improvement in the flash HSBC PMI.

• The outlook for employment took a turn for the better in May, consistent with the aformentioned responses regarding business conditions and family finances.

• Consumers’ attitudes towards real estate were noticeably firmer in May, despite the steady drumbeat of pessimism in both the local and international media. House price expectations increased notably in May, fully reversing their steep March-April dip. Consumers appear to be looking through recent updates on house prices that indicate that weakness is now more widespread than earlier in the year, with both the new and secondary dwelling markets visibly deteriorating. Countering that, selective policy easing has been announced in terms of both mortgage lending and local controls on investor activity. Consumers are expressing a collective faith that policy will eventually carry the day.

• Car purchasing conditions improved appreciably in May, to be 5.2% above the long run average and 1.9% above the level of a year ago. Passenger car sales growth has decelerated in the year to date, but this latest update looks promising for the second half of the year.

• Inflation expectations are 1.9% below their long run average following a modest increase in May. The official CPI target of 3½% for 2014 is unlikely to come under any significant threat, which should allow policymakers greater flexibility as the year goes on.

• Fewer investors were prepared to call stock prices higher over the next three months, after the exuberance of April.

• On the basis of the survey, Westpac remains comfortable with its current forecast of 7¼% GDP growth in 2014 but has raised its expectations for the May official data round, including next week’s NBS PMI.

Interesting that house price sentiment remains very bullish. Full report here.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.