Right on cue, Terry Ryder responds to today’s Tax Office release showing Australia’s enormous rental property losses with a riotous post in Property Observer, arguing that removing negative gearing “would make many matters worse”. Let’s examine some of Ryder’s logic:

“One of real estate’ core issues is the low level of residential yields in the major cities. This is because residential rents are too low, relative to sale prices.”

Funny how Ryder doesn’t state it the other way – i.e. that home prices are too high relative to rents.

Anyhow, back to Ryder:

The cure-all beloved by many with loud voices attached to soft brains is to eliminate negative gearing tax benefits…

But removing negative gearing would solve nothing. Rather, it would make many matters worse.

The fuzzy logic that leads some to believe it would do good is that price rises are caused by investors – and that property investors are essentially driven by negative gearing benefits.

But price rises are not caused by investor activity, in most cases. Investors are a minority force in the market and are motivated to buy, without emotion, at the lowest possible price.

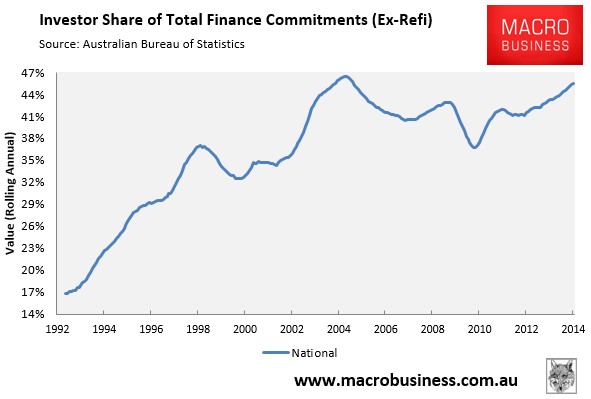

No Mr Ryder. According to the ABS’ housing finance data, property investors accounted for a whopping 46% of total housing finance commitments (excluding refinancings) in the year to February 2014. Moreover, their share has more than doubled since the early-1990s, which by coincidence also covers the period when Australian home values exploded (see next chart).

To ignore the growth of property investment is to ignore reality.

Back to Ryder:

So eliminating negative gearing may slow down investor buying but it won’t cause prices to fall.

What it will do is cause rents to rise – a lot. Without the tax offset, residential property as an investment will lose its appeal for some, especially those buying in the major cities. A shortage of rental properties will develop quite quickly, as happened last time negative gearing was eradicated (before being rushed back in). Sharp rises in city rents will follow.

Here we go again. The old “removing negative gearing would cause a shortage of rental properties and rents to rise” myth.

First, why would property investors campaign so hard against a reform that would raise rents? Think about that one.

Second, the claim that negative gearing’s removal would harm the rental market is complete bunkum.

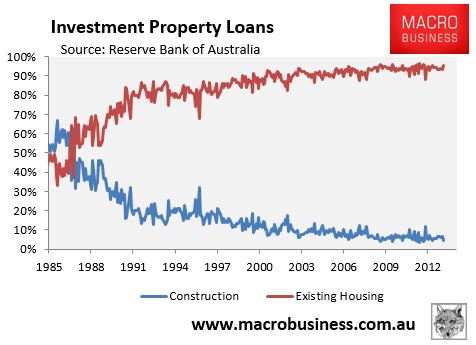

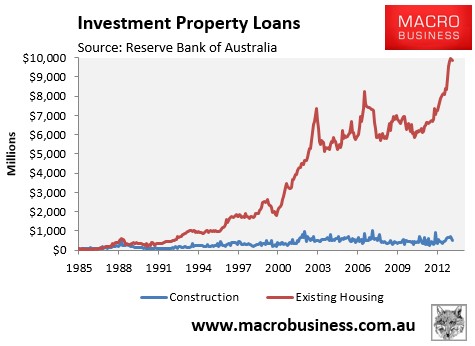

As shown time and time again on this blog, the overwhelming majority of investors purchase existing housing (see below charts).

And since investors primarily purchase existing dwellings, negative gearing in its current form simply substitutes homes for sale into homes for let. Accordingly, the policy has done little to boost the overall supply of housing or improve rental supply or rental affordability.

Ryder’s claim that the quarantining of negative gearing in the late-1980s caused rents to spike is also demonstrably false. The below chart plots the Australian Bureau of Statistics (ABS) rental series from 1972, with the period where negative gearing losses were last quarantined (i.e between June 1985 and September 1987) shown in red. As you can see, there was nothing spectacular about this period, with much higher rental growth recorded in earlier periods when negative gearing was in place:

Moreover, if we deflate the above series by CPI, in order to remove the effects of inflation, we again see that rental growth over the period when negative gearing was last quarantined was nothing special, with periods of higher rental growth recorded both prior to and subsequently:

In the event that negative gearing was wound-back and a proportion of investment properties were sold, who does Ryder think these homes would be sold to? That’s right, they would be purchased by renters (or other investors that would rent them out). In turn, those renters would be turned into owner-occupiers, reducing the demand for rental properties and leaving the rental supply-demand balance unchanged.

Back to Ryder:

The other factor never discussed in this increasingly wacky debate is the longer-term impact for the nation. Australia wants its citizens to invest to create retirement nest-eggs, thereby easing the growing budget burden from paying pensions to an aging population.

I’ve heard people argue that the federal budget could save billions each year if it wasn’t paying out on negative gearing tax breaks, but the long-term cost would be far greater if Australians stopped investing in residential property to provide for their retirement.

Seriously, I have never heard such a ridiculous argument. As illustrated beautifully in Saul Eslake’s 50 Years of Housing Policy Failure presentation, Australia’s home ownership rate has decreased over the past 50 years, despite favourable demographics (see next chart).

Surely, the best way to ensure people’s security in retirement is to increase access to first home buyers by making homes more affordable?

Australians would be in a far stronger financial position if they were not required to pay-off some of the world’s biggest mortgages, thanks to egregious policies like negative gearing.

unconventionaleconomist@hotmail.com