Something of a slow dawn is going on at Morgan Stanley today:

While considering potential metal and bulk commodity price direction the rest of the year, we found it useful to look through the lens of the increasingly divergent coal markets. Global seaborne metallurgical and thermal coal markets are in oversupply. According to our estimates, the met coal surplus is ~10 million tonnes (3.5% of 2014 demand) and thermal ~35Mt (4.1% global demand).

However, marginal met coal producers appear to have met their maximum pain threshold: Some suppliers in North America and Australia in the past month have idled export-bound output and we have tracked ~14Mt of supply cuts so far this year. The spot met coal price has since shown modest signs of recovery, suggesting the supply response created a price floor and could contribute to a further rebound.

Meanwhile, thermal coal producers are choosing operational rationalization instead of cutbacks: Prices are clearly not yet low enough to prompt a production response and miners are continuing to cut costs and hope the demand recovery will be enough to boost prices. To us, this suggests either we have not yet seen a price floor or prices could linger at current levels for the remainder of the year.

Is there a read-across to other commodity markets? Most metal and bulk commodity prices remain in the doldrums, despite a broad-based improvement in global consumption trends. This suggests supply side trends could be the key catalysts in these markets for the remainder of the year:

…Iron ore demand is resilient, with Chinese and global crude steel operating rates at record highs. However, an increasing amount of supply is entering the market and while we can anticipate a near- term rebound, it is tough to remain price positive when market surpluses are expected.

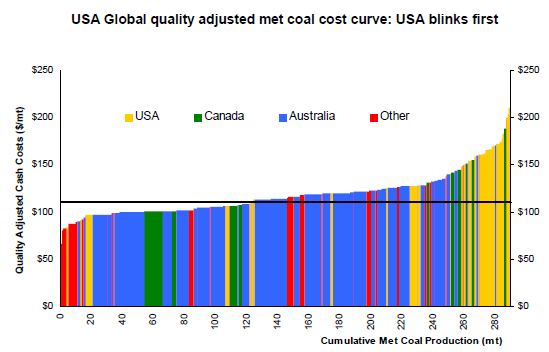

Here’s some back of the envelope calculations for you. The coking coal seaborne market is roughly 320 million tonnes (mt). So the 25 mt surplus that has driven prices down 70% from their highs was driven by a surplus a little over 7% of the total market. And check out how far down the cost curve prices have fallen too shake out production:

The total seaborne iron ore market is about 1200mt. The forthcoming surplus on existing projects is projected by Goldman and UBS to be around 250mt in 2015, in a low demand growth scenario that is a more than reasonable base case. That makes for a surplus roughly 21% of the total market.

Now, I know that there is less geographic dispersion and competition in the iron ore market. But that surplus is enormous. The numbers are rough but they’re so bowel-shakingly huge that it really doesn’t matter if they’re considerably wrong. The underlying truth remains.

So, if a 7% surplus killed the coking price by 70%, ask yourself, what does a 21% surplus do to the iron ore price? It’s down roughly 40% from its high already but if it replicates coking coal and falls 70% then it is headed for $55 where it will sit for several years.

That’s not a forecast but it is surely enough to raise a few doubts, no?

Not for Fairfax’s Max Mason in Singapore, reporting faithfully on his junket where Vale’s global director of marketing reckons:

“We are increasing our production. Of course there will be some pressure in terms of price, but our growth more than compensates the pressure in price,” Mr Alves said, while speaking at the Singapore Iron Ore Forum.

“We have to look to the mass production of iron ore in China, where conditions are continually deteriorating, both in terms of the productivity cost and quality, so all of this gives Vale the right way for us to come with new capacity. Our new capacity will come with lower costs, with better quality, so we don’t think believe it will be necessary [to slow production],” Mr Alves said.

The market is too bearish on iron ore, said Fortescue Metals business development group manager Zhuang Binjin, and the long-term outlook for the metal remains stable and strong.

Record high steel inventory levels may have a short-term effect on the iron ore price, but that is of no concern to Fortescue, said Mr Binjin, with the miner reducing cost of production.

If you believe that I’ve got a bridge to sell you. Rebar futures have opened another half percent down and Dalian iron ore future have slipped slightly at the open.