Reuters has a good piece today from Andy Home:

The existence of a magic number below which the price of iron ore cannot sustainably stay is widely accepted, although there are as many magic numbers as there are analysts.

But most think that it’s there somewhere in the $100-120 per tonne range.

…Of course the size of that surplus holds the key to how much higher-cost production must be forced out and at what price.

Hence the current focus on how the big expansions in Australia’s Pilbara are faring. Very well, in the case of the big three producers, Rio Tinto, BHP Billiton and Fortescue Metals, which has caused some analysts to adjust their time-lines.

Forgotten, though, in this current fixation on the supply side is what is happening on the demand side of the iron ore equation.

Even with multiple signs of recovery in steel demand in the rest of the world, it is China that holds the key…China’s steel sector is moving up through the gears…There’s just one small warning light flashing.

It’s the third time this year that exports have soared past the 6.0-million tonne mark. The cumulative year-to-date total of 25.87 million tonnes is up almost 30 percent from last year’s equivalent level.

…That so much material is seeping out of China at what should be a seasonal high point for its own demand is telling.

And it’s not hard to figure out what the problem is. Just about every signal coming out of the country is pointing to trouble in the construction sector.

Prices are down, sales are down and new construction is down.

…It is the elephant in the room in a market which is now obsessing about supply. If unleashed, it could trample all over everyone’s magic support numbers.

…Hear that sound? Is it just me, or does that sound like an elephant approaching?

Precisely. There are several demand side risks that have not yet been discounted by markets:

- China will face resistance to dumping steel. There are already moves to stop it in the US and others will follow given the distortions of public ownership in China and the strategic nature of steel production to nations. That will mean that the export outlet for excess Chinese production will be squeezed some time in the medium term and when it does its local steel price will come under even more pressure. Rationalisation is the end point with bankruptcies and gapping in the iron ore price.

- The second risk is that Chinese property spirals. Nobody knows if the correction is cyclical or structural (I lean towards the latter) but either way it appears Chinese authorities are in no hurry to rescue the market. The bit by bit approach to loosening we’ve seen so far looks likely to continue and I expect a downturn at least as bad as that of 2012 (otherwise how can Li and Xi claim to be reformers?) which is some way below yet:

The construction downturn started earlier in the cycle this time but it’ll still need at least stable prices and sales to grow starts once more.

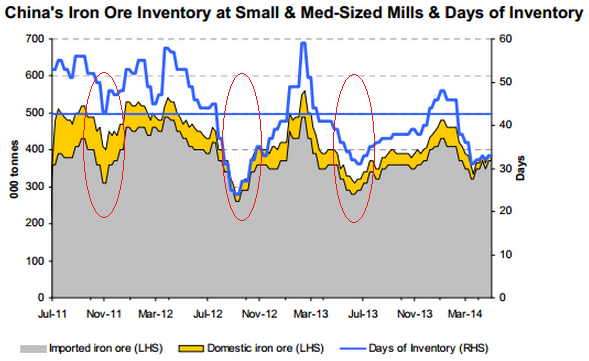

This, and the big port pile, is primarily why I think we face a 2012-style risk of a crash in the iron ore price later this year in Q3 when seasonal destocking of raw materials takes a hold at steel mills (chart from Morgan Stanley):

I’ve circled the destocking episodes of the past few years. Note that it arrived earlier in 2013. This time days of inventory is lower than previous years but that is offset by the giant port pile and mills could drive inventories to new lows given abundant supply.

Destocking episodes of the past have taken $50-60 off the price. I’m not expecting a repeat of that but $25 down to $75 seems awfully plausible.