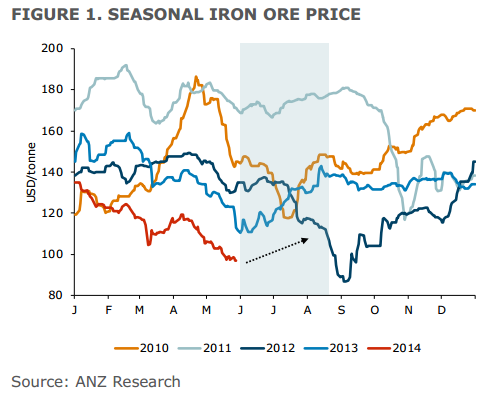

Expanded Australian iron ore exports are coming on quicker than expected which could trigger permanent closure of high cost Chinese iron ore supply. We estimate as much as 100 million tonnes of high cost Chinese iron ore supply could close this year if government efforts to consolidate (and clean up) the industry are successful. As a result, we think the key industry floor price, driven by China, is now closer to USD100- 105/tonne rather than USD120-125/tonne in 2013 (Figure 2). This level represents around the 90th percentile on the global cost curve.

As a result, we are revising down our price forecasts over the next three years by 10-13%. We now forecast iron ore prices to average USD110/tonne in 2014 from a previous forecast of USD120/tonne. We think current spot levels around USD90/tonne will be the low point of the year despite ongoing high supply – with a near-term relief rally and stronger fourth quarter restocking propping up end of the year prices to USD110/tonne.

Larger downgrades to 2015 and 2016 forecasts reflects the lower global industry floor price of USD100/tonne and the expectation that Chinese iron ore supply costs could be further reduced under a more efficient consolidated industry.

Some big cuts there but not big enough, Mr Pervan. There’s about as much chance of 100mt in Chinese production being knocked this year as there is of Australians cheering the Budget.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.