Last week, Statistics New Zealand released the national accounts for the March quarter, which revealed that real GDP in New Zealand rose by a strong 1.0% over the quarter to be up 3.3% over the year.

The headline result was slightly weaker than Australia’s, where real GDP increased by 1.1% over the March quarter and by 3.5% over the year.

Despite the weaker headline result, there is reason to believe that New Zealand’s economy is currently traveling far better than Australia’s, with Kiwis enjoying much faster growth in living standards than their Australian counterparts.

The difference essentially comes down to one factor: export prices and the terms-of-trade.

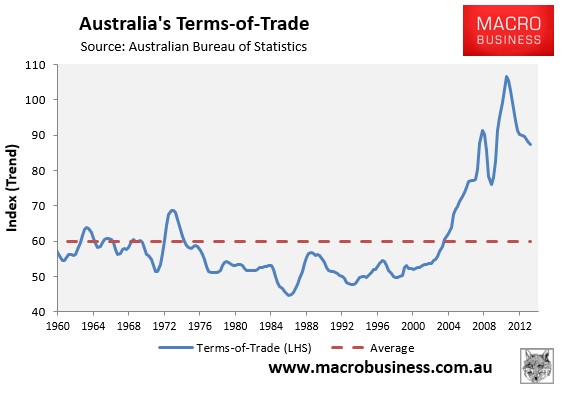

In Australia, export prices are falling, led of course by our biggest commodity export: iron ore. The situation is best summarised by the next chart, which shows Australia’s terms-of-trade – i.e. export prices divided by import prices – falling markedly since late-2011; albeit they remain highly elevated on an historical basis:

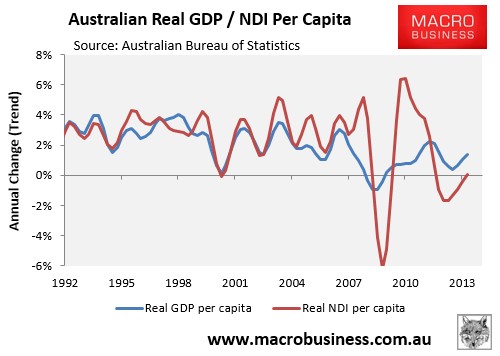

The fall in the terms-of-trade has acted to reduce national disposable income (NDI), ensuring that NDI grows at a much slower pace than output, as measured by GDP (see next chart).

In fact, after growing at a much faster pace than GDP since 2003, NDI has fallen for two consecutive years, courtesy of falling commodity prices and the terms-of-trade (see next chart).

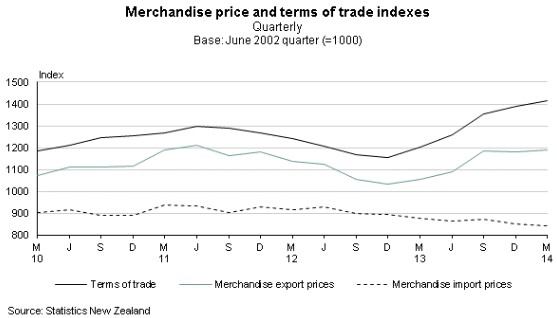

Now compare Australia’s situation with our cousins across the pond. There, the terms-of-trade has risen strongly in recent times (although will likely fall in the June quarter on the back of recent dairy price falls):

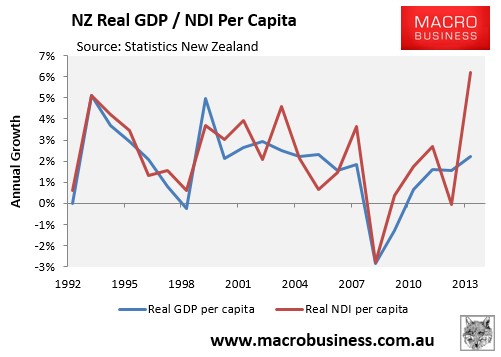

So much so that annual per capita NDI growth hit a whopping 6.2% in the year to March – the fastest pace of growth in at least 20 years, and well above the growth in per capita real GDP (2.2%):

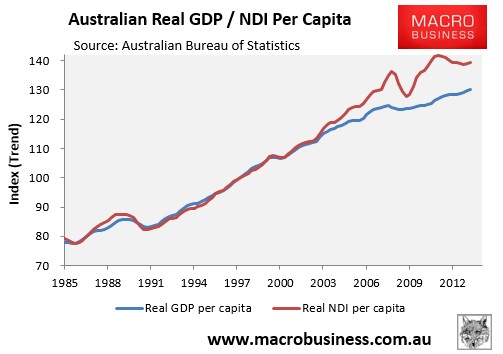

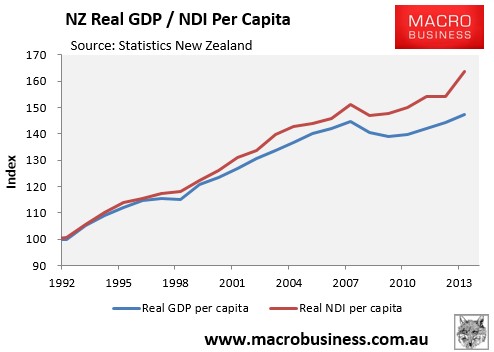

In turn, the gap between real per capita NDI and GDP in New Zealand is widening, in contrast to Australia (see next chart).

Looking ahead, one could logically argue that New Zealand’s economy is better placed to deal with the Chinese economy’s rebalancing away from fixed asset investment towards services and consumption.

New Zealand’s biggest export commodity – dairy – is likely to benefit directly from China’s emerging middle class, whereas Australia’s commodity exports – primarily used for Chinese construction and energy generation – will likely be a net loser from China’s transition to a services-led economy.

Thus, national incomes could very well grow at a healthier rate over the medium to longer-term in New Zealand than in Australia.