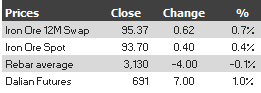

Here are the iron ore charts for June 25, 2014:

Paper and physical are grinding higher. But the Baltic Dry capeszie component fell another 3% and has largely reversed its recent hopeful bounce.

There is some kind of restocking activity going on but it’s muted. From Reuters:

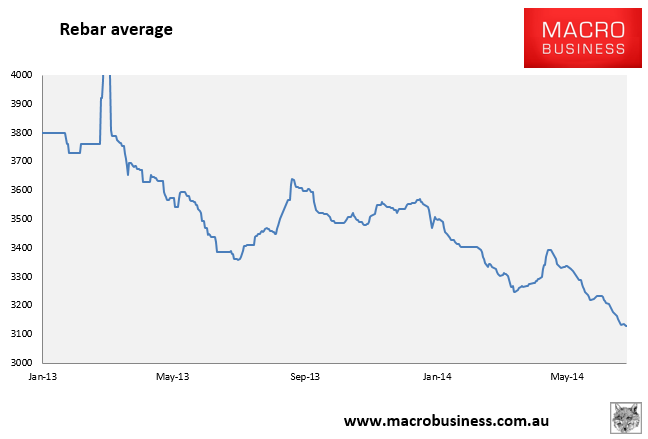

Shanghai steel rebar futures rose to their highest level since late May on Wednesday, propped up by expectations that traders would replenish stocks on hopes demand will pick up as the Chinese economy regains momentum.

The most-traded rebar contract for delivery in October on the Shanghai Futures Exchange was up half a percent at3,071 yuan ($490) a tonne by midday. It touched 3,086 yuan earlier, its highest since May 30.

Stocks of steel products held by Chinese traders stood at 13.53 million tonnes as of June 20, the lowest for that period since 2009, said Helen Lau, senior mining analyst at UOB-Kay Hian Securities in Hong Kong.

“I think we’re close to the end of destocking. If the inventory falls to 10-11 million tonnes, we might see traders start to replenish and by then we should see a more sustainable rebound in steel prices,” she said.

…”Traders holding imported material at Chinese ports attempted to lift their offers but saw little traction,” Steel Index said.

Yes, Shanghai rebar futures bounced a little. But rebar average is still falling and the prospect of a sustained steel restock as property slides seems to me to be optimistic.

The same goes for iron ore. My old mate and resident Business Insider bull Greg McKenna sees hope in the technicals:

It’s funny how Iron Ore price falls seem to get all the headlines but when it rallies – radio silence.

So, in the interests of balance, here is a chart of the September 62% FE Iron Ore swap futures contract.

Iron Ore at $95.13 this morning is up 7.29% off the recent low and has broken a three-month downtrend.

It’s a solid bounce and if it can get through the recent high at $95.77 a tonne then the outlook might have changed and a bottom might be in place.

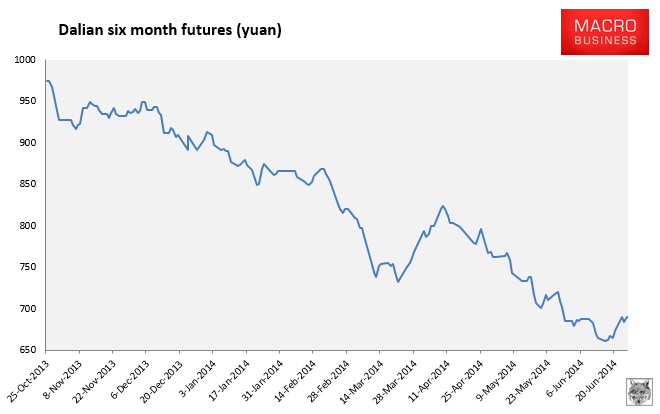

Actually, there are never enough headlines on iron ore, up or down, given its importance. But I don’t buy it. Iron ore restock rallies of substance rise 5% per day not 0.5%. We appear to have found a bottom for now but as long as Chinese property slides the risk of iron ore price weakness remains the primary driver of the stocking cycle.