The AFR has a report today claiming that the Western Australian Budget is facing a big hit to revenue as iron ore prices decline far faster than forecast in the Budget:

A sustained fall in the iron ore price could erase more than $1 billion from Western Australia’s debt-laden balance sheet…

The state government raises a large chunk of its budget from royalties on iron ore. The price dropped below $US92 last week, and is about $US30 below the price the state has used for calculating the value of its 2014-15 tax revenue…

The current $US30 differential, if maintained over 2014-15, would equal $1.47 billion less than forecast in the May state budget.

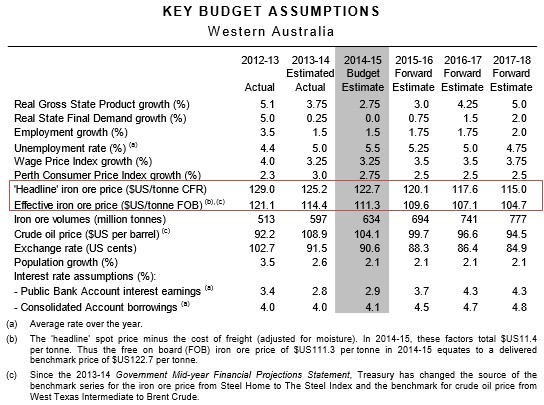

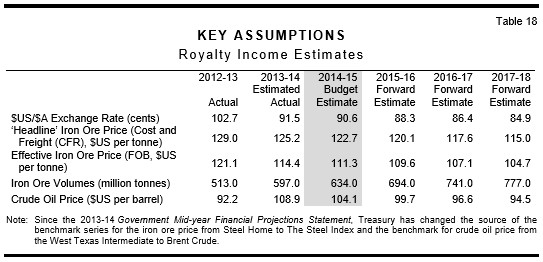

A quick look at the Budget Papers shows that the Western Australian Government has been highly heroic in its iron ore forecasts, tipping an average spot price of $122.70 over 2014-15, and only minor downward adjustments in the out years (see below table).

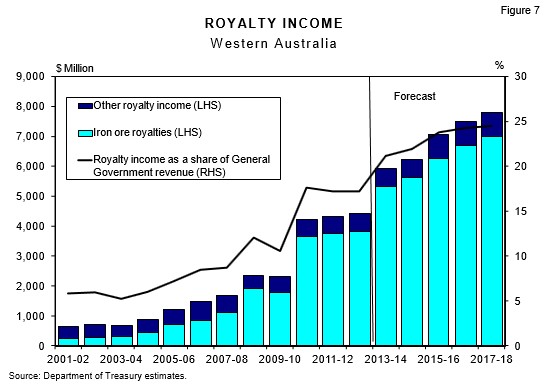

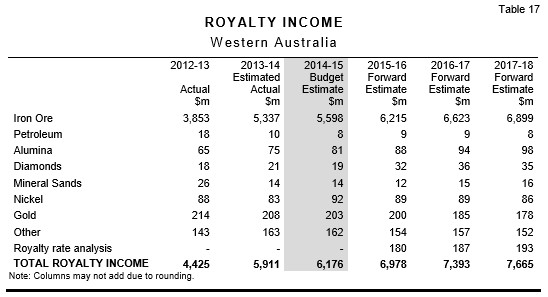

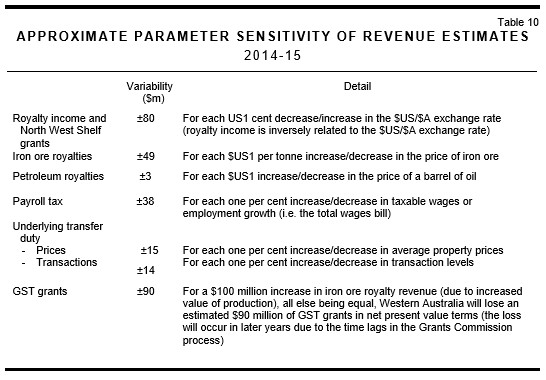

Mining royalties made up 21% of Western Australian revenue in 2013-14, which is forecast to increase to 24% by 2017-18, with iron ore accounting for about 90% of total royalty income across the forecast period (see below chart and tables).

And according to the sensitivity analysis contained in the Budget Papers, every $US1 fall in the iron ore price reduces Budget revenues by some $49 million:

Hence, the circa $US30 decline in the iron ore price, if maintained, could wipe some $1,470 million from Budget revenues in 2014-15.

Reading how Western Australia has devised its optimistic iron ore forecasts also does not instill confidence. First, the Treasury believes that demand will continue to rise strongly:

China’s iron ore demand is expected to grow by 3.2% per annum over the budget period, to reach 1.2 billion tonnes by 2017-18. Over the same period, demand from the rest of the world is projected to rise by about 3.5% per year to around 940Mt.

The continued urbanisation of China is likely to be a key driver of domestic consumption and new investment. In 1990, urban Chinese accounted for just over a quarter of the total population, but now they account for over half of the population. By 2030, it is estimated that urban Chinese will account for about 70% of the total population.

Based on United Nations data, around 90 million additional people are projected to move to cities between 2014 and 2018.

The Treasury also believes that higher cost Chinese iron ore supply will cease placing a ‘floor’ under the iron ore price:

Growth in low-cost supply is anticipated to place downward pressure on price. However, as prices ease, a substantial proportion of higher cost Chinese domestic iron ore production and output from ‘non-traditional’ producers may become unprofitable and withdraw from the market. Chinese iron ore tends to have a lower grade of iron content and therefore requires additional processing, which adds to the cost of production. It is estimated that about 50% of Chinese domestic production is uneconomic at an iron ore price of $US110 per tonne (based on Shanghai Metals Markets data). Chinese State-owned enterprises and integrated steel and iron ore producers may continue to produce at a loss for sometime before cutting output. This may result in volatility in the short-term, although as supply is gradually withdrawn, this should provide a floor to the price.

Both statements are too bullish in our view, leading to the type of overly optimistic price forecasts contained in the Budget.

In reality, Western Australia is likely to be ground zero in the coming iron ore bust.

unconventionaleconomist@hotmail.com