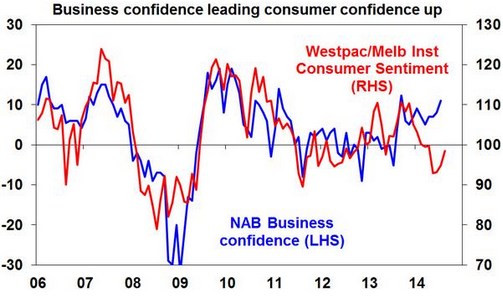

A chart here from Shane Oliver asks if business confidence is leading consumer confidence:

My answer is no, I still expect households to win this tug-of-war. As I wrote a last month for members:

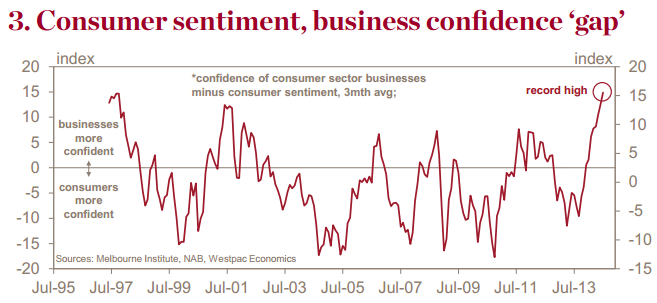

Last week saw the continuation of a recent divergence that’s going to play a very significant role in determining Australia’s growth rate in the year ahead. Consumer confidence remained weak but business confidence remained strong. Indeed, Westpac’s Red Book offered a spectacular chart illustrating that this divergence is now at its widest ever:

Why is this? Does it matter? And, which side of the sentiment coin is going to prevail in the economy?

I see four main reasons for the divergence – politics, debt, technicals and capacity utilisation – and each suggests a different outcome for the struggle.

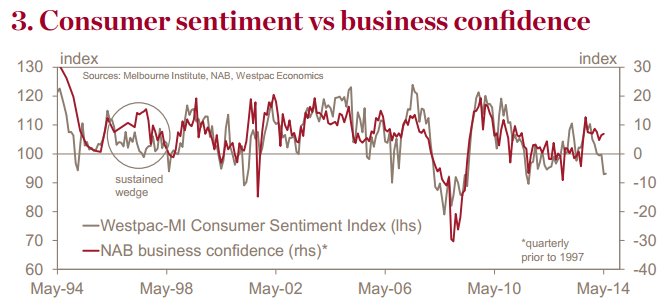

Let’s start with the technicals. The two survey’s used in the comparison are the NAB business survey and Westpac-Melbourne Institute consumer survey. The two usually track one another closely, however it is the consumer that usually leads and wins:

Note the circled period following the 1996 budget. That was the last time we saw a divergence of this magnitude. It persisted for 18 months but eventually it was business sentiment that capitulated. It’s not so obvious on this chart given the long time series but consumer confidence does usually lead business confidence in the Australian economy.

There are good reasons for why. In the ideal economy, business confidence rides high on a competitive edge and leads consumption by investing and creating jobs around that advantage. But in Australia we have a chronically uncompetitive economy that derives a huge proportion of its income from capital intensive, low employment dirt exports. It is only through the leveraging of that income that most domestic activity is generated and the primary mechanism for that is house prices (and more recently government debt). So, consumer confidence by definition leads business sentiment because the only reason to invest is consumer’s spending house price wealth effects (as opposed to the ideal of tradable and import competing advantages).

That leads to a second technical point. Because the resources sector’s importance so far outweighs its actual size, the NAB business survey under-represents mining (as do the Dun & Bradstreet and Roy Morgan equivalents). So, what we’re really looking at in this survey is weighted towards business confidence in the non-mining (read services) sectors of the economy. This will further exaggerate the fact that consumer sentiment leads business sentiment given it’s largely household spending dependent sectors that are being surveyed.

In short, the structure of the economy and the business survey suggest weak consumer confidence will pull down business confidence (and the any non-mining capex rebound) rather than the reverse.

There is a second, equally important, reason to think that this is the more likely outcome: debt. Since the GFC, the trends in Australian debt have seen historic changes. But the changes have been more stark for business than they have for households. Australian business has genuinely deleveraged and its balance sheet is squeaky clean. By comparison, households have done no such thing. They have disleveraged only, with an easing rate of growth in their debt accumulation. Ideally one would use income-to-debt and profit-debt-ratios ratios to make the point in a chart but the RBA’s credit aggregates illustrate it clearly enough:

Business debt has completed a dramatic retrenchment, personal debt less so and the latter is tiny compared to mortgage debt anyway, which has continued to balloon.

In the post-GFC world, in which blind Freddy is afraid of too much debt, the relative leverage of households versus business means the former is going to chronically under perform and erode the latter over time. That is also the recent history on the US.

To put it bluntly, the RBA’s campaign to raise house prices in order to get consumption moving is pushing on a weakened spring, if not a piece of string.

However, it is not all bad news. Business has one further reason to feel confident: politics. I’ve been quite surprised by the extent to which politics seems to matter to the business community. As the post-election bounce illustrated, it is clear that in some broad sense business feels better when the Coalition is in power. This is all the more so today when the leadership goes out of its way to appear business-friendly and is prepared to warp policy to the benefit of businesses (as opposed to defend markets).

When you think about it, it makes sense. Unions are stronger under Labor (though certainly nothing like they used to be) and the structure of the economy these days is so utterly dependent upon the Budget and interest rates that the Coalition pitch of being a better manager of both seems to resonate more strongly with its supporters and overwhelm other doubts. That provides a firm psychological prop for business sentiment.

But, again, there are reasons to suspect that that can’t last, just as it didn’t in 1996/97. The budget problems confronting this Coalition government are altogether more difficult than the last. The Howard government inherited an economy entering three sequential booms in productivity, housing and then resources. The Abbott government has inherited an historic mining bust, a half-baked housing boom fraught with bubble fears and foreign investment tensions, as well as persistently weak competitiveness and paralysed productivity.

To fix these things the government will have to restore dynamism to the economy via structural change but that means unwinding an enormous consumer bubble of entitlement to easy living. In short, the business community’s greatest hope of economic strength – a return to surplus politics – is in reality its greatest source of weakness because households are not yet prepared to deliver it. This is playing out before our very eyes in collapsing confidence for government, reform and in general, even though the needed structural changes needed have barely begun.

These three forces lead to the corollary of the fourth, captured in the following chart:

Without buoyant consumers, there is excess capacity in the economy and little need for business to invest, leaving it instead cutting costs to boost profits and sapping confidence in growth prospects.

The balance of the four forces leads to a conclusion that strong business sentiment will lose out to weak consumer sentiment over time.