Find below the highlight’s from Westpac excellent August Red Book:

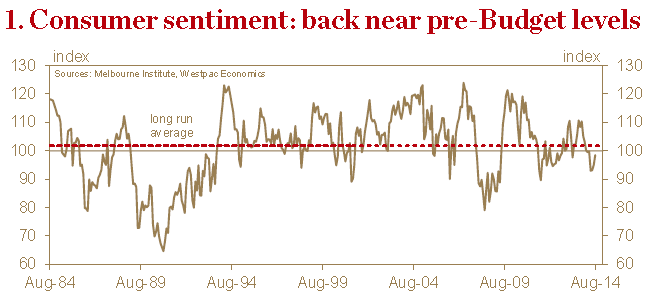

The Westpac–Melbourne Institute Index of Consumer Sentiment rose 3.8% in Aug, the most convincing gain since the Budget-related fall in May. At 98.5, the Index is back near ‘neutral’ having reclaimed most of the post-Budget decline.

― Two main factors likely contributed to the rise this month: the abolition of the unpopular carbon tax, and Senate resistance to many of the unpopular measures in the May Budget. Both positives could be undermined if the impact of the carbon tax removal falls short of consumers’ expectations or we see renewed uncertainty around key policy changes.

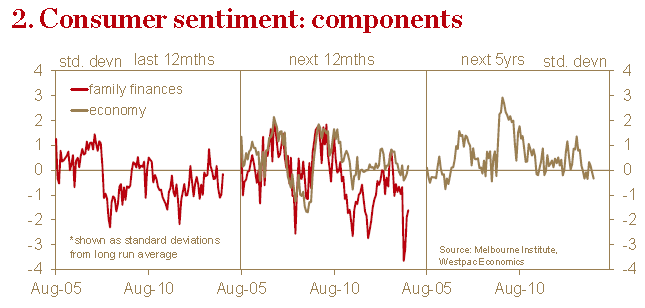

― The improvement this month was led by reduced pessimism on family finances – the components hit hardest in the post-Budget fall. Consumers are also more positive on the near term economic outlook but downbeat on the 5yr economic outlook.

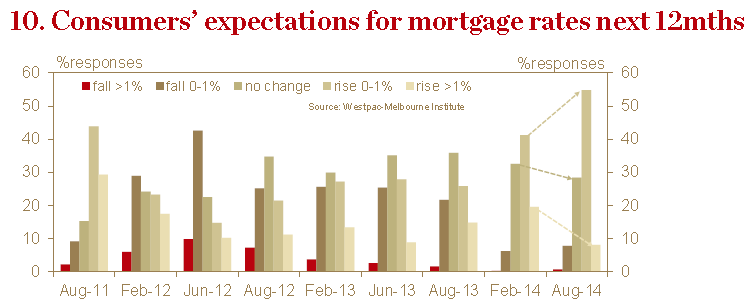

― Additional questions on mortgage rate expectations show a clear majority (63%) expect interest rates to be higher in 12mths time. That is similar to the last time we surveyed interest rate expectations in Feb, although the Aug survey found a clear outright consensus that the increase would be in the 0-1% range with few expecting rates to rise by more than 1%.

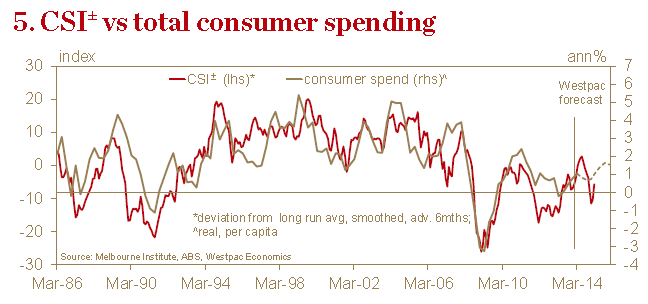

― CSI±, our modified sentiment indicator that we favour as a guide to actual spending, posted a solid 3.7% gain in Aug and is now pointing to positive, albeit sluggish, growth in per capita spending of around 0-½%yr (1¾-2¼%yr once population growth is factored in).

― Recent retail sales and business survey data confirm a slowdown in demand in Q2 but a less abrupt one than the post-Budget fall in sentiment would normally indicate and with more recent signs of renewed momentum.

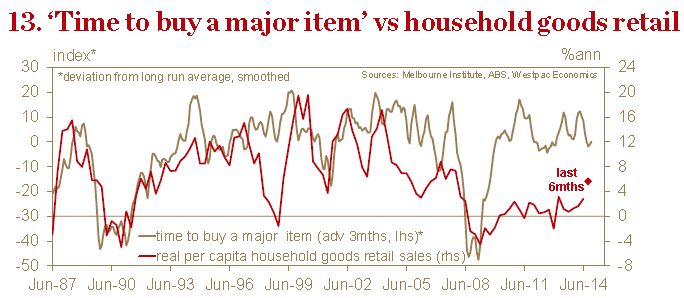

― The sub-index on ‘time to buy a major item’ rose 1.9% in Aug to be back in line with its long run average. Household goods retail sales point to a renewed pick up in durables spending after a flat Q2.

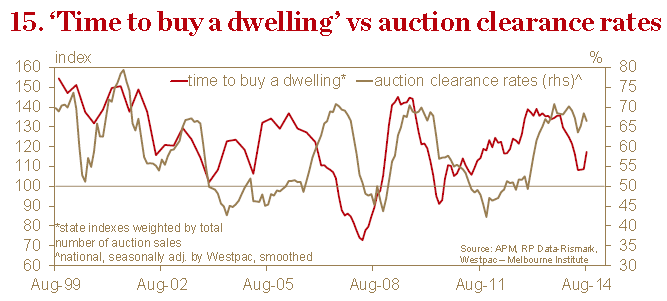

― Sentiment towards housing brightened. The index tracking views on ‘time to buy a dwelling’ surged 9.7% to be 12.1% above its post-Budget read. Buyer attitudes are still down on last year’s highs but are now back near long run averages.

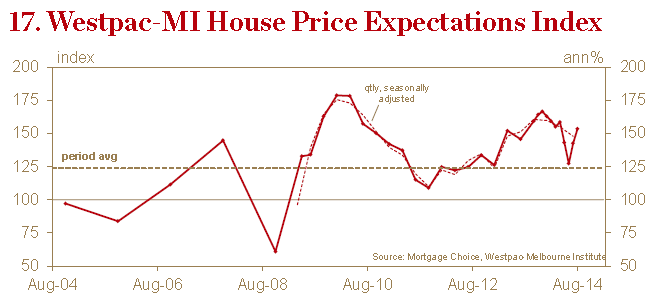

― The Westpac Melbourne Institute House Price Expectations Index continued to rally, rising a further 7.6% after Jul’s 12.1% rebound. The mix is consistent with signs of renewed momentum in housing markets since Jun.

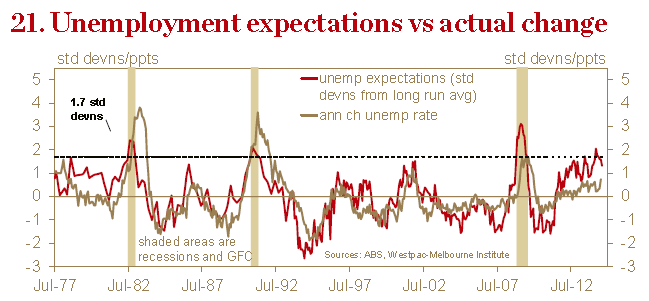

― Expectations for job prospects improved modestly. The Westpac-Melbourne Institute Unemployment Expectations Index fell 3% from 156.1 in Jul to 151.4 in Aug (recall that lower reads indicate fewer consumers expect unemployment to rise). The index is now 7.9% below its March peak but still high by historical standards. Notably, the decline came despite the surprising jump in the unemployment rate from 6% to 6.4% reported mid-way through the survey period.

Sentiment and spending are playing out very much as expected. MB has reckoned on a modest consumer recovery this year that tailed away as the election euphoria passed. That is where we are.

We do not expect this to change because we hold the view that the consumer has made a structural adjustment to higher savings rates following the generational shock of the GFC. And, frankly, if you look into Westpac’s dour spending forecasts, they agree.

The balance of risks to the outlook suggest the same. House prices are still rising at a good clip but the carbon tax removal will disappoint and the Government has no choice in returning to its Budget austerity project. It’s both politics and economics that are driving the necessity.

In terms of the former, the Government can not fail on its fiscal management mandate. That’s it’s central claim to legitimacy.

On the latter, if they don’t repair the Budget outlook then Australia’s economic model will unravel. Of course, when they do repair the Budget outlook the model will also unravel, but a little more slowly.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.