by Chris Becker

Ratings agency Fitch is out with a fascinating report today on global house price trends, specifically Asia Pacific.

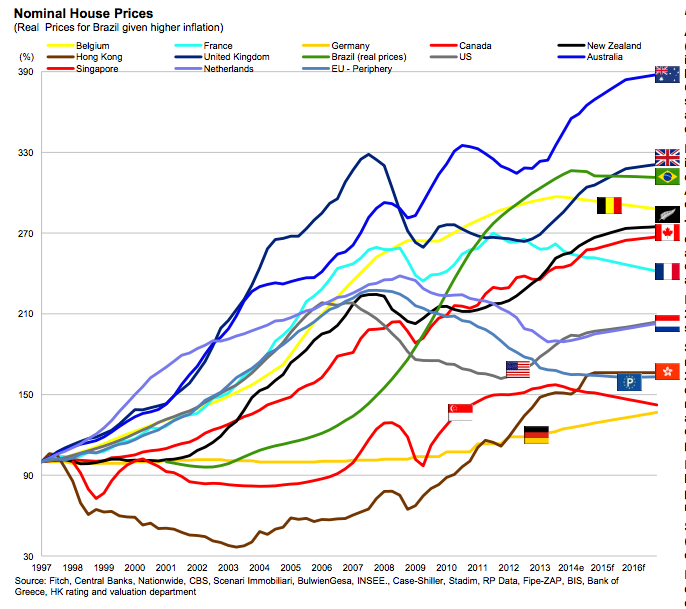

First of all, bravo Australia, bravo! Highest nominal house price growth across all developed countries since 1997:

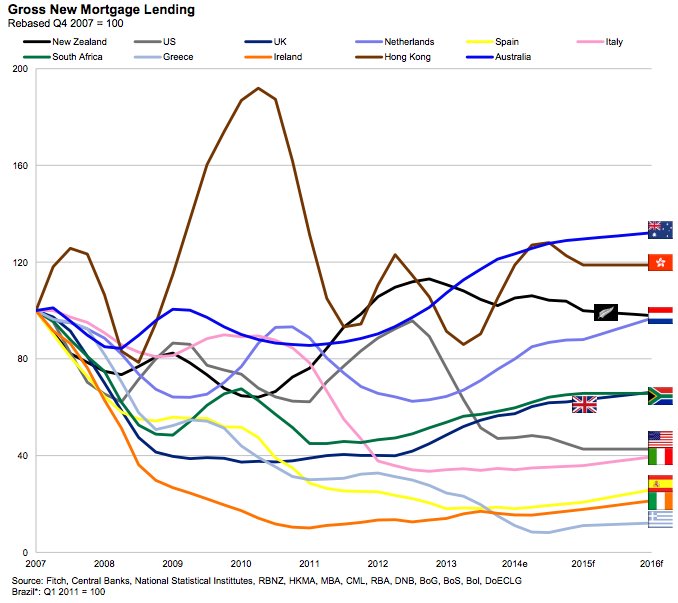

And of course, the gold also goes to Aussie banks as gross new mortgage lending surpasses everyone, everywhere:

Given these standouts, plus a closer look at the supply/demand dynamics, Fitch expects slower price growth for 2015 to about 4% in Sydney and Melourne with Perth at around 3% or less.

Here are the headline key points:

- Price growth has been driven by continued record low interest rates and increasing investor demand in the Sydney and Melbourne markets.

- Annual growth rates to date have reflected a twotiered market with the prices in Australia’s two largest cities outstripping other capital cities’ growth.

- Homebuyers have benefited from record low interest rates, with an average discounted standard variable rate for new loans of 5.1% since August 2013. Household debt to disposable income has been relatively flat since 2006 with a modest movement to around 145%-150%.

A very interesting call here – Fitch expect mortgage rates to rise?

affordability metrics to stay tight in 2015 with a potential interest rate rise and moderate house price growth in line with or even again exceeding wage growth. Mortgage rates have remained at historical lows since the RBA policy rate was reduced to 2.5% in August 2013 in response to weakening global demand and an expected slowdown in resource investment.

Lenders have also kept the discounted discretionary ‘standard variable rates (SVRs) at 5.1% compared to 5.9% 24 months ago.

Borrowing capacity has been curbed as lenders build in a buffer of 1.5%-2.0% when assessing borrowers’ debt service ability. This has partly offset lower rates.

But they are cautious:

Fitch expects policy and mortgage rates to remain flat in 2015. Large increases in the policy rate are unlikely as the RBA continues to guard the economy against the reduction in resource investment and focuses on stimulating the non-mining sectors of the economy.

And its all about “investment”, with the only returns being capital gains:

- Investment loan approvals are expected to continue to represent 50% of new lending (excluding. refinance loans) as investors compete with owner occupiers.

- Investor loans have risen 25% in the year to September 2014 and now make up 50% of new loans (excluding refinance).

- Investors have been driven by better returns with deposit rates remaining at historical lows.

- Increased housing activity in Sydney and Melbourne has resulted in price growth pushing gross rental yields to under 4%.

- With moderate house price growth expected to continue, rental yields will continue to compress to less than 3.5%.

The bottom line (emphasis added):

Fitch expects investor demand to remain high in Sydney and Melbourne, so long as interest rates remain at the current low level and so long as the tax incentives to invest in property remain.

Higher prices are pushing rental yields down and Fitch believes that this will temper the demand from investors and is likely to contribute to lower house price growth in 2015.

Somehow I don’t think most “investors” care about rental yield at purchase, its about capital gains over time and of course, if your property doubles every 7 to 10 years, so does your yield.

A rate rise by the RBA is very unlikely given the headwinds facing the Australian economy. With next to no macroprudential tools in place, FIRB asleep at the wheel and no alternative investments available, the only credible barrier to speculators dominating the Australian property market in 2015 is a significant spike in unemployment.